(Bloomberg Opinion) -- The world’s fund managers just can’t seem to catch a break.

Pressured by everything from cheap passive funds to burdensome regulations, big asset managers have been pinning their future on China’s growing $15 trillion fund industry. And for a while there, things looked pretty good. Beijing was cracking down on wealth-management products, whose eye-popping returns had propelled erstwhile rivals in the shadow-banking sector. Officials even permitted foreign fund managers and investment banks to control their China joint ventures. Many now await approval for their applications, which they were allowed to submit in April.

Beyond that, there’s been no progress. Meanwhile, the landscape is getting more competitive.

Last month, China made a new rule requiring banks to spin off their wealth-management products into subsidiaries. These units will operate independently from their parent companies, removing the implicit guarantee that boosted the appeal of their products for many savers. Yet the move merely opens another channel for lightly regulated, high-yielding WMPs to proliferate.

So far, around 20 banks have applied to set up these subsidiaries. Four of them — China Construction Bank Corp., Bank of China Ltd., Agricultural Bank of China Ltd. and Bank of Communications Co. — have gotten the green light, though they haven’t started operating yet.

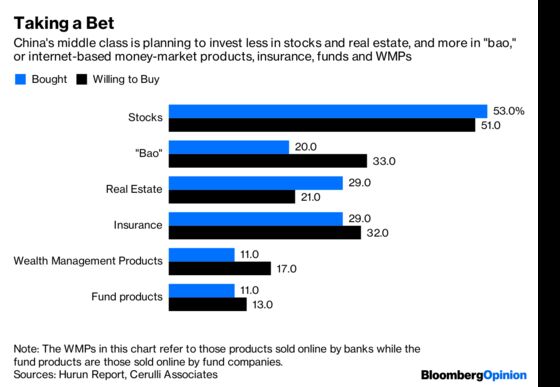

This is bad news for foreign fund managers, who can sell in China only through private funds, pitched to high-net worth individuals and institutions, or via a joint venture with a mainland partner. (BlackRock Inc., which has both, was looking to sell the stake in its tie-up with Bank of China late last year, with plans to launch its own majority-controlled venture, Bloomberg News earlier reported.)

Competition was already intense: Money-market funds like Alibaba Group Holding Ltd.’s Yu’Ebao — one of the world’s largest — have been diverting money from banks and other traditional funds. Soon, Tencent Holdings Ltd.’s WeChat Mini Fund will join the fray.

The challenge for foreign funds is that these new WMP subsidiaries aren’t bound by rules that limit the investment universe of mutual funds and even other WMPs. Unlike mutual funds, which are barred from structured products, as much as 35 percent of these units’ assets under management can go toward such investments. And while most WMPs invest only in fixed-income, the WMPs of these subsidiaries can put money into stocks, says Cerulli Associates analyst Miao Hui.

There are still more headaches for foreign competitors. Like Yu’Ebao and other money-market funds, banks’ WMP subsidiaries won’t have a minimum subscription limit. Buyers won’t need to go to a physical bank branch to inaugurate their first purchases, as is required for current WMPs sold by banks. And those foreign funds with Chinese partners may find them more focused on their wholly owned subsidiaries than the joint venture.

Bottom line: Through their new units, Chinese banks can provide investors more options, more easily.

Perhaps it’s some comfort that only big banks can afford the 1 billion yuan ($148 million) of registered capital such subsidiaries require. Investors wanting more sophisticated products, with mature risk-management systems and brand names, will continue to reach for BlackRock and Fidelity International funds. And the pie is growing: China’s mutual-fund assets under management rose 15.6 percent over the first nine months of 2018 to surpass 13 trillion yuan, while net new inflows were as much as 1.6 trillion yuan, according to Cerulli data.

Private bank wealth management products can invest in equities.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.