(Bloomberg Opinion) -- Beijing has long denied charges it manipulates the value of the yuan against the dollar. Nevertheless, the currency may be the most accurate barometer of trade relations between China and the U.S. this year. Watching its movements can reveal information about Beijing’s strategies.

Theoretically, the yuan’s value is set against a basket of currencies compiled by the China Foreign Exchange Trade System, an arm of the central bank based in Shanghai. In practice, the CFETS RMB Index closely matches the U.S. dollar Index. When the dollar gauge rises, the greenback should strengthen against the yuan. Most of the time, this is what happens – except when it doesn’t.

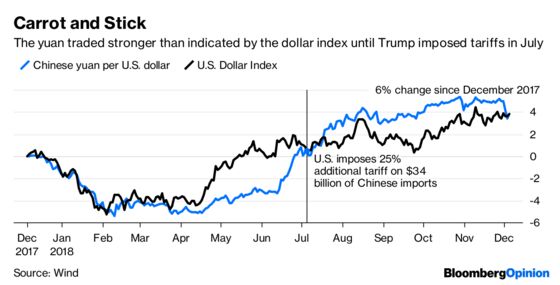

From December 2017 until spring this year, daily changes in the dollar-yuan exchange rate closely matched movements in the dollar index. But beginning around April 1, Beijing started keeping the yuan above the value implied by that gauge. That state of affairs held until late June, when China’s currency nosedived.

In April through June, Chinese officials were negotiating to prevent U.S. President Donald Trump from imposing tariffs. It appears that China played nice by holding the yuan at an artificially strong level, only to switch tactics when officials became convinced that the talks would be unsuccessful – perhaps as a warning to Trump.

On July 6, the U.S. imposed a 25 percent additional tariff on $34 billion of Chinese imports. The yuan weakened 6.7 percent in the month before and after the imposition of tariffs, compared with a drop of 1.8 percent for the dollar index. Measuring from when Beijing first started nudging the currency down, it dropped 9.4 percent compared with an increase of 4.6 percent for the dollar index.

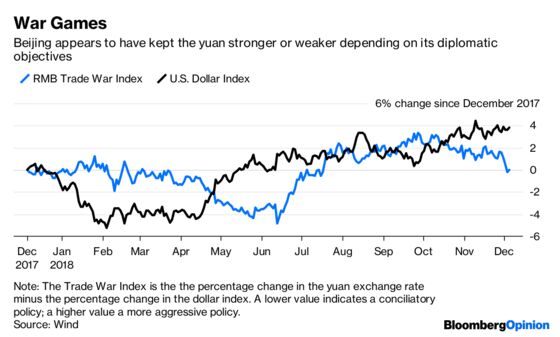

That pattern was repeated in reverse in the approach to the latest round of trade talks at the Group of 20 meeting in Argentina last weekend. Since September, a wedge has opened between the dollar index and the yuan, with the Chinese currency trading at a significantly weaker level than implied by the gauge.

As long as the U.S. was imposing tariffs, Beijing seems to have been happy to let the yuan languish. That changed with the truce agreed between Trump and Chinese President Xi Jinping in Buenos Aires.

The yuan spiked after the agreement, even as the dollar index remained essentially flat. The currency had its biggest gain in more than two years on Monday, strengthening 1 percent, and added a further 0.7 percent on Tuesday. (It retreated on Wednesday and again on Thursday after the chief financial officer of Huawei Technologies Co. was arrested in Canada at the U.S.’s request, enraging China.)

While we can’t say for sure that Beijing is manipulating the currency for diplomatic purposes, it certainly has all the appearances of doing so. When trying to avoid tariffs, it keeps the yuan artificially high. When trying to mitigate the impact of tariffs, it weakens the currency. Trying to convince Trump of China’s goodwill, it pushes the yuan back up.

What makes all this currency kabuki theater so notable is how little it gains Beijing. Trump believes, incorrectly, that this manipulation is aimed at boosting China’s trade. U.S. negotiators, meanwhile, are unlikely to be swayed by a one-week or one-month movement.

The fundamental problem is partly Washington’s lack of trust in Beijing to execute a policy. The CFETS pricing basket isn’t perfect in U.S. eyes. But adhering to it would serve China better than this continued trade-war gamesmanship.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Christopher Balding is a former associate professor of business and economics at the HSBC Business School in Shenzhen and author of "Sovereign Wealth Funds: The New Intersection of Money and Power."

©2018 Bloomberg L.P.