(Bloomberg Opinion) -- In a world caught between bulls and bears, convertible bonds can please both camps. As coupon-paying securities, they provide income like a bond. But they turn into equity if an issuer’s stock rises by a set amount, so investors can taste some of the upside, too.

In China, convertible bonds are by no means a compromise; they can offer mouth-watering capital gains that make you wonder if such a win-win situation can last. A year ago, Hong Kong-listed China Yuhua Education Corp. raised $120 million from a 363-day note. It’s now rewarding investors with a 67% return.

Acquisitive and cash-thirsty, Yuhua saw convertibles as a cheap way to raise debt — and the company worked hard to woo takers. In addition to a 3% coupon, it offered investors the opportunity to convert their shares at a strike price just 8% above where stocks were trading at issue, compared with a typical 20% to 30% premium. Management even offered to lower the conversion price if markets turned south by September. Win-win situations like these can’t last forever.

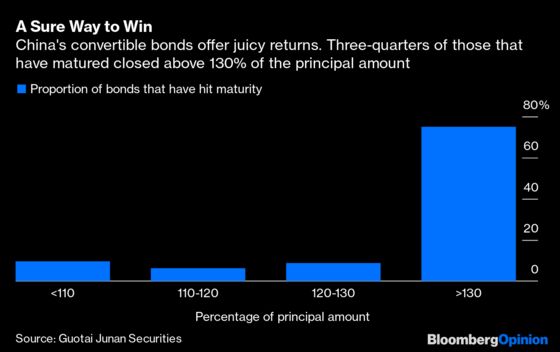

Increasingly in China, these bonds are designed to almost always turn into stock, either thanks to so-called conversion premiums that are artificially low, or generous clauses that can lower conversion prices. So what remains a relatively rare event in U.S. markets has become a more regular occurrence on the mainland, where close to 130 convertible bonds have hit their maturity, and more than 90% were converted into common stock, according to Guotai Junan Securities Co.

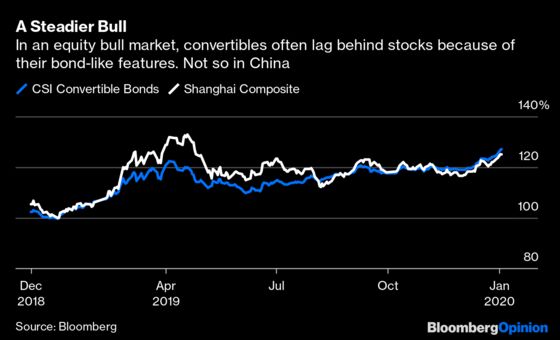

Borrowers eager to get cheap financing and investors hungry for yield have set off a market frenzy: China Inc. raised about $55 billion from such issues in 2019, equal to the previous two years combined. Last year, the CSI Convertible Bonds Index returned 26%, outpacing the blue-chip Shanghai Stock Exchange Composite Index. That compares with returns of 22% in the U.S., 8 percentage points shy of the 30% gain in the S&P 500 Index. Traditionally, convertible bonds lag behind stocks in a bull market.

Of course, China’s rising stock market has made conversion easy. But even in periods of decline, companies have shown that they’re more than happy to lower their conversion prices to help investors make a few extra bucks.

As for companies, convertibles are also a clever way to circumvent stricter listing regulations. While firms are required to wait at least 18 months between share offerings, such restrictions don’t apply to debt. Nor is shareholders’ approval required for issuance, so long as companies don’t go overboard. In the case of Yuhua, the limit is 20% of existing share capital.

So far, convertibles are a boon for borrowers and investors. But will this bull spirit last? At some point, stock investors will revolt, because convertibles designed to turn into equity by definition dilute their interests.

China’s capital markets are full of hybrids that blur the line between credit and equity. Inadvertently, Beijing’s securities regulators may be incubating a new bull market killer.

Of course, this came at great cost. For the fiscal year ended August 2019, the for-profit education provider reported 233 million yuan of non-operating paper loss, primarily due to fair value accounting on this bond.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2020 Bloomberg L.P.