As Trade War Hits, China Factories See Slowest Growth Since 2002

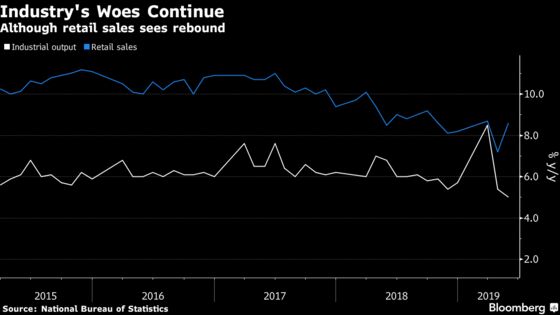

China’s industrial output growth slowed to the weakest pace since 2002, highlighting the headwinds that the economy is facing.

(Bloomberg) -- China’s industrial output growth slowed to the weakest pace since 2002 and investment decelerated, highlighting the headwinds the economy is facing as it grapples with the U.S. tariff war.

Industrial output rose 5% from a year earlier, while fixed-asset investment expanded 5.6% in the first five months. Both were slower than in April and below expectations. Retail sales was a bright spot, expanding 8.6% compared to May last year, partly because a longer May Day holiday encouraged more tourism and spending.

Officials have repeatedly said that the economy is strong enough to overcome the trade war and the central bank governor said recently he had “tremendous” room to adjust monetary policy if the conflict deepens. This continued slowdown may encourage policymakers to use such capacity.

“Beijing will surely step up policy easing measures to arrest the worsening slowdown,’’ said Lu Ting, chief China economist at Nomura Holdings Inc. in Hong Kong. “We expect Beijing to again allow local governments more freedom to scrap some restrictions in property markets to boost growth. We also expect Beijing to allow the yuan to depreciate further if the U.S. government decides to impose the 25% additional tariff on the remaining US$300 billion list.’’

While the government and central bank have unveiled various targeted measures to boost infrastructure spending, support credit growth, cut taxes and increase consumption, so far they have avoided a massive stimulus plan like in previous downturns.

Investment Slowdown

Fixed-asset investment by state-owned and private companies slowed, and there was a fall in investment in eight sectors, according to the data from the National Bureau of Statistics. While property investment slowed, it still grew 11.2 percent in the first five months of the year, with that sector remaining a prop for the broader economy.

What Bloomberg Economists Say:

"The most disconcerting aspect of China’s weak May activity data is the across-the-board deceleration in investment. The production side also notably undershot."

"Looking ahead, the impact of the negative trade shock is likely to intensify in the absence of a clear path to a resolution to the trade war with the U.S."

-- Chang Shu and Qian Wan

See full note here.

“This is substantially weaker than expected” and will likely increase the odds of action from the PBOC in the near future, especially if the results of the G-20 meeting between the U.S. and Chinese leaders is worse than expected, said Becky Liu, head of China macro strategy at Standard Chartered Plc in Hong Kong.

Fluctuations in the data are normal, but external uncertainties are increasing, a spokesperson for the National Bureau of Statistics said after the data was released. China has a large amount of room to increase consumption and added almost 6 million jobs in the first five months of the year, the spokesperson said. The survey-based unemployment stood at 5%, the same as in April.

“China needs more stimulus to keep GDP growing above 6%,” said Iris Pang, an economist at ING Bank N.V. in Hong Kong. “Retail sales was good because it was supported by the long holiday in May. But it could also be a sign that Chinese consumers spent domestically rather than taking leisure trips.”

--With assistance from Tomoko Sato, Jiyeun Lee, Miao Han and Claire Che.

To contact Bloomberg News staff for this story: James Mayger in Beijing at jmayger@bloomberg.net;Xiaoqing Pi in Beijing at xpi1@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, ;Malcolm Scott at mscott23@bloomberg.net, James Mayger

©2019 Bloomberg L.P.

With assistance from Bloomberg