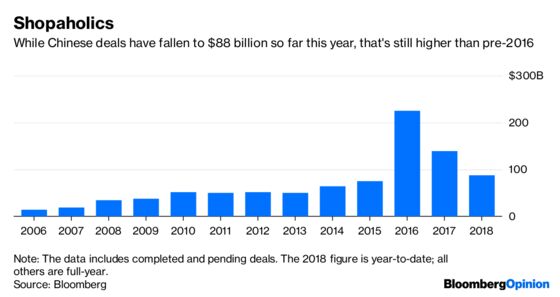

(Bloomberg Opinion) -- You’d be forgiven for thinking Chinese M&A is dead.

Over the past several months, the U.S. has led the charge among developed markets to close mainland buyers out of deals in technology and other sensitive sectors – and scrutiny will only get worse. That’s put a lid on big-ticket acquisitions.

But don’t sound the death knell: Deals are still happening, just ones that slip under the radar. Some are for small amounts in “boring” sectors, like infrastructure, logistics or healthcare. Others are in places like Southeast Asia and India that don’t so much as raise an eyebrow in Washington or Sao Paulo. (Just look at Alibaba Group Holding Ltd.’s investment in Indonesia.) Still others are in unthreatening industries, like Anta Sports Products Ltd.’s bid for the Finnish maker of Wilson tennis rackets.

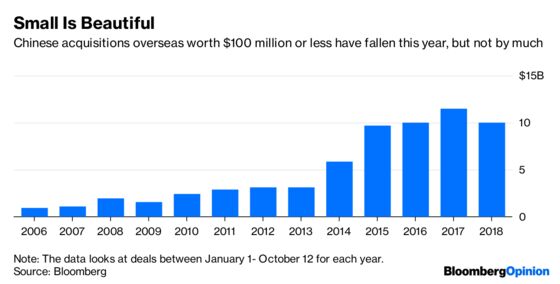

So far in 2018, Chinese buyers have racked up $10 billion of deals worth $100 million or less. While that’s 13 percent lower than the same point last year, it roughly matches the figure in 2016 – China’s blockbuster year for outbound M&A of all amounts – and outpaces every other year in data going back to 2006.

Moving to a low-profile strategy means that certain industries are out. Targets in the natural-resources sector, the object of China’s affections from 2013 to 2015, have stalled. CNOOC Ltd., which forked out $15.1 billion for Canada’s Nexen Inc. at the peak of the commodities cycle, saw its earnings get hammered for years after its splurge.

So are debt-fueled deals, especially in “negative sectors,” those where Beijing considers spending irrational. These days, that includes skyscrapers, hotels and sports clubs. The official line is that the economic rationale behind these deals seems to lie in chalking up capital gains – and moving money out of the country – rather than fundamentals.

HNA Group Co., which unloaded its Hilton Worldwide Holdings Inc. stake earlier in the year, and Anbang Insurance Group Co. were both under the gun for overbuying with debt. Now they’re in the process of reversing those sprees. You’ll start to see “more fundamental deals where there are synergies or a clear China angle,” says Hao Zhou, head of Greater China M&A at Bain & Co., which calls this strategy, “Win at home, export abroad.”

A case in point is the expansion of China’s tech giants into developing markets with growing populations. While these investments may not make money immediately, they offer useful opportunities to scale up and showcase Chinese technology without facing government resistance.

In Brazil, where Didi Chuxing bought 99 Taxis in January, ride-hailers continue to use the target’s app, but the back-end, ride-matching and safety algorithms are now Chinese. Didi has since expanded in Latin America; in April, it launched its service in Mexico, which is run by a team of scientists from China, Silicon Valley and Latin America.

That’s not to say that developed markets are a closed book. With Chinese shoppers driving luxury-sales growth, deals like Shanghai-based Fosun International Ltd.’s purchase of French fashion house Lanvin, and apparel group Shandong Ruyi Group’s acquisition of Switzerland’s Bally International AG have continued apace.

Healthcare deals also seem to get less pushback, if they’re small: China’s Huadong Medicine Co. is moving forward with its purchase of Sinclair Pharma Plc, the London-listed maker of skin-lifting and collagen-stimulation treatments.

Beijing also continues to bless politically expedient deals along President Xi Jinping’s Belt and Road route: BRI-related M&A hit $48.2 billion last year, according to an Ernst & Young report cited by China Daily. Anecdotally, it's easier for a company to get bank funding for these projects than anything else.

The falling yuan, down 8 percent since March against the dollar, may suppress some buying fervor. But it could also prompt more capital flight via M&A, as we saw a couple of years ago – especially now that China’s renewed anti-corruption campaign is rattling the country's wealthy.

For an economy its size, China remains a lot less acquisitive than the headlines suggest: Chinese firms shelled out just 0.6 percent of GDP on overseas acquisitions last year, less than half of what Japan spent, according to Bain. In that light, the Chinese shopper still has plenty of spending to do.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2018 Bloomberg L.P.