The Good News Hidden in China’s Slowing Economy

There’s good news hidden in China’s tumbling stock markets and slowing economy.

(Bloomberg) -- There’s good news hidden in China’s tumbling stock markets and slowing economy.

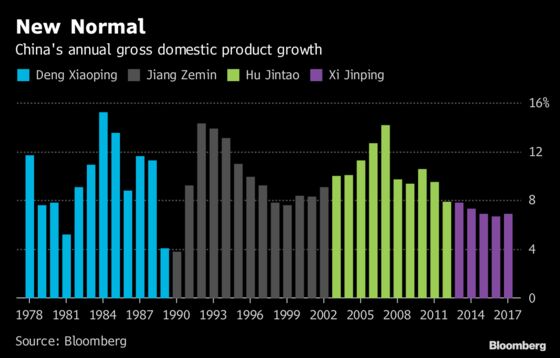

A government bid to curb risky lending, clean up industry, and restrain home prices is holding firm even as growth heads for its slowest annual pace in almost thirty years and the U.S. trade standoff threatens to deepen.

Rather than reaching for the old investment spending and monetary binge playbook of 2009 or 2015, Beijing is cushioning economic blows with targeted tax cuts, investment incentives and efforts to get more credit to efficient private-sector companies. President Xi Jinping may be nudging his nation onto a more sustainable growth path even if it means swallowing some losses along the way.

"Chinese leaders have made impressive initial success in reining in some of the most speculative parts of China’s financial system," said Andrew Polk, co-founder of research firm Trivium China in Beijing. "Many analysts aren’t recognizing these considerable initial gains."

For the world, the prospect of steadier economic growth, even if at a slowed pace, is welcome. And because China is so much bigger than it used to be, 6 percent growth can produce just as much global demand as the double-digit gains of old, meaning China will remain the world’s biggest growth engine.

One dividend from Xi’s policies to rein in excesses is productivity growth, which has risen from an average of about 1.9 percent annually between 2014 to 2016 to about 2.4 percent this year, said Morgan Stanley chief China economist Robin Xing in Hong Kong. Among key factors driving the improvement is the elimination of excess industrial capacity in industries from steel to cement.

Xing estimates the increase of debt will be flat this year, leaving the total ratio at about 276 percent of gross domestic product and says it’s poised to rise about three percentage points in 2019. That compares to annual average 15 percentage point increases between 2007 and 2015.

"It’s the first time China’s policy easing is mainly focused on fiscal rather than monetary policy," said Xing. "They won’t be giving up their hard-earned achievements on leverage and capacity control."

When viewed with a longer lens some of the pain Xi’s policies are inflicting on investors and companies can be seen as a good thing.

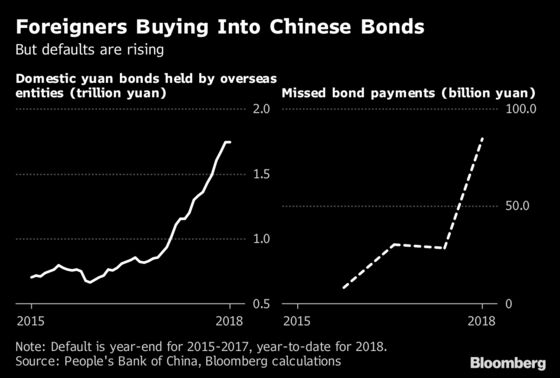

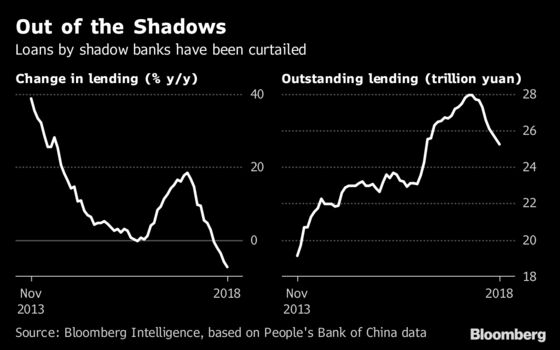

Consider corporate defaults, which are at a record this year as the squeeze on shadow banking continues. The IMF and World Bank have long argued that the removal of implicit guarantees would reduce moral hazard and allow risk to be meaningfully priced. That is starting to happen. As the chart below shows, foreigners are piling into China’s bond market.

Companies are buckling because of a shortage of credit after policy makers cracked down on the previously lightly-regulated shadow-banking sector. And there’s no sign policy makers are letting up: shadow financing shrank for an eighth straight month in October to the lowest since December 2016.

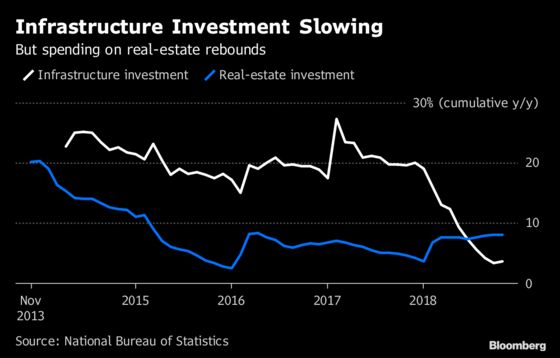

During previous downturns, policy makers used state banks to shovel credit to state-owned enterprises, which was deployed in a spending spree on everything from infrastructure to property and trophy buildings. That’s changed.

The pace of infrastructure investment growth declined to 3.3 percent in the nine months to September from a year earlier -- a record low in data since 2014. While the earlier growth pace was unsustainable, the government wants it to stabilize now. It recovered a tad to 3.7 percent year-to-date last month, signaling that more supportive fiscal policies are beginning to pass through to the real economy.

And while real-estate investment has picked up since the end of last year, it appears under control for now. New-home sales rose at the slowest pace in six months in October, adding to signs that the market is cooling under the weight of policies designed to restrict prices.

"Every time China has been hit by a shock, they’ve panicked and let the credit spigots loose to sustain growth," said David Loevinger, a former China specialist at the U.S. Treasury and now an analyst at fund manager TCW Group Inc. in Los Angeles. "As opposed to the past, the Chinese look like they’re trying to put a floor on growth, rather than engineer a credit-fueled recovery."

As the trade conflict with the U.S. has intensified, policy makers have sought to loosen some monetary settings and eased regulatory requirements on banks to encourage lending, lest the slowdown go too far. Yet while there’s been some speculation among economists that the People’s Bank of China would soon relent and cut benchmark interest rates, that still hasn’t happened.

More: Each round of weak data raises the pressure to give in on stimulus

That could be because the biggest test lies ahead. Donald Trump is poised to hike tariffs to 25 percent from 10 percent on $200 billion of Chinese shipments in January should no ceasefire be agreed with Xi when they meet at a Group-of-20 summit later this month. That would intensify pressure on growth. Things could get worse if Trump delivers on a threat to tariff all Chinese shipments.

The U.S. on Tuesday accused China of continuing a state-backed campaign of intellectual property and technology theft, saying it is involved in cyber-attacks on American companies that were both intensifying and growing in sophistication.

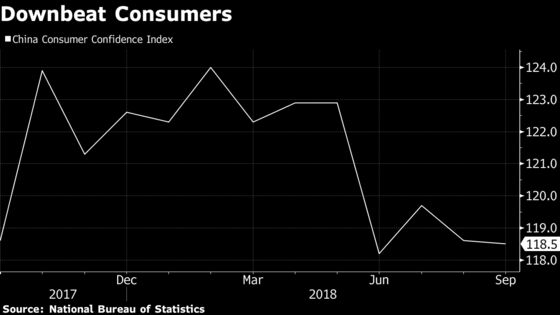

But so far, it’s not the trade war that’s hurting -- indeed shipments have benefited recently as exporters raced to beat the tariffs -- it’s the more downbeat mood of consumers.

For Xi, there is a red line for the slowdown. He needs enough demand to meet the target of creating 11 million jobs a year (already met for 2018) and bottom-line economic growth of about 6.2 percent for the next couple of years to deliver on a pledge that 2020 GDP and income levels would be double those in 2010.

"Policy makers have really changed their tack towards stimulus," Andrew Tilton, chief economist for Asia Pacific at Goldman Sachs in Hong Kong, told Bloomberg Television. "They have reiterated many times that they don’t want to do a 2009-like big bang stimulus and I think this time they mean it."

--With assistance from James Mayger and Matt Turner.

To contact the reporters on this story: Kevin Hamlin in Beijing at khamlin@bloomberg.net;Enda Curran in Hong Kong at ecurran8@bloomberg.net

To contact the editors responsible for this story: Malcolm Scott at mscott23@bloomberg.net;Jeffrey Black at jblack25@bloomberg.net

©2018 Bloomberg L.P.