(Bloomberg Opinion) -- U.S. President Donald Trump seems to think he holds the stronger hand in any currency war with China. Don’t bet on it.

The yuan is “under siege,” thousands of companies are abandoning the country and “massive amounts” of money are pouring from China into the U.S., the president wrote in separate Twitter posts over the past two days. The suggestion is that Beijing’s hands are tied by the risk of capital flight.

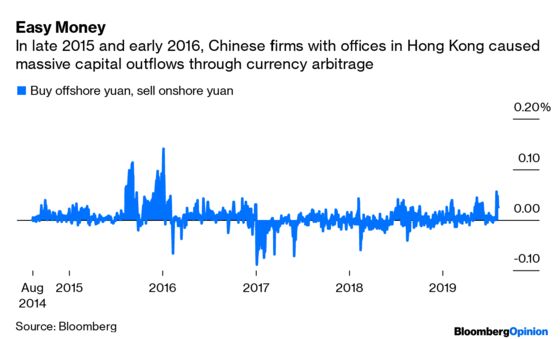

China’s last attempt to stem capital outflows was disastrous. Between 2015 and 2016, Beijing spent about $800 billion, or 20% of its foreign-exchange reserves, to stabilize the currency. Back then, banks, financial conglomerates and wealthy individuals raced to pull money out of the country, buying up luxury hotels, insurance products and any other overseas assets they could lay their hands on.

There are good reasons to believe this time is different, though. Beijing is still mindful of capital flight, but it’s less worried than in the past.

In 2015, a main channel for capital to exit China was currency arbitrage. The offshore yuan traded at much weaker levels than the onshore currency because of the absence of daily trading restrictions. Banks and state-owned enterprises with offshore accounts could earn easy money simply by selling the yuan in mainland China and buying the currency more cheaply in Hong Kong. The downside for Beijing was the resulting slide in the foreign reserves.

Nowadays, China doesn’t care as much if you short the yuan – in fact, that’s a key driver of this week’s decision to let the currency weaken past 7 to the dollar. Beijing has already taught the shorts a painful lesson. It’s amassed many tools to manage the offshore currency, the latest being issuing higher-yielding yuan notes in Hong Kong. U.S. hedge fund manager Kyle Bass exited a long-held short bet earlier this year. That’s testimony to how difficult it is to profit from this trade.

As for debt-fueled conglomerates that used overseas acquisitions to move money out, they’ve all paid a price. The former chairmen of Anbang Insurance Group Co. and bad-debt manager China Huarong Asset Management Co. are in jail, and HNA Group Co. has had its wings clipped. In any case, Chinese companies wanting to buy overseas firms are often no longer welcome, with regulators such as the Committee on Foreign Investment in the U.S. having adopted a tougher stance.

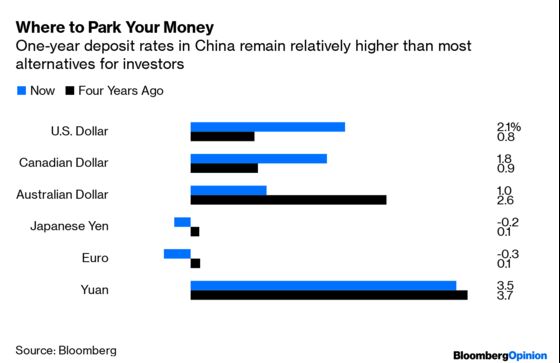

Sure, wealthy individuals in China still want to take money out, for portfolio diversification if nothing else. But bear in mind where we are in the credit cycle versus four years ago. Where can return-conscious Chinese place their money? Some 40% of global bonds are now yielding less than 1%. China’s 10-year bond, meanwhile, still offers a decent 3%, because the People’s Bank of China has conspicuously declined to join the world’s race to zero rates.

On Thursday, China set its yuan fixing weaker than 7 for the first time since 2008. While the headlines may suggest that the government is weaponizing the currency, the reality is that Beijing has been very gentle. One of the factors that goes into the yuan fix is a “counter-cyclical adjustment,” which in effect means the People’s Bank of China has been propping up the currency. Since early May, the PBOC intentionally guided the yuan stronger against market forces. Had it not, the yuan fix would be around 7.30 today, HSBC Holdings Plc estimates.

China still wants a trade deal and is extending an olive branch. Trump would be wise to realize that before patience runs out in Beijing.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.