China Tells Inefficient Firms to Toughen Up or Prepare to Fail

After letting inefficient firms survive for years, Beijing is now allowing them to fail.

.jpg?auto=format%2Ccompress&w=200)

(Bloomberg) --

China is turning the screws on the nation’s companies as authorities seek to take advantage of the global pandemic to strengthen its industrial might.

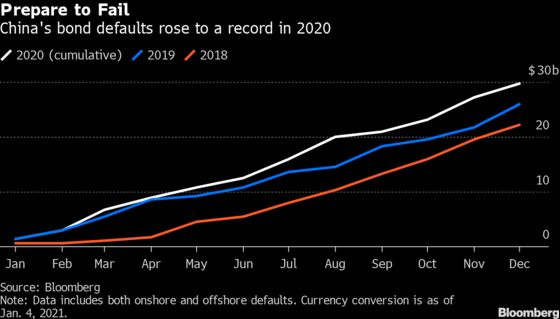

After letting inefficient firms survive for years, Beijing is now allowing them to fail. Bond defaults rose to a record $30 billion in 2020, including high-profile enterprises that had previously counted on the implicit guarantees of the state. Scrutiny and punishment of credit-rating agencies are increasing, while domestic exchanges delisted at least 16 stocks from their main boards last year -- the most in data going back to 1999.

The trend is set to pick up in 2021 as China’s central bank tightens financial conditions, making it harder for both state-owned or private firms with inadequate cash flow to survive. An economic recovery and a strong currency are giving policy makers more room to focus on reducing the amount of debt in the financial system, which is at a record 277% of domestic output.

“The good thing is China will keep financial risks under control, but the bad thing is it won’t bail out firms unless they are in an extreme situation,” said Larry Hu, head of China economics at Macquarie Group Ltd. “The government wants to make the most of a solid growth recovery to tighten monetary policy. We may see more companies facing challenges in seeking cash.”

Beijing has in recent months rolled out more measures aimed at increasing the efficiency of the country’s capital markets, as well as the quality of its companies. In December alone, China tripled the maximum prison sentence for securities fraud to 15 years, proposed shortening the delisting process for unprofitable stocks and vowed to improve oversight of the country’s credit-rating industry. China also imposed a cap on bank lending to property developers, a sector that’s laden with debt.

As China gets tougher on industry, its loosening of control over financial markets will allow investors -- rather than the state -- to punish poorly-run companies and reward growth. Concern over China Inc.’s reliance on U.S. markets for fundraising may have partly driven that action, as well as the Communist Party’s economic strategy of “dual circulation” that prioritizes strengthening domestic demand.

While the People’s Bank of China is unlikely to hike interest rates in the coming months, it has repeatedly signaled it will moderate the supply of cheap credit. The timing makes sense -- booming export growth has given the central bank room to cut back on stimulus measures deployed during the coronavirus pandemic.

But the consequences for the most vulnerable companies can be brutal: Beijing’s commitment to normalize policy was a factor behind a sudden wave of corporate defaults at the end of last year, which in turn froze lending in the interbank market. The World Bank has also warned that excessive policy tightening could be damaging for the global economic recovery.

Funding China’s future growth engines without destablizing its highly-leveraged financial system requires a carefully calibrated rebalancing of the world’s second-largest economy. For China and its companies, a shift of that magnitude can only be successful if those with weak finances and poor returns are allowed to go bust, according to Carlos Casanova, an economist for Union Bancaire Privee.

“Authorities will continue to walk a tight rope between stabilizing growth and reducing economic fragilities,” Casanova wrote in a December note. “For China’s debt restructuring gambit to pan out as expected, the pace of financial reforms must accelerate rapidly.”

©2021 Bloomberg L.P.