The One Thing That Could Derail Japan’s Sales Tax Hike

(Bloomberg Opinion) -- China may take Japanese fiscal policy hostage.

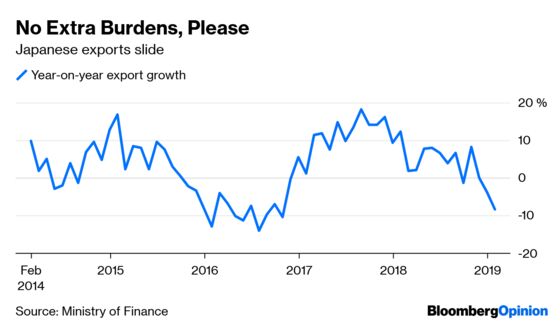

The fallout from China's slowdown is snaking its way through Asia's economy – and the world – bit by bit, data point by data point. Japanese exports, long considered a strength, just took an enormous hit.

Shipments to the Middle Kingdom plummeted 17 percent in January, the finance ministry said Wednesday. Overall, exports fell 8.4 percent, surpassing the 5.7 percent drop penciled in by economists. That's bad news for domestic bright spots like capital spending.

Numbers like this and you start to worry that Japan's economy needs fresh stimulus – let alone a burden like the consumption tax increase that's scheduled for October.

The hike has already been delayed twice. A predecessor has its iconic place in the pantheon of self-inflicted economic wounds: It continues to wear the blame for a recession in 2014 and the Bank of Japan’s failure to crank inflation up to 2 percent.

Prime Minister Shinzo Abe said it would take a Lehman-type jolt to get the government to shelve the tax increase again. Should we take him literally?

The odds of a 2008-style calamity are relatively slim; Abe is probably saying the economy would have to be substantially weaker than when he gave the levy its go-ahead in October. The current state of things certainly crosses that bar, and risks to the outlook have only mounted.

The caveats loaded into the tax increase signal ambivalence about it in the best of times. The cabinet was careful to say the hike would be 2 percentage points, not three as was the case in 2014. And Abe put a lot of ornaments on the Christmas tree: Most food would be exempt from the bump, and sales of large durable goods would get some state support.

The case for pressing ahead is that somehow services and infrastructure for aging workers need to be paid for. A chunk of the revenue also will be spent on education. And there’s never a popular time to lift taxes.

But some times are worse than others. It's not just that China and the U.S. are engaged in a trade war (though, granted, it may not be de-escalating). China's expansion is sputtering in the short term, bracketed by a long-range slowdown that's been gradually repressing its growth for a decade.

The latter was known last year, though may not have been foremost in Abe's mind. I doubt he contemplated the extent of the global deceleration at that point. Federal Reserve Chairman Jerome Powell didn't see it; why would a career politician who is a descendant of career politicians?

One model by UBS Group AG put world economic growth at a mere 2.1 percent annualized pace at the close of 2018. For some perspective, the International Monetary Fund's general rule of thumb is that growth of 2.5 percent is recession territory. (If UBS is right, stand by for another one of those ubiquitous IMF updates to its World Economic Outlook that contains forecast cuts.)

So, no. What we’re seeing isn’t Lehman-esque. That resulted in a rare outright contraction of global activity in 2009. But it might be enough to get Abe off the dime.

He’s gotta be thinking about it.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.