China’s Crackdown Will Shake Up World’s Largest Fintech Market

China’s Crackdown Will Shake Up World’s Largest Fintech Market

(Bloomberg) -- In a four-year campaign to root out risks to China’s financial system, regulators have set upon their biggest target yet: the world’s largest financial technology sector.

All three financial watchdogs have made it their primary goal this year to curb the “reckless” push of technology firms into finance, taking aim at a sector where loose oversight fueled breakneck growth for companies such as Ant Group Co. and Tencent Holdings Ltd.’s Wechat Pay. They have the green-light from President Xi Jinping, who in November called on regulators to “dare to” master their supervisory role.

The coordinated onslaught guarantees a shakeup among the country’s more than 7,000 micro lenders. But regulators have made it clear they intend to stretch well beyond, into every corner of internet finance from payments to credit scoring, wealth management to partnerships with banks and more. Fintech is the latest sector marked for an overhaul since 2017, when China’s leaders pledged to clean up threats to its $53 trillion financial industry, tackling property loans, opaque wealth management products and fraud-riddled peer-to-peer lending.

“Everything points to a toughening regulatory stance, which will surely bring more curbs down the road,” said Zhang Xiaoxi, a Beijing-based analyst at Gavekal Dragonomics. “Chinese regulators wouldn’t be comfortable with any financial activities staying outside their purview.”

No punches were pulled in November when authorities squashed the initial public offering of billionaire Jack Ma’s Ant, stunning investors from Shanghai to New York. The world’s most-valuable fintech has become a symbol of the no-holds-barred campaign underway, with Ant executives considering a plan that would make the firm more like a bank, subject to tighter oversight and higher capital requirements.

Authorities have told Ant it needs to get closer to its roots as a provider of payment services, while at the same time putting online transactions under oversight.

China’s central bank last week warned that any firm with more than 50% of the market in online payments or any two with more than two thirds could face antitrust probes and in a worst-case scenario be broken up. Ant’s Alipay and Wechat Pay are the biggest players in mobile payments, though the regulator has yet to clarify how it will judge market share.

Years of a head-to-head rivalry between Ant and Tencent dented profitability of the businesses and transaction growth has fallen to less than 10%, from more than 60% two years ago. Still, the data and user stickiness from payments has enabled the firms to diversify into other financial segments, which are now being put under supervision one after another.

| China’s crackdown so far... |

|---|

November:

|

December:

|

January:

|

Analysts at Citigroup Inc. predict new rules could include a cap on how much financial groups can partner with online lending platforms, and funding and capital requirements. Chen Shujin, an analyst at Jefferies Financial Group Inc., said regulators could also further crack down on their distribution of mutual funds and other wealth management products, standardize calculations on interest rates and force data sharing with the central bank’s credit-scoring system.

The People’s Bank of China said in January that it needs to move fast to fill the gaps in oversight, including banning over-hyped marketing of financial products online and encouragement of excessive borrowing. Guo Wuping, head of consumer protection at the banking regulator, has said easy access to online credit led many low-income and young people to be mired in debt.

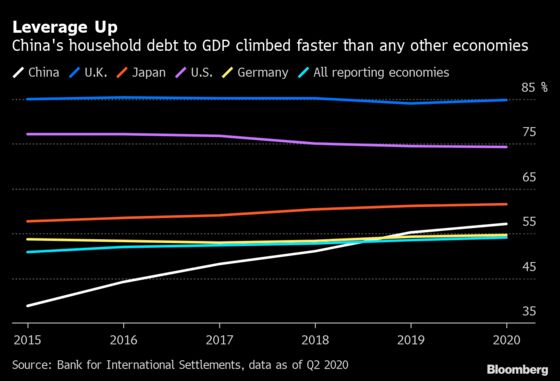

Concerns about surging consumer debt have long unnerved authorities seeking to sustain the nation’s economic rise. Over the past decade, the speed with which Chinese households accumulated leverage surpassed every other major economy, according to the International Monetary Fund.

Consumer loans climbed to a record 49 trillion yuan ($7.6 trillion) in November, stoked by a housing boom and ready access to credit. But the official data doesn’t capture all the risk as loans offered on fintech platforms are mostly uncounted.

Ant has been at the forefront of the boom, providing small, unsecured loans to about 500 million people. Out of the about 1.7 trillion yuan in consumer loans it has underwritten, only about 2% were kept on its balance sheet with the rest with the rest funded by third parties or packaged as securities and sold on.

Its success spurred a crowd of imitators both large and small.

Rival units of Tencent, JD.com, Baidu Inc. and nearly 7,200 other micro-loan operations are scattered across China, nearly twice the 4,000 traditional banks and even surpassing the number of peer-to-peer lending platforms at the peak.

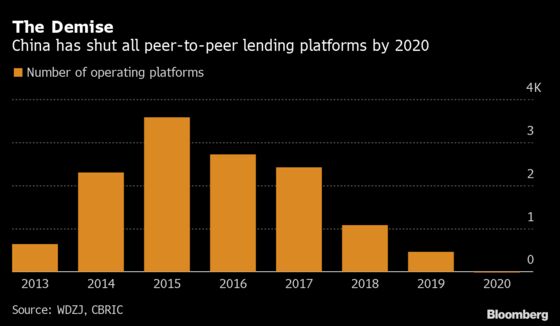

If what happened to the peer-to-peer lending industry is an indicator, the future for the vast majority of those fintech firms is bleak. In just two years, China purged the entire industry, which in its heyday had upwards of $150 billion in loans outstanding and more than 50 million users.

Once hailed as an innovative way to match yield-chasing savers with cash-strapped borrowers, P2Ps proliferated, helping fund everything from honeymoons and property purchase to companies’ working capital. Frauds and defaults became rampant, in some case leading to suicide and street protests.

Jack Ma, who never dabbled in peer-to-peer, attempted to draw a line between the sector and his empire during a speech at the Bund Summit in Shanghai in October. “We can’t dismiss internet technology’s contribution to financial innovation simply because of what happened to P2Ps,” he said.

Once the sector came in for special scrutiny, even the biggest players such as Lufax and Dianrong.com weren’t spared, with the banking regulator saying in November that none of the platforms had survived the clampdown.

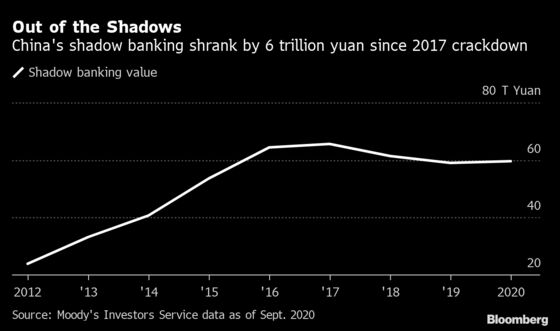

Officials have had a more measured approach to choking off shadow banking -- often loans masquerading as investment products. A lifeline for many small enterprises and property developers shunned by traditional lenders, the sector swelled to $10 trillion at its peak, driving up leverage and interconnectedness across the economy.

A subsequent crackdown shrunk assets managed by a hodge podge of institutions from banks to insurers and trusts by $1 trillion between 2017 and 2019, forcing a record surge in bad loans. The government eased some curbs last year to stabilize the economy after the coronavirus pandemic struck, halting its contraction.

Seen as necessary to ensuring financial and social stability in the world’s second-largest economy, the latest regulatory charge isn’t without risks. Easy access to credit has helped fuel consumer spending, boosting the economy and building wealth. The sweep against fintech firms also comes as officials are trying to make the economy more self-sustaining and they will need consumption and business investing to pull off the shift.

For now, financial stability remains the overarching concern.

“Fintech has not changed the nature of finance as a risky industry,” Deputy Governor Pan Gongsheng said in an op-ed in the Financial Times on Wednesday. “China is trying to strike a balance between encouraging fintech development and preventing financial risks via prudent regulation.”

©2021 Bloomberg L.P.

With assistance from Bloomberg