(Bloomberg Opinion) -- The logic behind China’s decision to ask its state-owned enterprises to halt imports of U.S. farm goods would, at one level, seem blindingly obvious. Leaders in Beijing may have a more complex game in mind, though.

After U.S. President Donald Trump last week threatened to impose tariffs on another $300 billion of Chinese imports, in large part because China had supposedly reneged on a promise to ramp up agricultural purchases, President Xi Jinping could hardly afford to look like he was bending before the pressure. Chinese state agricultural firms will wait to see how trade talks progress before resuming purchases from the U.S., people familiar with the situation told Bloomberg News Monday.

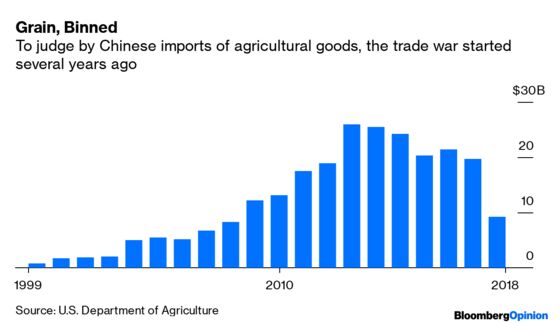

Economically, this was one of the easiest decisions Xi could possibly have made. The fact is that agricultural trade between the two nations has been declining since well before Trump launched his trade war. U.S. farm exports to China peaked all the way back in 2012.

Exclude the wood, paper and pulp industries, where trade has remained fairly constant, and the decline is even more dramatic: The $13.93 billion China imported in 2018 was barely more than half the $25 billion in 2014.

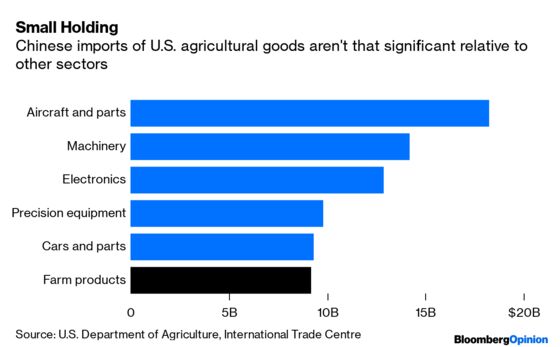

China pointedly isn’t making similar threats over aircraft, machinery, electronics, precision equipment and cars. Each accounts for a larger share of imports than farm goods but are far more difficult to replace using other suppliers.

The de facto ban has the additional benefit of maximizing political impact. President Donald Trump has made no secret of the fact that farm trade is close to his heart – hardly surprising, given how important swing states in the Midwest grain belt such as Iowa and Wisconsin were to his 2016 election victory. Chinese agricultural purchases were the most well-trailed part of the pact that Trump’s trade negotiators were working on before the talks blew up in May and Trump appears to regard resuming them as more or less a precondition to any further agreement.

Making a show of cutting this particular area of bilateral trade at a time when the American farmer is reeling from the after-effects of this year’s floods is a potent way for Beijing to jab its fingers in Washington’s eyes. (Today’s decision to let the yuan weaken past 7 to the dollar should similarly support Chinese exports and worsen the U.S. trade deficit that Trump cares so much about.)

The move could be more than a short-term attempt to lash out, however. When negotiations appeared to be making progress, China was only too happy to hint that it would beef up its farm purchases. But any trade discussion ultimately comes down to a bargain. By withdrawing apparent concessions now, Beijing is creating chips it can trade away again at a future date.

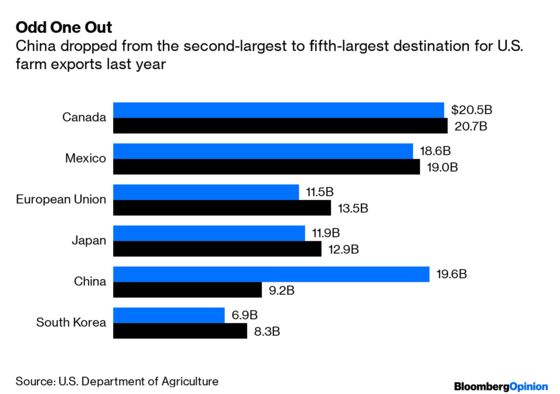

For all that China is a relatively slight importer of U.S. farm commodities -- behind Canada, Mexico, the European Union and Japan in the already trade-war affected 2018, and only just ahead of South Korea -- its potential is still enormous. Removing all barriers could lift the value of U.S. agricultural exports to China by $53 billion, twice the size of the $25 billion import trade in 2014 and enough to increase overall overseas purchases from U.S. farms by half, according to a study last year led by Minghao Li of Iowa State University.

That’s quite the carrot. At this point, even if trade talks do resume as scheduled in September, the chances of China agreeing to the kind of long-term structural reforms the U.S. has been demanding appear to be fading. Xi may be betting that Trump, desperate for a win on the campaign trail, will at some point agree to a smaller deal focused primarily on concrete Chinese purchases he can tout. Opening the checkbook then should be as easy as closing it now.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.