(Bloomberg Opinion) -- Portfolio money is returning to China stocks, and the view from 10,000 feet suggests the country is the place to be. The problem is there’s no easy way to deploy your money.

In the first full week of 2019, investors plowed about $1.6 billion into shares in Shanghai and Shenzhen through the Hong Kong stock connect program. Offshore, the MSCI China Index rose 5.1 percent, its best weekly performance in more than two months.

There’s a lot to like about China. The yuan has surged to a six-month high, and Goldman Sachs Group Inc. predicts the currency will stay firm this year. Meanwhile, the central bank alleviated a credit crunch by cutting the required reserve ratio for commercial lenders on Jan. 2. That’s sparked bets of many more reductions to come.

It’s a sharp reversal from a particularly difficult 2018 for China stocks that was caused more by a widening corporate earnings gap with the U.S. than the trade war. President Donald Trump’s tax cut supercharged profits for U.S. companies, and Beijing’s untimely deleveraging campaign damaged China Inc.

That hurdle has been removed. China’s fiscal policy will be more proactive this year, while Trump has already used up his ammunition. Granted, China’s corporate leverage is a concern but the U.S. economy is also floating on an “ocean of debt,’’ in the words of billionaire investment manager Jeffrey Gundlach.

Execution is the key, though. Finding investment targets in China’s $8 trillion stock universe remains difficult. The hottest names can go from hero to zero in one day, losing billions of dollars in value.

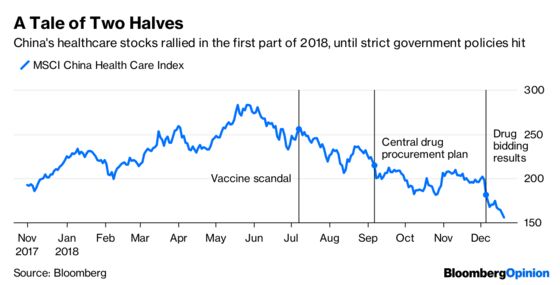

Last year’s bruising experience with education and healthcare stocks is still fresh on investors’ minds. Both are plays on China’s rising middle class, and relatively immune to the trade war, yet both were damaged by sudden shifts in government policy.

Education stocks were all the rage until August, when China decided to amend rules governing the country’s lucrative private education sector. The final kiss of death came in November when Beijing said for-profit kindergartens could no longer go public. A similar picture has emerged for healthcare stocks after the government decided to take over drug procurement for hospitals.

In hindsight, neither change was surprising. K-12 education has always been seen as a public good, not a place for private capital or profit. And China’s drugmakers were too content reaping profits from generic drugs to innovate.

All the same, such flash crashes are keeping investors skittish.

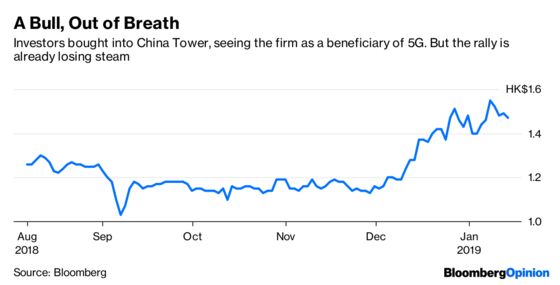

Take China Tower Corp., for example. The state-owned operator of telecom towers soared as much as 37 percent between November and early January on expectations it would be the major beneficiary of China’s 5G technology push. But as soon as the industry regulator confirmed some regions would be allowed to issue temporary licenses this year, investors started to sell. Knowing that China Tower’s owners (the mobile-phone service providers) are also its largest customers — a major corporate governance red flag — they decided the best policy was to take money off the table.

Or consider China’s solar power companies. They enjoyed only a one-day pop after the government said some plants will be able to sign long-term power purchase agreements with grids at fixed tariffs. Why were investors so nervous? The industry’s mountain of debt. It was only in October that China Singyes Solar Technologies Holdings Ltd. defaulted on a bond payment.

China likes to say it wants a slow bull market — not a fast, furious rally that inevitably ends with a crash. The way sentiment is looking now, any returning China bull will quickly run out of breath.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.