China Stocks Steady After Monday’s Record $720 Billion Wipeout

Chinese Equities Eke Out Gains After Monday’s $720 Billion Rout

(Bloomberg) -- Chinese stocks stabilized after the market’s biggest loss of value on record, with traders unconvinced that the recovery would last given the spreading virus outbreak.

The CSI 300 Index of equities closed 2.6% higher, with a measure of 10-day swings jumping to the highest in four years. The broader Shanghai Composite Index advanced 1.3%, while the ChiNext Index gained 4.8% on its best day in nearly a year. Turnover on domestic exchanges leapt 78% on Tuesday, the biggest increase since May 2016, to 881 billion yuan, a 10-month high.

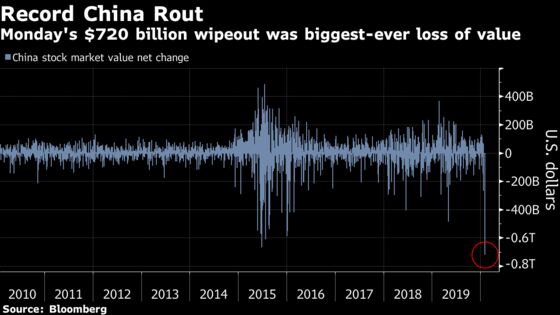

The gains follow a $720 billion plunge in Chinese shares, the largest shareholders in China have ever seen on a net basis. Even for an equity market that’s no stranger to volatility, declines of Monday’s magnitude are rare. The CSI 300 Index has only dropped 7.5% or more on eight previous occasions in its almost 15-year history, and half of those were during the turmoil in 2015. The last time it happened -- around the yuan devaluation in August that year -- the benchmark fell another 7.1% the following day.

Investors are bracing for wilder swings in stocks as they react to Beijing’s supportive measures and the worsening virus outbreak that’s threatening China’s economy. While some came out Tuesday to buy stocks on the cheap, most stopped short of predicting that any rebound will be sustained. More than 100 stocks were still trading limit down on Tuesday.

“The worst is not over for China’s markets,” said Sean Lee, a fund manager at Shin Kong Investment Trust in Taipei who is buying Chinese suppliers to Tesla Inc. after the U.S. company’s shares soared overnight. “We’re only seeing a rebound after yesterday’s sharp decline. It gives us time for a short breather. Funds will flock to stocks with good news in the short term.”

The CSI 300 slumped 7.9% Monday as mainland markets traded for the first time since Jan. 23. All but 162 of the 4,000-odd stocks in Shanghai and Shenzhen recorded losses, with about 90% dropping by the maximum allowed by the country’s exchanges. The huge number of shares trading limit down means it could take days for investors to execute their orders.

China set its daily yuan fixing stronger than the key 7 per dollar level on Tuesday in a signal of support even as the currency weakened past the key level on Monday. The People’s Bank of China set the daily reference rate at 6.9779 per dollar.

Two-thirds of the Chinese economy will remain closed this week as several provinces took the extraordinary step of extending the Lunar New Year holiday to help curb the spread of the disease that’s claimed more than 420 lives, with confirmed cases topping 20,000.

Casino stocks fell after Macau, the Chinese territory that’s the world’s biggest gambling hub, said it would discuss potential measures to suspend operations in the sector in a bid to contain the spread of the deadly coronavirus. Galaxy Entertainment Group Ltd., Wynn Macau Ltd., SJM Holdings Ltd. and Sands China Ltd. fell at least 1.5%.

Even investors who were brave enough to buy stocks on Monday aren’t exactly turning bullish for the long term. The declines took major stock indexes below almost every technical support level in sight, leaving analysts with little to go on for their predictions.

“There’s not much I can buy today,” said Lu Boliang, CIO at Shenzhen Qianhai Daoyi Investment Holdings Co. “It was just panic, panic, panic everywhere. Some people who were planning to sell at the open might have turned buyers today after seeing fewer shares splattered. Prices may be so low that its too painful to sell at this stage.”

--With assistance from Amanda Wang.

To contact the reporters on this story: Cindy Wang in Taipei at hwang61@bloomberg.net;April Ma in Beijing at ama112@bloomberg.net

To contact the editors responsible for this story: Richard Frost at rfrost4@bloomberg.net, Sofia Horta e Costa

©2020 Bloomberg L.P.