Is China Really the Economic Juggernaut We Feared?

(Bloomberg Opinion) -- In China's new normal, consider dropping the modifier.

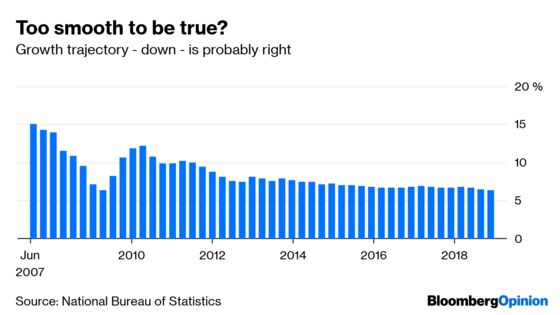

The economy, put charitably, is having some issues. Numbers frequently point to faltering growth and the notion that, just like other major economies, China has a business cycle. That juggernaut we all gushed over – you know, the one that's going to supplant the U.S. – isn’t quite so super after all.

That's one way to view two bits of economic news bookending the week. Premier Li Keqiang's address to the National People's Congress on Tuesday skipped setting a specific growth target, preferring a range of 6 percent to 6.5 percent. That seems to suggest a distinct chill has come to the economy. Come Friday, the buzz was a paper published by the Brookings Institution that said China’s gross domestic product had been overstated for years.

In some respects, the paper played to long-held perceptions that government statistics, especially GDP, are flawed. I've lost count of how many times China cynics have simply cried: “They’re fake anyway!”

Those were the cynics. Others – some deeply versed in Chinese commerce and policy – would more gently steer the discussion toward their preferred gauges of activity. Either way, the performance was said to be unprecedented in their lifetime.

Li himself contributed, perhaps inadvertently, to the cynics’ camp: As an up-and-coming provincial official, he was said to have called the data “man-made,” according to Wikileaks. Bears had a hard time breaking through when China's expansion rates clocked double-digit growth rates or close to it.

Those halcyon days now seem behind us. Fewer people have China on a pedestal. Notwithstanding the cyclical weakness now buffeting China, there is more attention paid to the long-term trajectory of the country's economy. It will continue slowing, ultimately to a rate resembling the U.S.’s now, or even lower. That's what big economies do.

That trend is in place regardless of whether or when China overtakes the U.S. as the world's largest economy by GDP. If the paper’s authors are correct, that point may arrive later than the 2030 timeline usually cited.

The authors also acknowledge that data provided by local governments to the National Bureau of Statistics had some helium. The NBS eventually got a handle on this and adjusted accordingly before releasing the broader quarterly GDP figures.

Sometime around 2008, things began to go off the rails. Local numbers became more inflated, but the NBS didn't revise accordingly. The paper also had some discussion of local officials’ incentives to overstate figures, as well as bureaucratic and political structures that color what gets published.

“Much of the underlying data behind the national accounts is out of the hands of the NBS. Furthermore, the question is what incentives does the NBS [have] to resist local officials who misreport data. Interestingly, although the NBS adjusts downwards local statistics, it does not report the adjusted local statistics, perhaps out of a desire to not confront powerful local leaders.”

To some extent, this is looking through a rearview mirror. One of the defining features of China's recent landscape – aside from its broad slowdown – is the growth of services relative to heavy industry. We'll see what changes that produces; and whether it closes the reliability gap.

So China's model isn't perfect, whatever the shortcomings of Western politics and economics are. As we look back on the week, it's also worth remembering how much the hagiography of China rhymes with the Japan mania of the 1980s and early 1990s.

There’s a lesson. Take trendy ideas with a pinch of salt.

Salute the week.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.