Why China Can’t Get Its Economy Moving

Why China Can’t Get Its Economy Moving

(Bloomberg Opinion) -- China’s new GDP numbers show that the world’s second-biggest economy is growing more slowly than at any time since the early 1990s. Chinese leaders know what they need to do to arrest the slide: pump more credit into private companies, which generate the majority of jobs and growth. The fact that growth isn’t picking up regardless of their efforts would suggest banks are resisting this imperative. But, the issue isn’t whether they’re complying, it’s how they’re choosing to do so.

The government is correct that the private sector’s health is essential to the viability of the overall economy. Private firms account for 80% of jobs, 60% of economic growth and about half of all fiscal revenue in China -- and manage to do so with far lower levels of debt than state-owned companies. Since May 2018, the central bank has thus repeatedly cut banks’ reserve requirement ratios to free up liquidity, then nudged banks to direct that credit toward private firms, especially small- and medium-sized enterprises.

At the same time, authorities have demanded that banks reduce risk which, in a slowing economy, should mean more conservative and market-oriented lending practices. Chinese banks consider small, private companies as the single riskiest group of borrowers in the economy. Unlike state-owned firms, they’re not backed by the government and often don’t have a lot of assets that they can post as security.

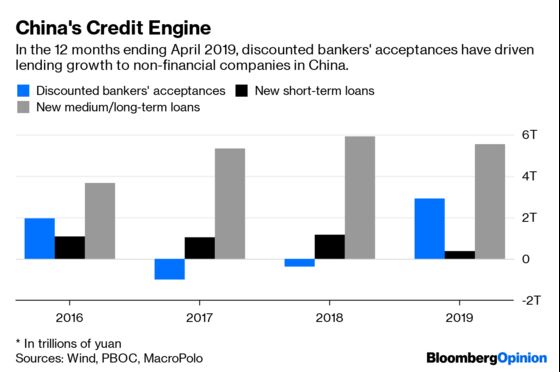

Banks have found a way to balance these competing demands by ramping up a very specific type of lending -- discounting of bankers’ acceptances.

While bankers’ acceptances exist the world over, they play an outsized role in China’s financial system. When a company buys something from a supplier, it can pay using a bankers’ acceptance, issued by a bank on behalf of the buyer. When the acceptance matures at some pre-arranged point in the future, the supplier exchanges it for cash from the bank for the amount of the sale. The bank then seeks payment from the company on whose behalf it issued the acceptance.

Sometimes, however, the company that’s been paid with an acceptance needs money before it’s due. It can then go to any bank and exchange the acceptance for cash, albeit at a discount to the value of the acceptance. In short, discounting is not unlike a low-interest payday loan, with the bank lending against future income. The discount rate is currently about 3.6%, which means that if a company cashes in a 100-yuan acceptance that matures in six months, it will receive a discounted 98.2 yuan from the bank.

For the past year, growth in bank lending to nonfinancial companies has been driven solely by bankers’ acceptance discounting. At the end of April 2019, the outstanding volume of discounted bankers’ acceptances -- what the People’s Bank of China refers to as “paper financing” -- was up 2.92 trillion yuan ($425 billion), or 76%, from a year earlier, accounting for 32% of all new credit created in that period. Meanwhile, new medium- and long-term loans declined 6% over the same period to 5.53 trillion yuan. Short-term loans (which accounted for 4% of new loans) fell 67%.

For banks, discounting seems like a handy solution to their political dilemma. Most of the companies that present acceptances for discounting are small, privately owned firms -- just the kind of companies the government is looking to support. At the same time, discounting is the safest type of corporate loan a bank can make. While the cash goes to a company, the counterparty risk lies with the bank that issued the acceptance.

In effect, discounted bankers’ acceptances are interbank loans. Consequently, the risk-weighted capital that banks need to set aside against them is far less than that required for ordinary corporate loans. That’s particularly useful at a time when the large volume of bad-loan write-offs is making unprecedented demands on bank capital.

What acceptances don’t do, unfortunately, is expand economic activity. As a rule, companies don’t like discounting their acceptances. Many Chinese firms operate on wafer-thin margins, and discounting erodes their profits. Only when they desperately need cash -- to pay wages, bonuses, taxes and social security contributions, utilities and interest on loans -- do they resort to the tactic.

While acceptances are useful as a way of getting cash to companies that are otherwise struggling to stay alive, therefore, they don’t provide either the investment capital or working capital needed to stimulate growth. For that, banks would have to extend real (and far riskier) loans to companies, which they’re still loath to do.

The central bank has supported discounting as the answer to the private sector’s problems. Other branches of the government are less convinced. At the end of June, an official from the National Audit Office said the financing environment for small firms hasn’t “fundamentally improved.” Till now, Chinese policymakers and banks have been able to convince themselves that they can make the country’s financial system safer while also stimulating growth. They may soon have to choose between the two.

To contact the editor responsible for this story: Nisid Hajari at nhajari@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Dinny McMahon is a fellow at MacroPolo, the Paulson Institute's think tank, where he publishes "The Cleanup," a monthly newsletter on efforts to clean up China's financial system. He is the author of "China's Great Wall of Debt."

©2019 Bloomberg L.P.