China State Firms Once Deemed ‘Safe’ Now Rocked by Defaults

China State Firms Once Deemed ‘Safe’ Are Now Rocked by Defaults

(Bloomberg) -- Rising defaults by China’s state firms are showing the need for bond investors to be much savvier about those borrowers -- no easy feat in a country where government decisions and business operations lack transparency.

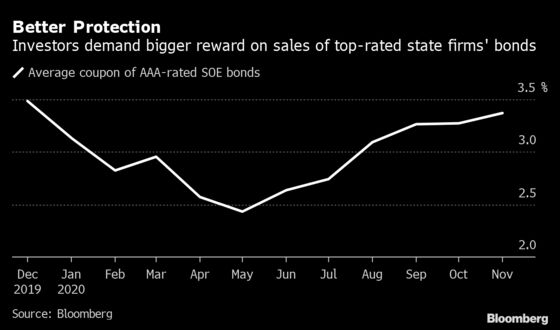

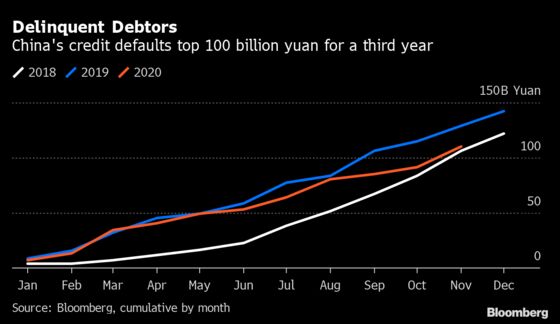

Five state-linked companies -- from a coal miner to a top chipmaker and an auto firm with ties to BMW AG -- have defaulted for the first time in the onshore bond market this year. That’s the most since 2016. In the secondary market, the average yield of more than 700 riskier bonds of local state-owned enterprises jumped to 17% from 13.4% after a payment failure by Yongcheng Coal & Electricity Holding Group Co., Bloomberg-compiled data show. Last month’s defaults helped send debt issuance costs to a 2020 high for top-rated SOEs, as sovereign bond yields also climbed.

The recent defaults among state firms represent a shift from the past two years, when occurrences were mostly among private sector companies. They represent less than 30% of China’s AAA-rated onshore debt. A pivot in the source of credit risk to the gigantic state sector could pose a major challenge to the investing community and policy makers alike.

“State-linked credits have been hammered, but the quality of those credits is inextricably connected to government policy, which can be very opaque,” according to Brock Silvers, chief investment officer of Kaiyuan Capital. “State-linked credits can thus be particularly treacherous, especially for investors without significant local expertise.”

But investors will need to focus beyond government policy. Repricing risk among state borrowers means that examining a company’s business fundamentals, as well as its ownership structure, will become more imperative. Still, strong knowledge about murky local politics and evolving industry policies will also help better identify the most vulnerable firms in the state sector.

“Investors should pay more attention to the market competitiveness and solvency of each company, instead of relying too much on government support,” said Ivan Chung, Hong Kong-based analyst at Moody’s Investors Services. China is unlikely to come to the rescue of a weak company in a competitive industry, such as commodities, if the firm’s default won’t trigger major fallout, he said.

Potential buyers are also re-evaluating the odds of recouping investments once state-owned firms enter distress or default. Bonds of state-linked defaulters have tumbled recently, a sign of dwindling faith in restructuring outcomes for the firms. Peking University Founder Group Corp.’s keepwell bonds trade below 10 cents on the dollar, Qinghai Provincial Investment Group Co.’s bonds are at 37 cents and some Tsinghua Unigroup Co. notes change hands in the 20-cent range.

“Repricing is already happening in SOE bonds with the low recovery expectations” according to Owen Gallimore, head of credit strategy at Australia & New Zealand Banking Group Ltd. in Singapore.

| Read more about the growing risks in China’s credit markets: |

|---|

| Why China’s Debt Defaults Are More Alarming This Time: QuickTake |

| China Credit Pain Worsens as Two State-Linked Firms Default |

| Why China Sought Help With Credit Ratings for Bonds: QuickTake |

| The Ticking Debt Bomb in China’s $15 Trillion Bond Market |

| State Sector Defaults Raise Alarm Over China Town Builders |

Efforts by Beijing to deleverage China’s economy and increase efficiency mean more state companies may be allowed to default. Firms in poorer provinces are especially vulnerable to the shift amid the lingering effects of the coronavirus pandemic.

“As the domestic situation gradually stabilizes, the determination to resolve local debt risks and reduce overall leverage is being reflected in the prudent monetary policy” of China’s central bank, said Rollin Cai, fund manager at HSBC Jintrust Fund Management Co. Local fiscal revenue is likely to continue being squeezed by pandemic impacts, reducing how much provincial governments can support local SOEs, he said.

Still, authorities will be keen to prevent defaults from upsetting the financial system too much. China’s top financial regulators met last month to discuss maintaining market stability and liquidity in the wake of November’s defaults. They also pledged a “zero tolerance” approach to violations in the bond market.

But it’s clear that the bloated state sector is in for some hard times, and investors need to be agile so they don’t get caught up in what could become a messy process. “For bonds that were originally overvalued, we will now definitely require higher premiums and better protection,” said Yuanyuan Li, head of fixed income at HSBC Jintrust.

“Investors are returning to look at the fundamentals of pricing by evaluating an issuer’s solvency,” she said, “rather than their government background and ratings.”

©2020 Bloomberg L.P.

With assistance from Bloomberg