China’s Trying to Break Addiction to Corporate Bank Loans

China is strengthening efforts to encourage direct financing of companies in financial system that’s long been dominated by banks

(Bloomberg) --

China is strengthening efforts to encourage direct financing of companies in a financial system that’s long been dominated by banks, as the private sector struggles with access to credit.

Regulators in recent months relaxed rules for companies seeking listings on China’s stock markets, moving toward a registration-based system that in theory automatically green-lights applicants provided they meet set criteria. While regulators still demand case-by-case reviews for bond sales, a legal amendment to be rolled out March 1 calls for “sharply simplifying” the requirements.

The moves are part of a broader initiative to raise the sophistication of the nation’s capital markets. The campaign includes letting overseas asset managers apply for mutual-fund licenses from April, and new legal guidance on bondholders’ rights. At stake for the private sector is broadening access to credit beyond banks, which tend to favor state-owned enterprises.

“China has been pushing for more direct financing for years but we’ve noticed a stronger tone on that front lately,” said Gao Ting, head of research at Nomura Orient International Securities Co. in Shanghai. “China’s economy is still faced with big downward pressures so regulators sense the urgency.”

Economic growth in China has been squeezed the past couple years both by the trade war with the U.S. and policy makers’ moves to shrink the shadow financing sector. The clampdown on leverage has particularly hit private enterprises, which had tapped into China’s swelling wealth management products to fund growth. A clean-up of regional banks has also put the squeeze on smaller private firms.

Noise from Washington about potentially making it tougher for Chinese firms to raise capital in the U.S. have only added to the impetus to develop China’s own stock markets. The latest developments came in late December, when China’s legislature approved revisions to the nation’s Securities Law, easing up on rules for companies to list on stock exchanges.

Issuance Surge

This year could see 260 to 320 new listings, raising as much as 380 billion yuan ($55 billion) across four different domestic venues, according to projections by Deloitte LLP. That would mark a surge from 201 initial public offerings raising about $38 billion last year, according to data compiled by Bloomberg.

The shift to a registration-based system has been years in the making. The China Securities Regulatory Commission previously served as the gatekeeper for offerings, with a seven-person listing-review committee examining each application. Under a registration system, questions of IPO supply and timing are left to companies and the market, rather than regulators.

Relaxed controls were also announced late last year for secondary share sales, at least for those on ChiNext, a market focused on small-cap stocks. That could help stoke a rebound since squeeze on share placements was enacted in 2017 to help reduce pressure on the equity market at the time.

Foreign Cap

On the demand side, China is now looking at letting foreign investors buy bigger shares of the nation’s domestic equities. Fang Xinghai, vice chairman of the CSRC, said this week. There’s potential to lift the limit beyond 30%.

“While not immune from the vagaries or highly sentiment-reliant equity behavior often present in emerging markets, China’s equity market has expanded rapidly and China is working to professionalize its investor base,” said Hannah Anderson, Global Market Strategist at JPMorgan Asset Management. “Efforts are further along on the equity side than they are on the bond side,” she said.

When it comes to bonds, issuance is still on a case-by-case approval basis for much of China’s market. After the national legislature’s Dec. 28 announcement, all eyes will be on the scheduled March 1 roll-out of the Securities Law amendments -- which called for streamlining pre-requisites for bond sales and eliminating “approval committees” at the regulatory agencies that oversee them.

Demand Base

A bigger challenge is encouraging a diversified ownership base for China’s corporate bonds, including the budding domestic mutual-fund industry along with overseas investors.

“We’ve had a build-up of debt in the past decade, and that has lumbered the banks with some burden on their balance sheets,” said Timothy Moe, chief Asia-Pacific strategist at Goldman Sachs Group Inc. That “suggests that China’s financing model of banks financing the majority of capital needs to shift to include a greater focus on capital markets,” he said at a conference earlier this week.

Many borrowers, such as property developers, faced with limited options at home have been raising dollar debt offshore. But China has been working to develop its domestic bond market, the world’s second-largest at $13 trillion. Along with reforms to open up foreign buyers, regulators in the past year moved to welcome overseas ratings agencies and underwriters.

David Chin, China country head for UBS Group AG, highlights two stark differences between China and developed markets.

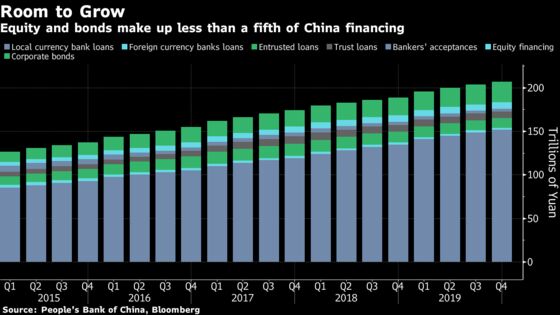

“One is the size of direct financing (equities and bonds) is dwarfed by the size of bank lending, and the other is the retail portion of the stock market, which is about 80% versus 20% institutional,” he says. “Both of these two, over decades, will become more like mature markets overseas. But it will take a long time.”

--With assistance from Irene Huang, Shen Hong and Annie Lee.

To contact Bloomberg News staff for this story: Amanda Wang in Shanghai at twang234@bloomberg.net;Lucille Liu in Beijing at xliu621@bloomberg.net

To contact the editors responsible for this story: Sofia Horta e Costa at shortaecosta@bloomberg.net, Christopher Anstey, David Watkins

©2020 Bloomberg L.P.

With assistance from Bloomberg