China’s Slowdown Tests Central Bank Amid Debate Over Easing

China’s Slowdown Tests Central Bank as Debate Rages Over Easing

(Bloomberg) -- China’s marked economic slowdown in the second half of the year is testing the central bank’s policy mettle and dividing economists over whether more aggressive action is needed to avoid a deeper downturn.

The People’s Bank of China is having to juggle multiple economic risks, pulling policy in different directions. Growth is heading for lows not seen since 1990 -- if last year’s pandemic year is excluded -- factory-gate inflation is soaring, while the currency is rallying on the back of record trade surpluses.

On top of that, the U.S. and Europe’s imminent scaling back of pandemic stimulus is squeezing China’s room to loosen policy.

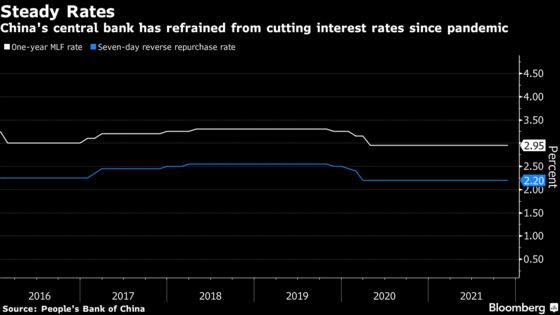

The PBOC has refrained from any significant easing measures since its surprise cut in the reserve requirement ratio in July. It’s opted instead for a targeted approach: providing support to small businesses and green sectors, and relaxing some restrictions on property financing and mortgage lending.

The State Council, China’s cabinet, said in a statement Monday the PBOC and regulators should use various financial tools to boost liquidity to smaller businesses. Premier Li Keqiang also echoed those sentiments Monday, saying the economy faces “new downward pressure” and the focus should be on supporting small firms.

The central bank is now signaling an easing bias again, highlighting concerns about the domestic growth outlook in its latest quarterly monetary policy report published on Nov. 19.

Yet there’s much disagreement among analysts about how much pain Beijing will tolerate before stepping in.

| Read More on the Topic: |

|---|

|

Some economists, like Citigroup Inc.’s Liu Li-gang, see a strong case for aggressive action, including more RRR cuts and a reduction in policy interest rates to arrest the slowdown and avoid a “hard landing” in the property sector. Citi trimmed its growth forecast for 2022 to 4.7% from 4.9% on Tuesday, and predicted no property investment expansion next year.

Many analysts, however, argue the economy’s problems are structural, and broad easing would only inflate bubbles and harm the authorities’ effort to correct the property market.

“The easing polices will be mild and will be targeted next year,” said Liu Peiqian, China economist at NatWest Group Plc. “Given the ongoing firm stance on property sector deleveraging, I expect monetary policy easing to be more targeted to support green financing and small and medium-sized enterprises.”

Here’s a look at the diverging views from analysts on the various monetary policy options going forward:

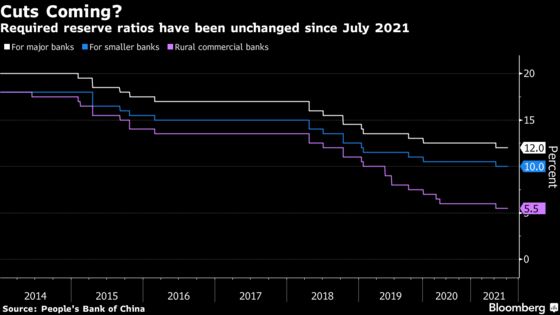

RRR Cut

Many analysts have dialed down their expectation for another RRR cut in recent months given the acceleration in inflation and Beijing’s preference for policy “fine-tuning.”

The chance of a reduction by the end of 2021 “has become slim” since the PBOC appears to have chosen to manage liquidity via shorter-term tools, according to Frances Cheung, a rates strategist at Oversea-Chinese Banking Corp.

Nathan Chow, a senior economist at DBS Group Holdings Ltd. agrees that RRR cut by year end is “unlikely,” as does Zhou Hao, senior emerging markets economist at CommerzBank AG.

Those who still predict a RRR cut, like Ding Shuang, Standard Chartered Plc’s chief economist for Greater China, say the fourth quarter will be the PBOC’s last window to do so, given the RRR for smaller banks is already quite low and its use as a regular channel for liquidity injection in the future is limited.

What Bloomberg Economics Says...

The latest monetary policy report “indicates the PBOC intends to cushion the impact of potential liquidity tightness stemming from the Fed’s upcoming taper and following tightening.”

“This reflects the current state of China’s economy -- sluggish growth means further monetary easing is warranted.” Bloomberg Economics expects a 50 basis-point cut in the RRR in coming months.

David Qu, China economist

For the full report, click here.

Pantheon Macroeconomics says a reduction in the fourth quarter is needed to maintain liquidity conditions, while Citigroup sees a strong case for a 50-basis point cut in the first quarter of 2022.

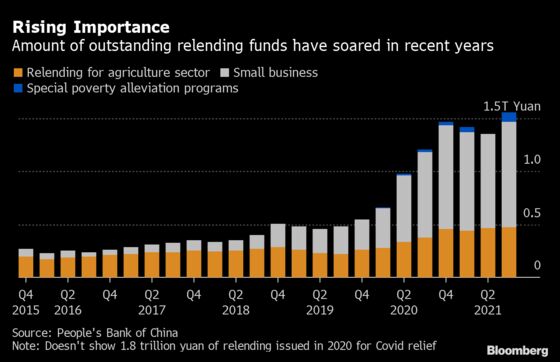

Structural Tools

The decarbonization relending program could unleash 3.3 trillion yuan ($517 billion) of funding next year, according to Li Chao, chief economist at Zheshang Securities Co. Ltd. Mortgage policy for first-time buyers could also relax, which will boost credit growth and support the economy in the first quarter, he said.

On top of existing programs, the PBOC could encourage banks with large U.S. dollar deposits to directly lend dollar loans to property developers with large dollar debt obligations, which can prevent default risk contagion in the offshore credit market, according to Citi economists led by Liu.

Policy Rate

Most analysts expect key policy interest rates -- including the seven-day reverse repurchase rate and the medium-term lending facility rate -- will remain unchanged in coming months. Outliers include Capital Economics Ltd., which predicts the PBOC will start to lower rates by the end of this year and further next year, to result in a 50 basis-point cut in total. Citi also sees a 25 basis-point cut in the second quarter of 2022.

“The possibility of a rate cut still exists when the economy’s downward pressure magnifies in the year end and the first half of next year,” said Bruce Pang, head of macro and strategy research at China Renaissance Securities Hong Kong Ltd.

The Securities Daily also highlighted the debate over interest rate cuts on Tuesday, saying. It cited Wang Qing, chief analyst at Golden Credit Rating International Co., as saying the PBOC is less likely to cut the MLF rate this year, but the loan prime rate may trend lower if it opts to cut the required reserve ratio for banks.

Ming Ming at Citic Securities Co. Ltd. said the PBOC will keep liquidity “reasonably ample” via open market and MLF operations in the short term rather than cutting the RRR, according to the newspaper report.

Liquidity Operations

The PBOC is likely to maintain liquidity support via open-market operations, according to Mitul Kotecha, chief Emerging Asia and Europe strategist at Toronto-Dominion Bank. Cheung of OCBC predicts another rollover of medium-term lending facility funds in December in the absence of a RRR cut.

©2021 Bloomberg L.P.

With assistance from Bloomberg