(Bloomberg Opinion) -- What’s not to like when borrowing in a foreign currency is much cheaper than at home? That’s the happy situation for China as it launches another batch of debt deals in euros, repeating its successful foray of last year. Beijing is bringing five-, 10- and 15-year tranches to further build a yield curve in euros.

But this isn’t some covert snub to the U.S. or a judgment on the dollar’s primacy. China raised $6 billion in a four-tranche deal just last month, as it has done annually since 2017.

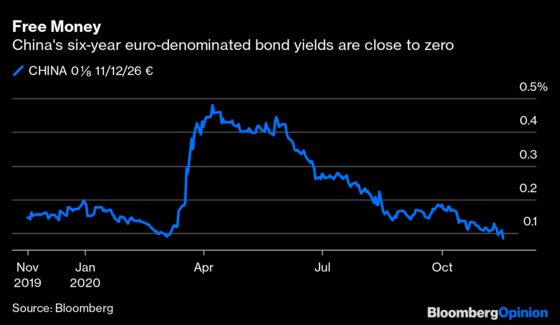

It’s just so amazingly cheap to fund in euros that it would seem foolish not to. The backdrop is a European Central Bank that’s hoovering up bonds in its quantitative easing program and which has a -0.5% deposit rate. China will only have to offer a negative yield for the new five-year tranche; even the 15-year note will be below 0.75%. This compares very favorably to the 3.15%-3.55% yields on comparable domestic notes in yuan, which have been rising steadily since the summer.

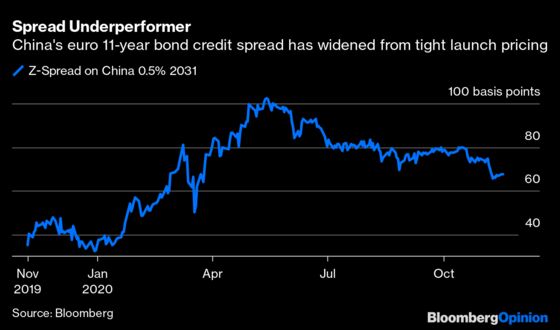

China’s euro-denominated bonds aren’t eligible for purchase by the ECB, which does have an impact in the secondary market. Credit spreads — the premium charged above benchmark European government debt — widened on last year’s notes.

But this new raft of issuance has enlivened investor interest, allowing the lead managers on the sale to tighten the indicated spreads to below those on the 2019 debt. Given the aggressive pricing, the overall order book may not reach the 20 billion euros ($23.7 billion) of demand on last year’s sale, when 4 billion euros was raised across seven-, 12- and 20-year maturities.

The yuan is at its strongest level in two years and China has foreign exchange reserves in excess of $3 trillion, so these foreign borrowing exercises are really about diversifying its international investor base. There was a lot of European interest last year.

Italy made similar moves this week to maintain its international following, with a dollar issue, but it paid a price. The $3 billion five-year deal had a 1.3% yield, which is more expensive than where Italy funds in euros (very close to zero for five-year debt). Nonetheless, Rome will be pleased its order book was more than three times covered, showing it still has U.S.-based demand.

This is what these foreign currency sovereign deals are about: national marketing. China’s sale opens the door for its companies to access the euro bond market, as it’s useful to have a sovereign benchmark for price comparisons. The dollar bond market for Chinese corporates, usually priced out of Hong Kong, is still 20 times larger than the one for euros, so there’s room to go further. Especially when China is rewarded for building its brand courtesy of the euro area’s incredibly low rates.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.