China’s Evolving Toolkit to Manage Monetary Policy

China's Evolving Toolkit to Manage Monetary Policy: QuickTake

(Bloomberg) -- China’s monetary policy is in flux, as the central bank tries to weed out risky lending while ensuring money keeps flowing into the economy. To achieve those sometimes competing goals, the People’s Bank of China is engaging liquidity tools and pricing signals, while keeping its historical benchmarks dormant. An added complication: managing the impact of the prolonged trade standoff with the U.S. and calibrating the speed at which it opens the financial system to outsiders. The bigger picture is the PBOC’s transition from being China’s only lender under Mao Zedong to something resembling the Federal Reserve or the European Central Bank -- a modern institution that sets the price of short-term money using interest rates to lend in financial markets. But for now, it’s not clear what that lending benchmark will be. Yi Gang, who took over the reins at the PBOC last year, has signaled faster change, saying the bank may study stopping the release of the current benchmark lending rates -- a step toward making prices more market driven. How soon those changes will start remains unclear. That means investors need to keep watch on a variety of fronts to discern policy direction. Here’s a look at the main items in the PBOC’s evolving toolkit.

Open Market Operations

While OMOs cover a variety of tools, they usually refer to the PBOC offering reverse-repurchase agreements in the open market. The contracts are short-term loans to primary dealers -- mainly major banks -- and are the most common tool to smooth money-market rates. Reverse repo operations are gaining prominence as the PBOC increases the frequency of operations and adds different tenors (the amount of time to maturity). In a broader sense, open market operations also include tools with longer tenors such as central bank bills. Regardless of the tenors, the operations can result in either a net injection or withdrawal of cash from the financial system and hence have an immediate effect on the money market. There has been growing chatter that the central bank is planning to move forward with a long-awaited liberalization of interest rates, eventually scrapping the 1-year benchmark lending rate.

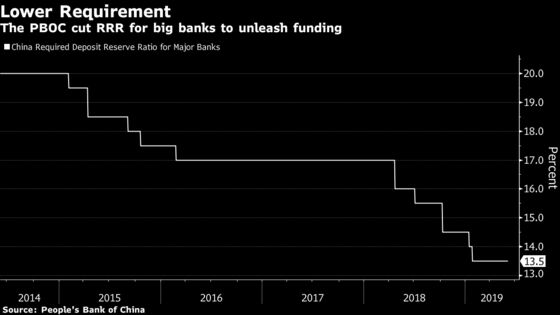

Required Reserve Ratio

A measure of how much cash banks must deposit at the central bank, mainly to ensure they can handle customer withdrawals. In China, it’s also an important means to manage the money supply, especially with the nation’s persistent current account surpluses. While this tool had been eclipsed by innovative methods such as the Medium-term Lending Facility (see below) in recent years, it looks to be returning to favor. In contrast to many of the central bank’s lending tools, a reserve-ratio cut is a nearly cost-free liquidity source for banks. Cuts ensure lenders have cash to dole out to borrowers as the move toward more market-oriented interest rates drives up deposit rates.

Medium-term Lending Facility

The MLF started in 2014 and allows the central bank to provide funds with longer maturities, stabilizing market expectations with tenors ranging from three months to a year. As the funds come with higher interest rates compared with reverse repos, MLFs can ensure adequate funding without flooding the banking system. MLFs also help improve rates transmission in China where financial markets still lack depth, as they set borrowing costs at the longer end of the curve. Outstanding MLF loans declined to nearly 3.6 trillion yuan ($521 billion) by the end of May 2019, as the PBOC turned back to reserve ratio cuts. The central bank conducted the first targeted version of MLF in January, offering funding cheaper than the regular MLF in a move that helps guide lending to small businesses.

Benchmark Interest Rates

The PBOC historically used benchmark lending and deposit rates to set the basic fundraising costs for banks, companies and individuals. These are the most powerful, but bluntest tools in the PBOC’s arsenal, with impact across the entire economy when changed. The rates were last altered in October 2015 and the central bank is now allowing banks some leeway above or below the official rate, as part of its liberalization. According to Yi, the strategy is to gradually "unify" these rates with money market rates, which the central bank controls through other tools.

Balance Sheet

The PBOC’s balance sheet is different in many ways from those of its western peers. With $5 trillion in assets, it’s the world’s biggest. It’s mainly in foreign currency, which the bank bought in large amounts to keep the yuan stable despite a huge trade surplus and capital inflows. As China’s cross-border capital flows become more balanced, the size of this position in foreign exchange will stabilize. For now, that pile forms China’s war chest to manage the currency, a task entrusted to the State Administration of Foreign Exchange, or SAFE.

Rates Corridor

The PBOC is also trying to build an interest-rate corridor that could help reduce central bank intervention in the market, by setting upper and lower bounds. It hasn’t been completely successful. Part of the reason is that the intended upper bound of the corridor -- the Standing Lending Facility, or the Chinese version of U.S. Discount Window -- is only available for larger lenders, and actually asking for access is seen as frowned upon. There have been times that the 7-day repo rate, the short-term borrowing cost of financial institutions, surged beyond the SLF lending rate with the same maturity.

Others

The PBOC has created tools similar to the MLF to offer funding in different scenarios:

- Pledged Supplementary Lending is a program used to fund investment by the nation’s three policy banks in areas including re-developing shantytowns.

- Short-term Liquidity Operation was introduced in 2013, aiming to address temporary fluctuations in the money market. It hasn’t been used in recent years as the central bank moves to daily open-market operations.

- Contingent Reserve Allowance is aimed at providing temporary liquidity to banks during the Chinese New Year holidays, when there is usually a cash shortage because of gift-giving. The tool replaced the Temporary Liquidity Facility, which was used only once last year to ease a cash crunch before the holidays.

The Reference Shelf

- QuickTake explainers on China’s achy economy, the mysteries of China’s economic data and China’s market meddling.

- An explainer on the composition of the PBOC’s balance sheet.

--With assistance from Jeff Kearns and Malcolm Scott.

To contact Bloomberg News staff for this story: Yinan Zhao in Beijing at yzhao300@bloomberg.net;Miao Han in Beijing at mhan22@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, James Mayger, Paul Geitner

©2019 Bloomberg L.P.

With assistance from Bloomberg