(Bloomberg Opinion) -- In China, some policy-easing measures would be better done discreetly.

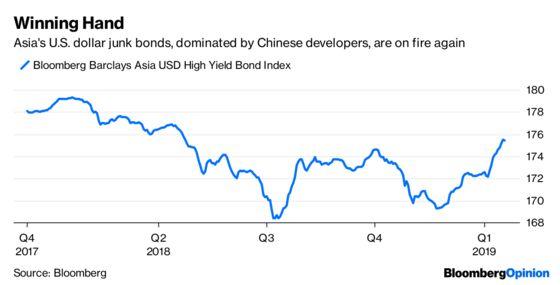

Sentiment toward China’s junk-rated real-estate developers has improved markedly in recent weeks. A few firms, such as Sunac China Holdings Ltd. and China SCE Group Holdings Ltd., were able to sell debt at lower coupon rates than expected. Always thirsty for more financing, China Evergrande Group is coming to market again, hoping to raise billions in a three-tranche offering. Bonds issued by Asia’s riskiest borrowers – mainly Chinese developers – are on their longest winning streak in almost two years.

Murmurs are growing louder that easing measures are coming to China’s property market. Spurred by a more dovish central bank, the average mortgage rate for first-time buyers fell in December, which hasn’t happened in almost two years. A few cities are starting to loosen home-purchase restrictions, long seen as a major obstacle to a boom, by allowing non-residents to buy.

Make no mistake: Any policy overtly seen as giving developers a helping hand is illusory, and won’t be carried out as anticipated.

In late December, Hengyang – a small city (by Chinese standards) of about 8 million that doesn’t even enter the National Bureau of Statistics’ monthly pricing survey – said it would remove price caps on new homes. The announcement fueled media speculation that more local tinkering was on the way. The next day, the city reversed course, saying in a public statement that, “Houses are built to be lived in, not for speculation,” precisely the sentence President Xi Jinping used at the 19th Party Congress in 2017.

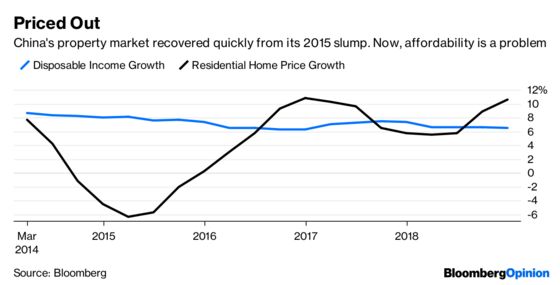

Investors eager for easing would do well to remember how politically sensitive home affordability has become. While household disposable income growth slowed to 6.5 percent in the fourth quarter, from just under 10 percent four years earlier, that hasn’t stopped the cost of homes from soaring. In the last five years, prices in megacities such as Beijing, Shanghai and Shenzhen have more than doubled.

Just like its gross domestic product number, China’s home-price statistics aren't bulletproof. To “smooth out” the data, and diminish any appearance of a market running too hot, developers often procrastinate in submitting online registration of first-home sales. That can mean these figures – and any easing that ensues – could be delayed.

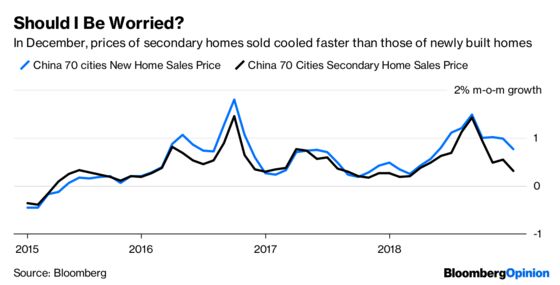

Meanwhile, because the market for secondary home sales is less liquid, prices there may not be all that accurate, either. The two data series diverged recently, with the figure for new homes in tier-1 cities on average up 0.77 percent in December from a month earlier, while secondary sales cooled faster. Last month, 22 out of 70 cities saw declines in their secondary home prices, the most since March 2016.

A bright spot is Beijing’s willingness to allow new U.S. dollar bond issues again. Developers have already sold $5.5 billion of notes in January, on track to fulfill the $15 billion of refinancing needs estimated by HSBC Holdings Plc.

Bulls may say these junk bonds are cheap, now that the market is no longer pricing in rate hikes from the Federal Reserve. Borrowers are paying a much higher spread over U.S. Treasuries than a year ago. But are investors worried about oversupply? Last January, a flood of new bonds from financially savvy players such as Evergrande and Country Garden Holdings Co. was arguably the catalyst that killed Asia's high-yield dollar bond market.

And do keep politics in mind. While Beijing may enthusiastically support 5G’s build-up or car manufacturing, seeing developers thrive is last on its list. Any policy easing will be small and brief.

The option-adjusted spread of Asian dollar junk bonds over U.S. Treasuries was 5.7 percent recently, compared with as low as 2.77 percent a year ago.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.