China’s Risky Wealth Products Gain Appeal in Low Rates Era

China’s Risky Wealth Products Gain New Appeal in Low Rates Era

(Bloomberg) --

One notable consequence of China’s efforts to stimulate economic growth: companies now have a strong incentive to make risky investments.

Record-low interest rates propagated by the People’s Bank of China are creating a quirk in the corporate borrowing system. Yields are so low in the country’s short-term debt market -- with one company this month selling bonds as cheaply as 1.74% -- that some firms may be issuing debt and using the proceeds to buy high-yielding asset management products, according to BNP Paribas SA and Citic Securities Co.

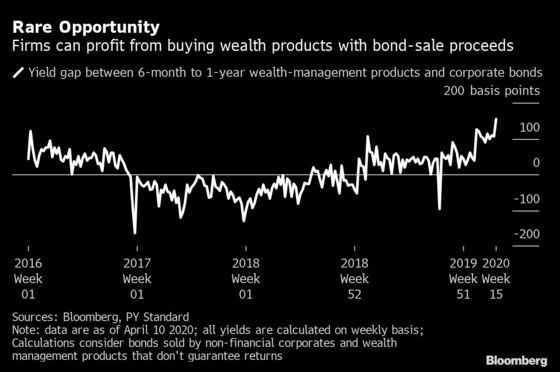

The charts show it’s a profitable trade: the yield gap between short-term corporate debt and banks’ wealth contracts was this month the widest since at least 2016. The products typically buy assets like junk debt to maintain high returns.

While there’s little evidence that the practice is widespread, the mere opportunity reveals the challenges China faces ensuring liquidity makes its way into the real economy. And as the outlook for most businesses around the world becomes increasingly murky, raising cash to invest in a new factory or hire more employees may not seem like an attractive option for management right now.

“Companies are pessimistic about the economy, so they refrain from expansion but save the money at banks,” said Ming Ming, head of fixed-income research at Citic Securities. “This could in turn hurt growth. The yield gap is now at an abnormal level.”

The yield spread between wealth management products due in six months to a year and corporate bonds of the same tenor has expanded to 155 basis points in April, according to calculations based on Bloomberg and PY Standard data. That’s about three times the level seen a year ago.

Meanwhile, the cost of one-year AAA bonds dropped seven basis points to 1.91% Thursday, the lowest level in more than a decade. The PBOC stepped up its monetary loosening on Wednesday, dropping the rate it charges on medium-term loans to an all-time low. That followed its recent cut of the costs on short-term funds, and also a reduction of the amount of cash some banks need to set aside as reserves.

Deploying stronger fiscal policy could discourage the practice by encouraging companies to invest in their businesses, according to Li Qilin, an analyst at Yuekai Securities Co. While Beijing has announced measures including additional infrastructure bond sales and tax breaks for small businesses, the spending pales in comparison to packages unveiled by governments in U.S., Japan or Europe.

“Without strong fiscal support, firms’ motivation to sell bonds and contribute to the economy will remain low,” said Yuekai’s Li. “Companies may get more benefits if they buy wealth management products relative to investing in the real economy.”

Zhang Xu, chief fixed-income analyst at Everbright Securities Co., says most firms will want to tap capital markets to cover their cash shortages. Corporates need to focus on meeting more urgent needs than generating yield, he said, given the impact of the pandemic.

For those tempted to take advantage of the arbitrage window, the returns for wealth contracts remain elevated. That’s because such products usually invest in assets like debt sold by property firms and local government financing vehicles, and sometimes bonds with lower ratings, said David Qu, an economist at Bloomberg Intelligence.

Wealth-management products are building blocks of a shadow-banking system that exists largely off banks’ balance sheets. They have already invested in each other, meaning one soured product could infect others.

By ceding control of the products to brokerages and fund management firms, those institutions have created new layers of products investing in bonds and loans to risky investors. The financial regulators will enforce stricter rules to limit cross-holding of asset management products at the end of this year.

“Corporates will be motivated to do the arbitraging trade due to the yield gap,” said Ji Tianhe, a strategist at BNP Paribas SA in Beijing. He predicts small and medium corporates are more likely to take advantage of the yield gap. “They will benefit as long as the wealth management products don’t default.”

©2020 Bloomberg L.P.

With assistance from Bloomberg