(Bloomberg Opinion) -- So much for deleveraging. China’s biggest shadow lenders are back.

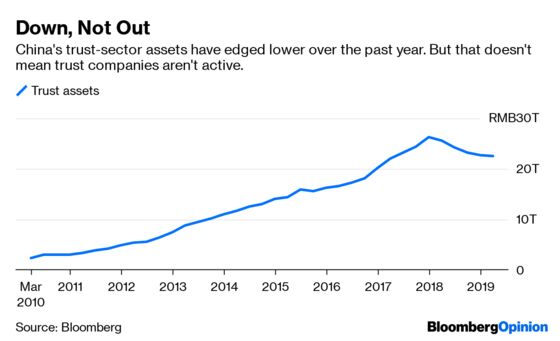

On the surface, it may look like regulators have managed to shrink the role of trust companies, after a wide-ranging, months-long crackdown on China’s financial underbelly. Assets under management at these lightly regulated non-bank financial firms – a hybrid of private equity, asset management and lending – posted their first annual decline last year. Business revenue in the first quarter fell 5% from a year earlier. Broad shadow-banking assets fell 1.2 trillion yuan ($170 billion) in the first three months of this year.

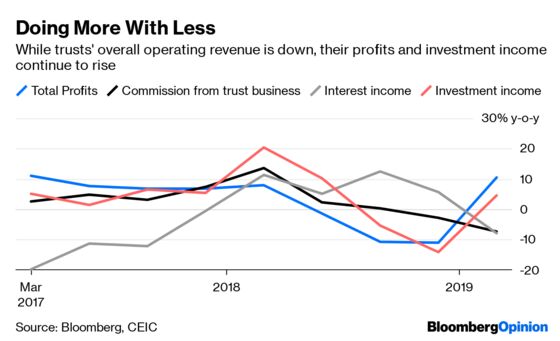

But in reality, trust companies are still in business: Monthly flows of their lending rose more than 90 billion yuan in the first five months of the year. While trust assets in the first quarter fell 0.7% from the previous period, they still stand at a staggering 22.54 trillion yuan. Trust companies’ fee income as a percentage of total assets under management rose for the first time in a decade in 2018, according to UBS Group AG’s Jason Bedford. Total profits in the first quarter rose 10.3% from a year earlier.

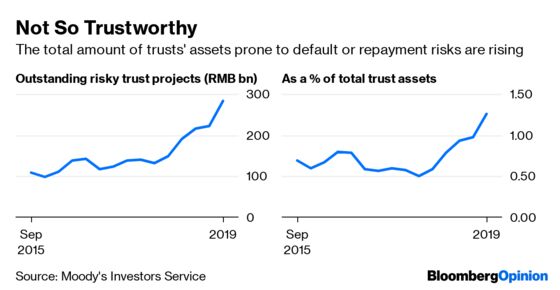

Trust companies are lending directly to parts of the real economy that need it most, beyond bank balance sheets. Financing using trust assets climbed 4.4% in the first quarter, after dropping in the previous three quarters. As this figure rises, the quality of trust assets has deteriorated: The proportion prone to default and repayment risks climbed to a record high of 90% from a year earlier, according to Moody’s Investors Service.

With more complex credit products under regulatory scrutiny, income from so-called actively managed trust assets with higher fees (i.e. loans and other investments) is ticking up. That means firms have even more incentive to push these businesses. In the past, shadow lenders leveraged such investments to juice returns; with the central bank artificially suppressing interbank rates, that could happen again. Analysts have already started discussing whether officials will shift toward even looser monetary conditions in the aftermath of money-market stresses.

The resurgence of trust companies raises two questions: How dependent is China on shadow lenders, and can regulators even get their arms around the 60 trillion yuan ($8.7 trillion) of shadow-banking assets (on paper) – equivalent to 66% of gross domestic product – without kicking off another buildup?

For now, Beijing doesn’t appear to have many options: The fact that activity is picking up even as officials attempt to calm nerves in the interbank funding market shows the economy’s deeply rooted, steadfast reliance on these institutions for credit, especially when banks are flinching.

For years, trust companies worked alongside China’s banks to keep credit flowing in the system. The headline drop in their assets under management has largely come from a decline in trust beneficiary rights products. These are loans put in a trust special-purpose vehicle, which effectively allows banks to reclassify souring debts. Trust companies have also acted as agents between companies lending to each other. Together, so-called entrusted loans and trust loans stood at 20.1 trillion yuan at the end of the first quarter.

Most of trust-backed products are concentrated at regional lenders – the likes of Baoshang Bank Co., which was recently taken over by regulators. In the early part of 2017, such products, in the form of investment receivables, increased between 10% and 40% at smaller banks. At Baoshang, they rose close to 15% and stood at 153 billion yuan, or a quarter of its assets, according to its latest financials.

In theory, this tangle of financing can be unwound. But markets are signaling that there isn’t much tolerance for a bumpy ride. Meanwhile, a sudden hit to credit growth has wider implications that Beijing isn’t prepared to deal with, especially in the short term.

Whether officials can maintain calm as they attempt to clean up a sprawling and opaque financial system is beside the point. What’s clear is that China needs its shadow banks now more than ever.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2019 Bloomberg L.P.