Joke Bond Tells Us Nothing About China’s Debt Risk

(Bloomberg Opinion) -- What a difference a year makes. Twelve months on from the fanfare that surrounded China’s first dollar bond sale since 2004, its return to the market is a reminder of how fickle the nation’s policy-making can be.

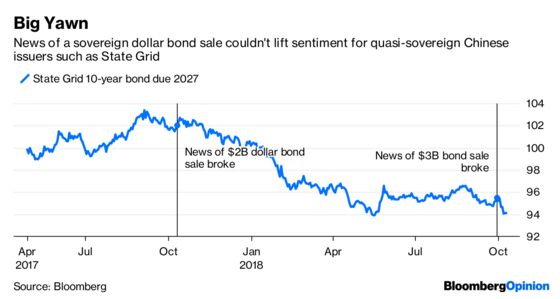

Optimism was in the air when the finance ministry sold $2 billion of notes in October 2017. Quasi-sovereigns such as State Grid Corp. of China saw their dollar securities rally even before the official roadshow. The hope was that the ministry’s new bonds would establish a sovereign benchmark yield curve and lower the cost of overseas borrowing for state-owned companies. The sale ended up pricing at a spread closer to bonds of AAA-rated Germany than the A+ countries such as Japan with which China shared a rating.

Fast forward to now. State Grid’s bonds have been unable to halt their decline since Sept. 28, when Bloomberg News’s Carrie Hong reported plans for a $3 billion sovereign dollar sale. There’s no more appetite for bonds issued by China Inc.

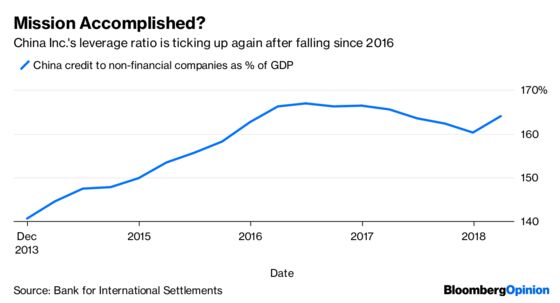

To go by the ministry’s roadshow presentation, everything is blue skies. Bank for International Settlements data show that China Inc.’s leverage ratio rose only 0.4 percentage points to 255.7 percent last year, meaning that it's been “effectively controlled,” the ministry said.

That’s anything but the reality. President Xi Jinping’s deleveraging campaign has gone into reverse. Says who? The Basel-based BIS, the same authority quoted by the finance ministry. The turnaround has halted defaults, making it harder to assess the true level of risk for China’s borrowers.

This was predictable. The drive to control debt championed by Xi at the 19th Communist Party Congress in October 2017 turned into a clumsy operation. China’s 10-year government bond yield climbed quickly after the congress, breaching 4 percent in November. Traders flew into a frenzy, worrying that Beijing’s bureaucrats would follow the top-down directive too earnestly and open the floodgates for defaults.

We questioned then whether soaring borrowing costs were bearable for indebted state-owned enterprises. Sure enough, by May, we started to see a string of defaults, including one by a local government financing vehicle, or LGFV, in Inner Mongolia.

By June, the government appeared to have made a U-turn, after Washington blindsided Beijing with a 25 percent tariff on Chinese imports (the two sides had issued a positive-sounding joint statement days earlier). Payments by debt-strapped LGFVs, including those in technical default, have since been quickly settled. So far, investors haven’t lost money.

But traders also worry when there are no defaults. China has an array of ticking time bombs. LGFVs, the off-budget shell companies that did much of the infrastructure work for municipalities, have amassed at least 30 trillion yuan ($4.3 trillion) of debt, estimates HSBC Holdings Plc. These entities started issuing bonds in 2015, and repayment pressure is building.

Meanwhile, an intense cost squeeze has gripped China’s corporate sector, from the soaring prices of oil and rentals to social-security contributions. A staggering 1 trillion yuan of pledged-share loans due in the second half could also spell refinancing trouble for companies.

External factors are biting hard. The U.S. Federal Reserve has raised rates four times in the past year. Some of the $1.6 trillion invested in emerging-market dollar securities will return to U.S. shores. The escalating U.S.-China trade war will also dent sentiment toward Chinese assets.

To be sure, Beijing will have no trouble selling its $3 billion of bonds – a tiny amount for a $12 trillion economy. Global fund managers that track JPMorgan Chase & Co.’s emerging-markets bond indices will have to buy. Any excess will be swept up by state-owned asset management firms eager to please Beijing.

But this sale, just like last year’s, is a joke. No serious investor will use the issue as an anchor to assess what China Inc.’s real cost of capital should be.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2018 Bloomberg L.P.