Look Within for China’s True Growth Threat

Weakness in domestic demand is a bigger danger to the global economy than the trade war with the U.S.

(Bloomberg Opinion) -- Investors and institutions such as the International Monetary Fund are fretting over the risk of a potential global recession caused by the U.S.-China trade war. Their concern is misplaced. The true danger to global growth is the weakness of China’s domestic economy.

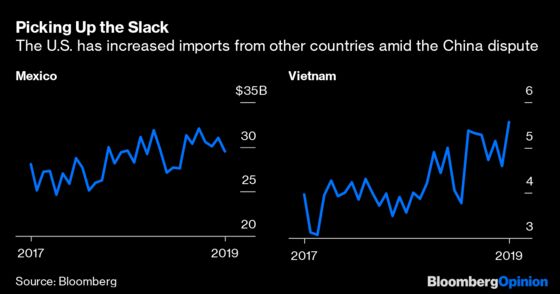

Total U.S. trade isn’t declining. On the contrary, it’s growing at or just beneath its decade-long rate. A decline in shipments to and from China has been offset by increased trade with partners such as Vietnam and Mexico. In a broad global market where goods can easily be substituted, manufacturers will absorb price signals and move to different producers. That’s what is happening, as U.S. tariffs drive up the cost of importing Chinese products. The result is that there has been no net change to global trade levels from the U.S.-China dispute, even if growth has slowed sharply.

The more interesting change is to Chinese trading patterns. Whereas the composition of U.S. purchases remains close to long-term trends, China is showing declines across most product types and geographic partners. Chinese imports from the rest of the world fell 5% this year through September. Why is it showing such a divergence from the U.S.?

There are three specific reasons:

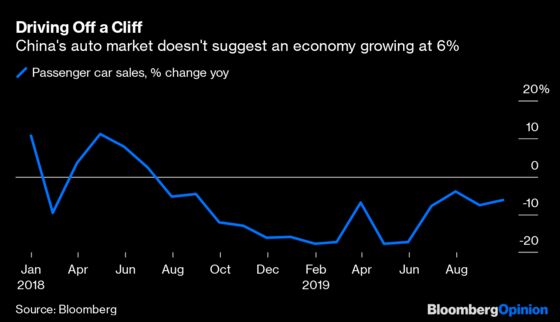

- First, the Chinese economy is growing much more slowly than the headline 6% rate would suggest. Sales of consumer products from smartphones and cars to washing machines are falling or flat-lining. There are similar declines in in specialty traded goods such as Japanese and German precision machinery, which are destined for Chinese markets and not merely as inputs for goods that end up in the U.S.

- Second, there appears to be a conscious plan of import substitution designed to benefit Chinese producers, even when domestic goods cost significantly more. Countries such as Australia produce cheaper iron ore and coal than companies in China. Yet domestic output growth for these commodities has outpaced the increase in imports. Whether in semiconductors or commodities, China is pursuing a plan to move away from imports.

- Third, lack of dollar liquidity is restricting China’s ability to engage in international trade. Leakages have undermined the effectiveness of a foreign-exchange rule that has restricted banks to sending only one dollar abroad for every one they bring in. China’s foreign trade can’t afford just to break even; it needs to generate a significant surplus to cover these leakages.

For years, China drove global demand for many raw materials, accounting for more than 50% of annual growth in output. The subsequent downshift has had an enormous spillover impact. The question for businesses around the world is whether this is a temporary or structural phenomenon. With an excessively indebted economy, slowing growth and a rapidly aging population, it’s almost impossible to see China returning to the pre-2015 rate of expansion.

Headlines about the trade war understandably grab attention but the reality is more mundane and worrisome. Irrespective of what happens to the bilateral trading relationship, the world is coming to the end of China’s rapid-growth era.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Christopher Balding is a former associate professor of business and economics at the HSBC Business School in Shenzhen and author of "Sovereign Wealth Funds: The New Intersection of Money and Power."

©2019 Bloomberg L.P.