Looking to Ride This China Bull Market? Better Think Twice

(Bloomberg Opinion) -- Is this the beginning of another 2015-style bull run, or just a dead cat bounce?

China’s $6.4 trillion stock market is roaring back, reentering bull territory after surging more than 20 percent from its Jan. 3 low. Turnover surpassed 900 billion yuan on Monday, the most since 2015. Brokers tracked by Bloomberg Intelligence soared by their 10 percent daily maximum for the second consecutive day. That could mean this rally has longer to run, according to some superstitious traders.

In many ways, China Inc. is looking a lot like it did three years ago – at the dawn of another neck-breaking, super bull run.

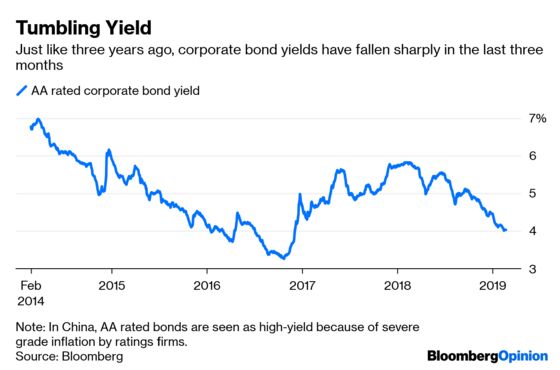

In late November 2014, the People’s Bank of China surprised the market with a cut to its benchmark lending rate. That drove high-yield companies’ financing costs from a December high of 6.1 percent to 5.2 percent just three months later. Thanks to the central bank’s latest easing measures – including a surprise reserve-ratio cut – the cost of borrowing has also fallen lately. In theory, business operations should get healthier with cheaper borrowing, which bodes well for stocks.

And just like three years ago, Chinese companies are battling deflationary pressure. If Beijing can somehow manage to pull the economy from disinflation quickly, or so the thinking goes, we should expect a sudden jump in profits, because earnings are expressed in nominal terms.

To revive animal spirits in the A-share market, though, China has to cross a few hurdles.

First, cheaper borrowing costs are meaningless if credit remains unavailable to the private sector. While local governments, and their off-balance-sheet affiliates, have enthusiastically issued new bonds in recent months, high-yield enterprises – real estate developers, for instance – still can’t raise new notes onshore. In a series of articles last week, even researchers at the PBOC acknowledged this pitfall, conceding that China may have “capital swamps”: pockets of excess funds and lower funding costs for some, but not others.

Second, this round of deflation may prove far more stubborn. Back in 2016, Beijing fought falling prices by focusing on the low-hanging fruit – supply-side reforms such as shutting down empty factories to curb coal mining and steel production. The same trick won’t work twice, and Beijing will discover that weak demand is a lot more difficult to correct than excess supply.

Most importantly, China’s private sector is now battling a crisis of confidence, causing some entrepreneurs to flee the country. We’re already seeing the private sector’s mistrust of the government in business decisions: Manufacturers are parking cash in industrial land, while holding back purchases of equipment and machinery. Such behavior is a good indication future sales growth could slow, as my colleague Anjani Trivedi found.

Ultimately, the stock market is a celebration of entrepreneurial spirits. If private enterprises no longer have faith in the system, there’s only so far this rally can go.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.