China’s ‘Too Sudden’ Bond Selloff Is at Mercy of Stock Rally

China’s ‘Too Fast, Too Sudden’ Bond Rout at Mercy of Stock Rally

(Bloomberg) -- A brutal selloff that’s made China’s government bonds one of the world’s worst performers is showing no signs of ending any time soon.

That’s because the chances of significant monetary easing from the country’s central bank are becoming even more remote, as recent stock market gains raise government concerns over the risk of an equity bubble. Beijing will want to avoid the kind of debt-fueled stock binge that ended chaotically five years ago, which was partly encouraged by cheap and plentiful money in the financial system.

China’s 10-year government bond yield rose the most since late 2016 on July 6, helping make the notes the world’s third-worst performer the past week through Thursday-- when the trading volume of futures on the debt jumped to the highest level on record. The rout comes at a time when the bonds are already under pressure from a surge in issuance and Beijing’s cautious approach to liquidity. Sovereign notes became the cheapest relative to equities in two years.

“The stock rally and bond tumble exceeded my expectations -- they were too fast, too sudden, and the past week feels like half a year,” said Ji Tianhe, a strategist at BNP Paribas SA in Beijing. He forecasts that the 10-year yield will continue climbing and match last year’s high of around 3.4% in coming months. “The central bank will refrain from major easing due to the advance in equities,” he said.

With further issuance on the horizon, the declining trend in price looks set to continue. The notes should be avoided for now, say analysts from BNP Paribas and ANZ Bank China Co. The yield on China’s 10-year government bonds has jumped 15 basis points this week to 3.06% as of Friday morning.

Here’s a look at the factors challenging the bond market:

Stock Rally

The tumble in debt mirrors a rally in equities. Stock trading turnover has soared, margin debt has grown at the fastest pace since 2015 and online trading platforms have struggled to keep up. Bullish articles in state-run media spurred the mood.

The recent advance has made it even harder for the People’s Bank of China to ease -- lower funding costs also make it cheaper for investors to load up on debt and buy stocks. Loose monetary policy was one driver behind the 2015 bubble, the bursting of which wiped out $5 trillion of equity value.

“The rally in equities has disrupted China’s monetary policy. Now Beijing can’t send out a strong easing signal as that will create a stock bubble,” said Xing Zhaopeng, a markets economist at ANZ. “We won’t likely see any major easing measures over the next month, and that will be bad news for bonds.”

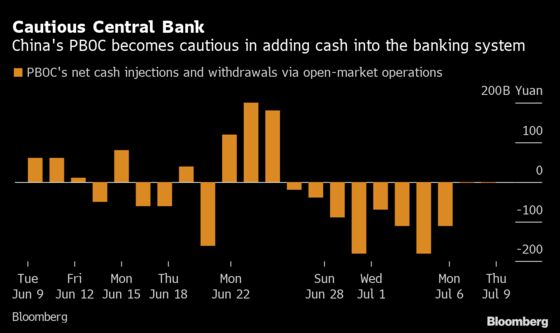

PBOC Caution

The central bank has repeatedly disappointed the market by not loosening its monetary policy aggressively. It has refrained from cutting the amount of cash lenders need to set aside as reserves, despite Beijing signaling last month that such an easing measure could be used. The PBOC in the past three days maintained a neutral position after draining cash from the financial system for eight straight sessions, exacerbating concerns over a liquidity shortage.

Still, analysts see an inflection point when the spike in government yields begin to hurt the economy, which may trigger action from the central bank. Collateral damage from the slumping sovereign-bond market is already roiling the credit market, where companies are shelving plans to sell debt as borrowing costs surge. They canceled about $11 billion worth of deals in June alone, according to data compiled by Bloomberg.

“The 10-year yield will fluctuate above 3% for a while,” said Chen Qi, chief strategist at private fund management company Shanghai Silver Leaf Investment Co. She added that while the PBOC will maintain an easing bias, the era of very loose monetary policy has passed.

| Read more about China’s economy and markets here: |

|---|

| All Eyes on China’s Unstoppable Stocks After $460 Billion Rally |

| Chinese Firms Rush to Cancel New Bond Plans as Yields Surge (1) |

| PBOC Keeps Tighter Liquidity Leash as Economy Recovers |

| China’s Tumbling Bond Market Needs a Big Liquidity Injection (2) |

Spike in Issuance

By the end of July, the central government intends to sell 1 trillion yuan ($143 billion) of so-called special notes, with the proceeds put toward fighting the virus outbreak. Banks will have the incentive to preserve cash to buy these higher-yielding securities, meaning China’s sovereign notes will suffer from the issuance increase. More debt is expected to hit the market in August and September, as regional authorities unleash their own launches delayed by the special bonds, meaning pressure on sovereign notes should persist throughout the third quarter.

©2020 Bloomberg L.P.

With assistance from Bloomberg