(Bloomberg Opinion) -- China is losing that wow factor.

Another economic growth number with a six in front of it. Another tired superlative about the slowest expansion in three decades. There's going to be a lot of that as China's economy gets bigger, older and loses that emerging-market glamor. Nothing inherently bad about that.

We’ve become so used to China's sway that it's easy to forget its modern economy is just 40 years old. As the Middle Kingdom settles into a pattern resembling a big power’s, it will be common for gross domestic product figures – actual or forecast – to be the lowest in decades. In time, China will eke out a pace that looks slow even by post-2008 U.S. standards.

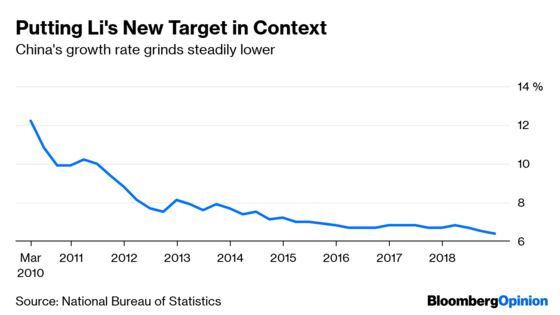

That's one context for looking at the growth goal released Tuesday by Premier Li Keqiang at the National People's Congress. The target is 6 percent to 6.5 percent for 2019, down from about 6.5 percent penciled in last year. Making this a range of outcomes, rather than a specific number, acknowledges that China is cooling from short-term factors within the broader framework of a much longer evolution.

The immediate story: China is buffeted by efforts to shed a legacy of profligate lending and has taken a bit of a hit from the trade war. This will wash out at some point; the trade missiles lobbed over the past year are unlikely to be a regular fixture. Rather than open-slather stimulus to nurse the economy through this cyclical soft patch, Beijing is going for more tailored measures, such as the cut in value-added tax that Li also unveiled. A full-blown interest rate cut, for example, has been resisted.

The longer tale is how China's growth profile falls more into line with that of major economies and onetime emerging markets that have now matured, like South Korea, Taiwan and Singapore. China's expansion will lag emerging markets' and become positively microscopic compared with the double digits fawned over in the early 2000s.

China's real growth rate will be more like 4.5 percent between 2018 and 2022, 2.8 percent from 2023 through 2030 and 1.5 percent in the following decade, Capital Economics projected at a conference in Singapore Tuesday. To put this in perspective, developed economies will hover between 1.6 and 1.8 percent. The OECD made similar points in this paper last year.

That isn't to say Beijing shouldn't loosen the fiscal and monetary reins to smooth out the short-term sag, which is what economies big and small do in moments like these. Relative to past cycles, authorities have been conservative in their response. That's a mature response befitting a maturing country.

China no longer looks like the unstoppable economic juggernaut we saw in the last decade. It has ups and downs, patches of strength and weakness, like other substantial powers.

Report cards that go from beginning with 8-point-something, to 7, to 6 – and eventually to 5 and below – are no longer head-turning. That's the way it should be. It’s what happens when you grow up.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.