Want to Buy a Car? China’s Got a Deal for You

Beijing is pushing auto financing to boost consumption. Hoping new credit will solve old problems has rarely turned out well.

(Bloomberg Opinion) -- The world’s largest car market is grappling with a sharp slowdown. What’s the best remedy?

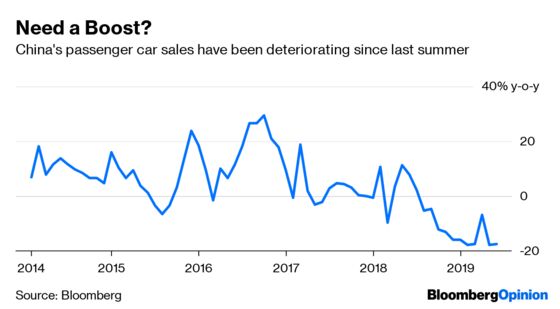

China’s car sales and output have fallen dramatically every month since July 2018. Inventories are piling up, especially for autos that don’t comply with emissions regulations, which will kick in next month for a large part of the country.

Beijing has pulled out all the predictable stops: unrolling consumption-boosting stimulus plans; building out charging stations and intelligent-road networks to encourage electric-vehicle purchases; and making used-car transactions easier. Still, nothing’s really moved the needle yet.

Now, China is making auto financing even more accessible. Given the car sector contributes around 4% to nominal gross domestic product, this makes sense. But with the country’s financial system teetering, the wisdom and timing of this decision is questionable.

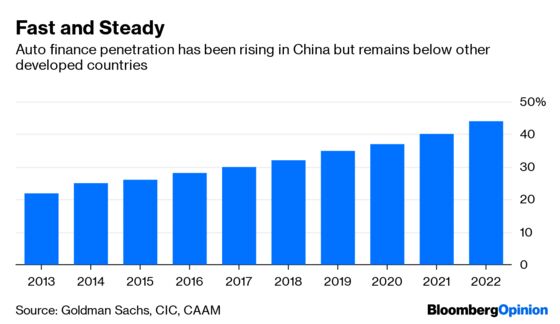

Using credit to boost consumption isn’t unheard of, and China’s auto-financing market is already worth more than 1 trillion yuan ($150 billion). This figure has ballooned in recent years as more consumers turn to lending companies, borrowing platforms and commercial banks to fund vehicle purchases. While the proportion of new car sales backed by auto loans remains relatively low compared with other economies – at around 30% to 40% – it’s growing fast. Some dealers report even higher auto-finance penetration levels. The market is expected to more than double to 2.4 trillion yuan by 2022.

As Beijing cracked down on peer-to-peer lending platforms last year, fears that China’s auto market could face a subprime-like meltdown started surfacing. Many attributed the steep drop in car sales to credit tightening. Yet even as purchases plummeted month after month, auto financing edged up.

So far, that hasn’t been too much of a concern. The biggest beneficiaries of easy lending have been luxury buyers and higher-income borrowers, who stretch their yuan to buy the next best model. These consumers repay their debts on time, if not early. Loan performance has improved and delinquency rates are far from dangerous. The ability to borrow for these folks is an added bonus, not a necessity.

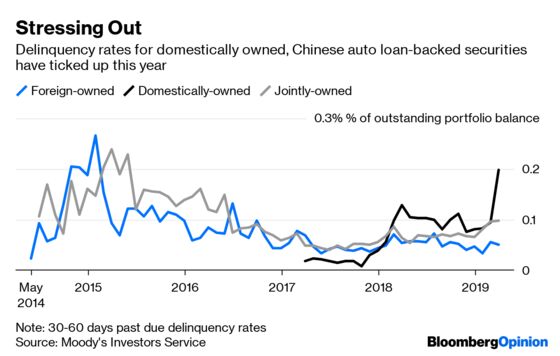

But Beijing’s focus has been on boosting consumption in rural areas, where demand is dipping sharply. Car-ownership levels in these smaller and often poorer cities remain low and buyers are more price sensitive. Auto-finance companies, primarily arms of domestic carmakers, have started extending interest-free loans along with other perks to lure buyers. That’s pushing car loans to weaker borrowers in a weak market. Early signs show that delinquencies are already rising in these regions, albeit from very low levels.

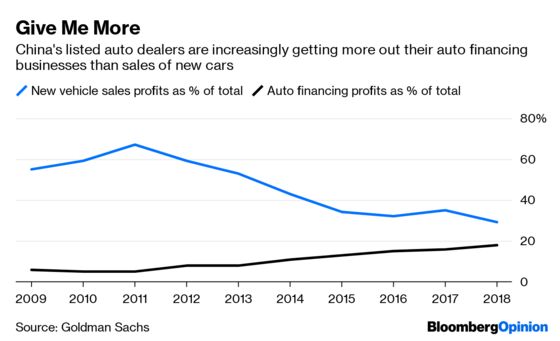

Manufacturers and dealers are also in a tight spot. When car-sales were surging in 2016 and 2017, companies didn’t need their financing arms – they were a nice-to-have growth business. Now that profitability is deteriorating, firms have become more reliant on these units for growth. Another blow to the bottom line came when China’s banking regulator in April said dealers couldn’t collect loan-servicing fees, in a bid to protect consumer rights. After maintaining stringent and conservative loan-to-value standards, lenders are showing more flexibility on borrowing caps and restrictions are getting looser. This comes as Chinese credit markets remain in a precarious state.

With this type of lending on the rise, funding needs are increasing. Securitization of auto loans hit more than 120 billion yuan in 2018, the highest since the market took off. Such asset-backed securities help fund auto-lending companies; unlike banks, they don’t collect retail deposits. Regulators have also encouraged lenders to tap other sources of funding, including borrowing in the interbank market – but that’s just where stresses have been climbing.

There’s also China’s electric-car push to consider. While initially generous subsidies are waning, sales of green vehicles continue to rise. Yet anything consumers actually want to buy or are incentivized to purchase remains expensive. In theory, that would make electric cars a good candidate for auto financing. But there’s a catch: Their credit risk is higher than traditional autos. No one quite knows how long these vehicles last; the faster their technology evolves, the quicker models can become obsolete. “The inherent uncertainty on vehicle value preservation may change the payment behavior of borrowers facing stress,” according to S&P Global Inc.

Yet again, China is returning to credit to solve its problems. In this latest push, Beijing isn’t paving the road to recovery for its auto market so much as getting stuck in old potholes.

Loan value as of 2017, according to Goldman Sachs report citing CIC and the China Association of Automobile Manufacturers.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2019 Bloomberg L.P.