China Takes a Risk on GenZ’s Love Affair With Debt

(Bloomberg Opinion) -- China has a mounting debt problem. Not just over-leveraged companies, but a rapid build-up on household balance sheets that is hitting records. You can blame youth for a borrowing binge that, if left unchecked, could be China’s next credit bubble.

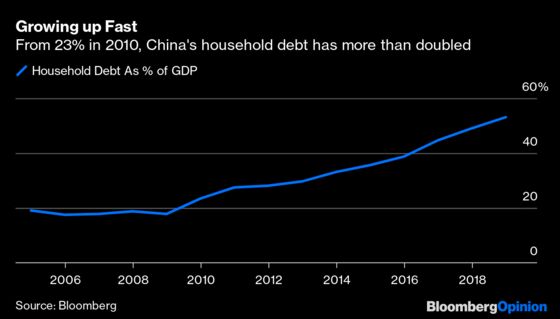

Household debt hit levels of 57% of gross domestic product in the third quarter, according to Bloomberg Intelligence analyst Matthew Phan, more than double just 27% in 2010. Fitch Ratings said in July that it was surging at a pace roughly double nominal GDP growth. Behind it lies increasing use of mortgages, credit cards and smartphone lending apps. As a percentage of disposable income, household debt jumped to 99.9% in 2018 from 93.4% a year earlier, according to the People’s Bank of China in November.

China’s Generation Z, born from the mid-1990s to the early 2000s, has taken to debt in a way their more-frugal parents didn't. They have little income and therefore virtually no credit history. It doesn’t matter, because they have had access to a whole range of online banks, fintech startups and peer-to-peer lenders, some of which charge exorbitantly high interest rates.

A run of scandals has featured the owners of small, online lenders running off with the money. Borrowers have used consumer loans to buy real estate or speculate on stocks. Some have lost their savings due to high interest rates, well over 50% in some cases by adding “transaction fees” even though the legal limit is 36%.

In late 2017, China asked peer-to-peer lenders to apply for licenses to justify their operations. Many have applied but none have received them. Some 1,200 closed in the first nine months of 2019 as loans outstanding tumbled 48%.

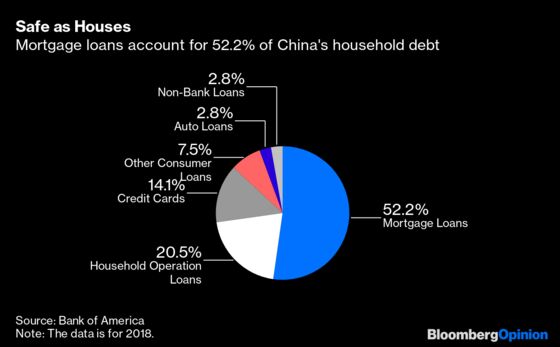

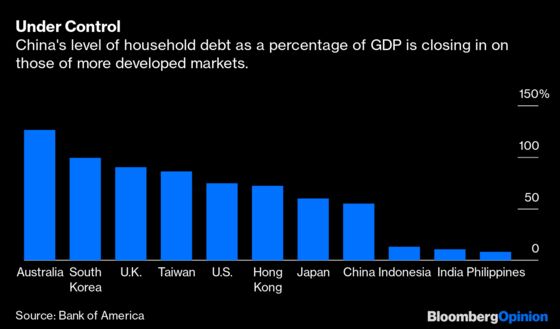

To be sure, this is no systemic risk waiting in the wings. More than half of household debt is secured by some kind of collateral, as much of it is tied to housing or auto loans. Viewed in a global context, China’s debt levels look moderate. Household debt-to-GDP is 126% in Australia, 99% in South Korea, and 75% in the U.S., according to Bank of America.

But that’s less reassuring than it seems. U.S. household debt has actually fallen in recent years, from around 90% in 2010. China’s upward trend shows no sign of abating. For all the crackdown on peer-to-peer lenders, there are plenty of ways to borrow money. Apart from consumer lenders like billionaire Jack Ma’s Ant Financial, once barely used credit cards are getting more popular. Outstanding credit card debt reached $1 trillion in China at the end of 2018, having risen more than 30% annually in the last few years, Fitch Ratings noted.

The real-estate loan worries that plagued Americans during the 2008 financial crisis are less of an issue in China. Beijing has curbed over-exuberance in the housing market over the past five years by raising down payments on purchases, capping new home prices, or pushing banks to tighten mortgage lending. These could be loosened should the market suffer real damage. Chinese policy is dominated by the need to maintain stability.

Yet as China’s household debt levels keep rising, costs in servicing debt climb with it. Consumers take this on at considerable risk. Unlike the United States, China doesn’t have a personal bankruptcy law, meaning that creditors can go after everything a debtor owns. The resulting fear undermines consumption more than it otherwise would. That’s bad news for an economy suffering from the trade war and hoping that consumers will prop up growth in coming years. GenZ’s love affair with personal credit going sour could be the last thing China needs.

Bank of America putChina's household-debt-to-GDP level in 2018 at 55%.

According to the International Monetary Fund, there are some protections for debtors - courts can allow debtors to pay their obligation in installments.and they can keep certain minimum assets to take care of themselves and their families. But that's only if the debtor has a single creditor rather than multiple lenders, as is increasingly the case.

To contact the editor responsible for this story: Patrick McDowell at pmcdowell10@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.