(Bloomberg Opinion) -- What consumption downgrade? China’s most prized liquor is roaring back.

Two weeks before the Lunar New Year, consumers are emptying out Kweichow Moutai Co.’s inventory again. On JD.com, one of Moutai’s online retailers, the fiery baijiu costs more than 2,000 yuan ($300) per half-liter bottle, a good 30 percent higher than its 1,499 yuan “suggested retail price.”

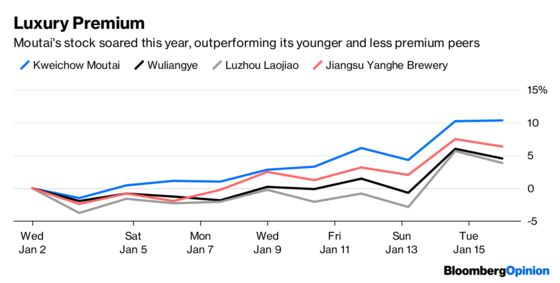

Moutai’s stock price is also on a tear. Its Shenzhen-listed shares are up 12 percent this year, propelled by healthy buying from foreigners through the Hong Kong Stock Connect. Investors are clearly undaunted by China’s economic slowdown, preferring Moutai to its younger and cheaper siblings such as Wuliangye Yibin Co.

Shares of overseas luxury brands from LVMH Moet Hennessy Louis Vuitton SE to Pernod Ricard SA have sold off on concern Chinese demand is weakening. So why should Moutai be immune, considering one bottle costs a month’s salary for a minimum-wage Beijing worker?

One attraction is limited supply. A bottle of Moutai takes five years to brew and thanks to President Xi Jinping’s anti-corruption campaign, which started in 2013, the company is running out of stock. Management has said it will boost volume by 7 percent this year. Even if Moutai wanted to increase production by more, it couldn’t.

This, though, is an old argument. The new story is distribution.

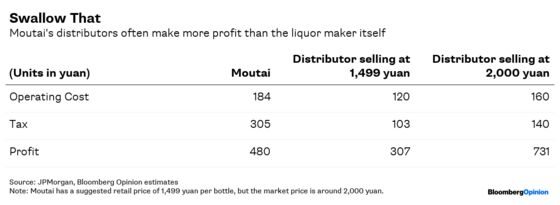

Not surprisingly, the liquor maker is highly lucrative. Moutai sells its core Fetien product to distributors at 969 yuan per bottle, pocketing 480 yuan in after-tax profit. That’s an enviable 50 percent net margin.

Its distributors can make a lot more. Even if they sold at Moutai’s suggested retail price, they would earn a net 308 yuan, JPMorgan Chase & Co. estimates. At 2,000 yuan a bottle, the extra 500 yuan flows directly into the hands of the middlemen – not to Moutai’s bottom line.

This is now Moutai’s main draw: the potential to improve margins. Currently, the company outsources 90 percent of its sales to third-party distributors. On Thursday, the provincial government of Guizhou, where the liquor maker is based, warned officials not to abuse their powers by granting distribution licenses. The local government is Moutai's largest shareholder and relies on the liquor maker for fiscal revenue.

Moutai intends to maintain supplies to existing sellers this year, Chairman Li Baofang told its distributor conference in late December. But the company will sell all its additional output directly, through channels such as exclusive stores and e-commerce platforms. It’s the first time Moutai has talked overtly about a mixed-channel sales strategy, according to Bernstein Research analyst Euan McLeish.

Better distribution can help many of Moutai’s problems to melt away. Wary of its state-owned enterprise status and how its products are well beyond the reach of China’s middle class, the company has said there are no plans to raise its suggested retail price this year. There’s no bar to capturing some of the fat from its distributors, though.

Those third-party seller profits can also provide a measure of insulation against China’s slowdown. Think of it this way. Moutai gets only 969 per bottle, less than 50 percent of what consumers are paying right now. Getting its act together on distribution should enable Moutai to weather any economic storm.

There’s a concern that a government short on cash may impose higher sin taxes on makers of baijiu. But again, such costs pale next to distributors’ profits. Moutai currently pays a baijiu tax of 15 percent, or 145 yuan per Fetien bottle. There’s plenty that can be skimmed off sellers’ margins to cover any tax increase.

The bigger question is whether a lumbering SOE can make a good job of direct sales. Earlier this week, consumers faced a five- to seven-day wait for JD.com to source baijiu. That would be too late for many Chinese needing to travel home before the new year holiday. The supply logjam appeared to have cleared on Thursday.

So Moutai investors can raise a glass to 2019. Unlikely as it might seem, this ultimate luxury brand may prove immune to China’s consumer malaise.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.