China Inc. Credit Stress Most Acute in Liaoning, Qinghai

China’s Corporate Credit Stress Most Acute in Liaoning, Qinghai

(Bloomberg) -- China saw a record number of corporate defaults last year and that trend looks set to continue as policy makers try to tighten credit and pull back on stimulus this year.

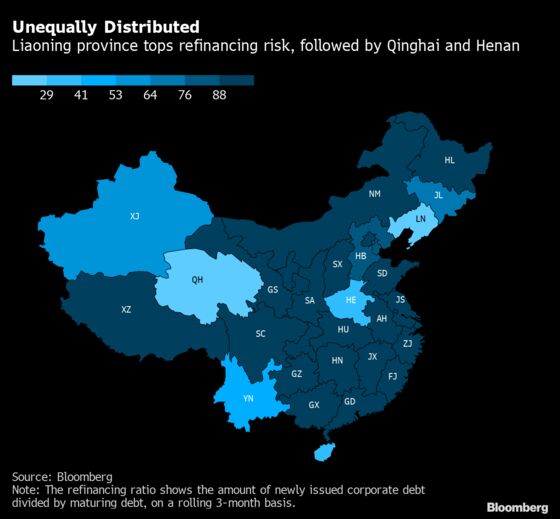

Those stresses aren’t distributed evenly across the country though, with companies in the provinces of Liaoning, Qinghai and Henan facing the most difficulty in raising funds at the moment, according to Bloomberg analysis of all corporate bonds issued in China.

The data shows that firms in those three regions issued new bonds equal to less than 30% of the debt that matured over the last three months. Firms in other provinces such as Anhui and Zhejiang were in a much better position, issuing 251% and 171% more bonds than maturing debt, respectively. The ratio was 116% nationwide in January.

The wide variation between provinces highlights another aspect of the unbalanced nature of China’s recovery, with the richer eastern provinces booming but other areas such as the rust-belt north-east being left behind. Those provinces tend to have weaker government finances, which can limit their ability to help struggling companies and bail-out state-owned enterprises.

“The track record of provincial government’s support to local state-owned enterprises and other companies would be important to look at when evaluating the province’s credit risk”, said Chuanyi Zhou, a credit analyst at Lucror Analytics in Singapore.

Worst Three

As the heartland of China’s rust-belt industrial base, Liaoning province has long been troubled by a weak economy. Almost 4.8% of loans were classed as non-performing at the end of the first quarter of 2019, according to the banking regulator, compared with 1.8% of loans nationwide at that time. Brilliance Auto Group Holdings Co., a large state-owned company, defaulted in November, increasing concerns about the province’s finances.

“Economic development and leverage management are the fundamentals of regional credit metrics,” said Ting Meng, credit analyst at ANZ Bank China Co., adding that those factors “decide the repayment capability.”

Companies in Liaoning only raised enough money to cover 17% of maturing debt over the past three months. Firms in Qinghai were able to replace 22% of maturing debt, and those in Henan borrowed an amount worth 29% of the debt that matured, meaning a large decrease in total credit for these three areas.

Along with Liaoning, both provinces saw defaults at large state-owned enterprises recently, raising questions about the financial resources of the local governments. Energy and mining conglomerate Qinghai Provincial Investment Group Co. defaulted on three dollar bonds last year, while the default of Henan-based coal miner, Yongcheng Coal & Electricity Holding Group Co. was one of a series of credit events late last year that roiled financial markets and prompted the central bank to inject liquidity.

Companies defaulted on a total of $3.79 billion corporate bonds in both the onshore and offshore markets in January, 2.62 times the amount in the same period last year.

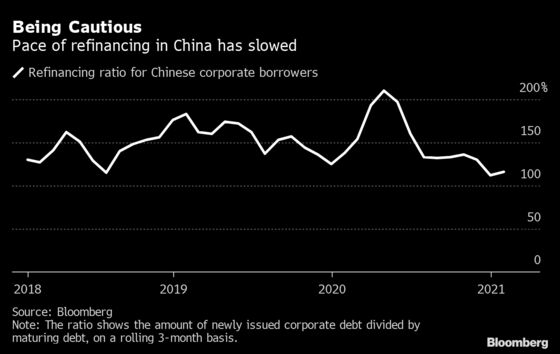

China has in recent months rolled out more measures to reduce financial risks and lower the speed at which debt is growing. That can be seen in the decline in the nationwide refinancing ratio, which peaked in April.

A ratio of more than 100% means more debt is issued than matured, and below 100% means that new debt isn’t keeping up with maturities. A score of 0% means there was no new debt issued.

©2021 Bloomberg L.P.