(Bloomberg Opinion) -- Dismantling the opaque underbelly of China’s financial system is proving far tougher than Beijing could have imagined.

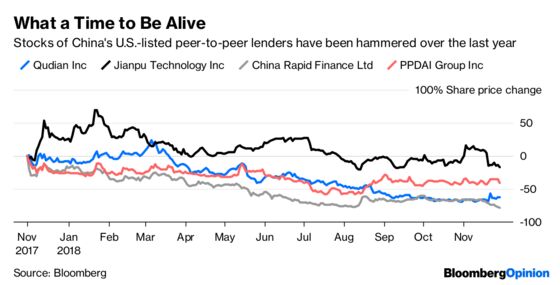

After rolling out a stream of reactive regulatory measures over the past year, authorities are now preparing to effectively phase out the $176 billion peer-to-peer lending market, Bloomberg News reports. Small and medium-size P2P platforms will be wound down, while large ones will probably be asked to rein in lending.

P2P lending was one of several types of informal financing mechanisms that sprang up to satisfy burgeoning demand for consumer debt. Amid lax regulation, they were allowed to proliferate: Loans through such platforms accounted for more than 10 percent of consumer credit at one point. The number of P2P lenders reached 5,000 at the peak in early 2016, with outstanding loans of close to 1.4 trillion yuan ($200 billion). Some of that money was invested in property and corporate bonds.

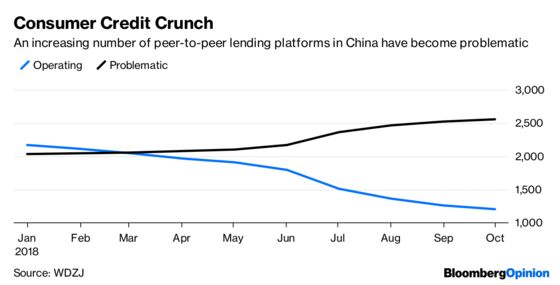

Then the difficulties began. The number of failed lenders rose, causing investments to be wiped out and prompting protests by victims in cities including Beijing. More than half of P2P platforms are considered troubled, according to P2P data provider Wangdaizhijia.

An ensuing blizzard of regulation and consultation papers did little to curb the runaway sector. Directives such as Document 141, issued by online finance regulators, served only to distort the system further. This attempt to regulate online lenders instead saw them morph into “loan facilitators” for banks, primarily rural and small commercial ones. In some cases, the online lenders earned fees while banks took the credit risk; in others, they assumed the credit risk but banks funded the loan.

Having failed to bring the industry into line through rules, Beijing is effectively giving up and just shutting it down.

The P2P market is a microcosm of the government’s challenges with the financial system as it tries to deleverage the economy. Asset managers created almost 30 trillion yuan of shadow credit alongside the already-gargantuan 250 trillion yuan banking system, according to Goldman Sachs Group Inc. The formal banking system funded almost 40 percent of shadow assets. Growth dipped after new asset management rules came into effect earlier this year, but shadow credit remains well above 2016 levels, at more than 25 trillion yuan.

Products and assets have morphed as regulation has come in, but the underbelly remains deeply entrenched.

Besides the slight shrinkage in such non-bank assets, the side effects of deleveraging have been painful. Financial-system liquidity has been squeezed, economic growth has stumbled and borrowing has become difficult. Small companies, especially private ones, are under pressure.

With the credit mechanism becoming less effective every month, Beijing is returning to what it knows best: plain vanilla bank loans and bonds. Banks have been called on to rescue private companies and small-to-medium-size enterprises. Sales of domestic bonds have already surpassed last year’s total.

Untangling the financial system from its shadow twin was always going to be a thorny task. But disabling channels of credit for consumers and companies, rather than restricting or proactively regulating them, may not be the best way. After all, at its peak P2P lending was only about 1 percent of China’s total loan book. A draconian clampdown may also dent consumer confidence and threaten further unrest.

The danger of heavy-handed tactics is that informal lending activities will be forced deeper underground, making risks harder to detect. There are no easy answers to China’s shadow dilemma.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2018 Bloomberg L.P.