China Unexpectedly Drains Cash as Leverage Builds in Bonds

China Seen Slowing Cash Injections as Leverage Builds in Bonds

(Bloomberg) -- China’s central bank withdrew cash from the financial system for the first time in six months, after excess liquidity had pushed an interbank borrowing cost to an all-time low.

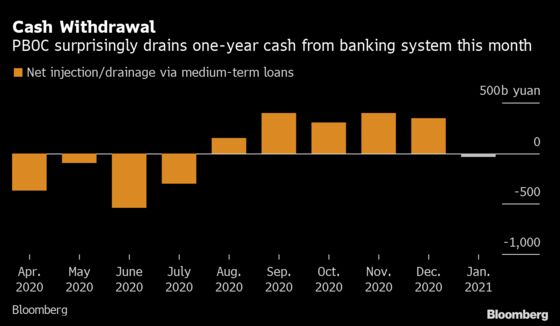

The People’s Bank of China offered just 500 billion yuan ($77 billion) of medium-term loans to lenders on Friday, resulting in a net drainage of 40.5 billion yuan for January. Analysts had predicted a net injection of 230 billion yuan. The interest rate was kept unchanged at 2.95%, according to a statement from the central bank.

The move signals that the PBOC’s monetary easing of the past two months may be ending. While the policy has helped repair sentiment in China’s credit and government bond markets, injecting too much cash risks further stoking leverage in the financial system.

“The injection is much less than consensus,” said Xing Zhaopeng, an economist at Australia & New Zealand Banking Group. “This means that the era of super-loose cash supply will end, and liquidity conditions will not be as favorable as previous years.”

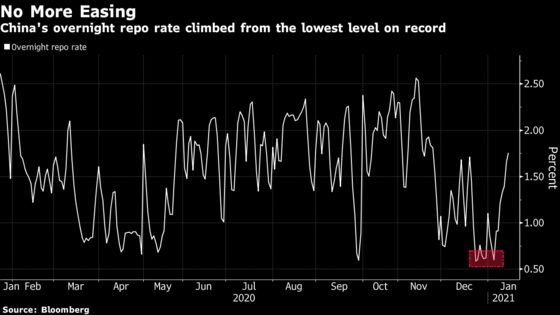

Evidence that liquidity is too loose is showing in a popular tool used by traders to finance their bond purchases. Market rates were so low -- and demand to borrow was so intense -- that daily turnover in overnight repurchase agreements touched a seven-month high earlier this month.

While this month’s cash withdrawal was unexpected, China’s bond and money markets showed relative calm on Friday. That’s because the financial system still has plenty of cash: the cost of interbank borrowing fell below the central bank’s policy rate in December, a sign of plentiful liquidity. The overnight repo rate was up 8 basis points at 1.75% as of 2:48 p.m. in Shanghai, while the yield on 10-year sovereign bonds rose 3 basis points to 3.14%.

As China’s economic recovery from the pandemic gains firmer footing, authorities have repeatedly signaled the need to repeal stimulus measures deployed last year. Beijing is keen to stabilize borrowing after the country’s debt surged to a record 277% of total output in August.

The PBOC typically pumps more liquidity into the financial system before the Lunar New Year holiday, which in 2021 falls in mid-February. That’s because residents tend to withdraw cash to pay for travel and gifts. Last year Beijing reduced the amount of capital lenders need to hold in reserve, freeing up about 800 billion yuan. It made a similar move in 2019.

| Read more about China’s financial markets... |

|---|

| China’s Narrowing Rate Gap Pinches the Yuan Carry Trade: Chart |

| China Tells Inefficient Firms to Toughen Up or Prepare to Fail |

| No Sign of China’s Bond Quota as Government Looks to Curb Debt |

A series of high-profile corporate defaults rippled through the interbank market at the end of last year, forcing the central bank to take action. The PBOC added 550 billion yuan of one-year funding to the banking system in the closing weeks of 2020, avoiding a funding crunch that was also wreaking havoc on the government debt market.

Chinese lenders will need less cash on hand than last year to pay for newly issued debt, of which they are the biggest buyers. Governments at the central and local levels will sell 1.62 trillion yuan of bonds in the first quarter, a drop of about 30% from the same period last year, according to estimates by strategists at Nomura International Hong Kong Ltd.

Lenders are also facing less repayment pressure on their interbank debt, with this month’s maturities set to be the lowest since April. The recent spike in virus cases in some provinces may discourage Chinese residents from traveling over the holiday period, potentially reducing the demand for cash.

©2021 Bloomberg L.P.

With assistance from Bloomberg