China’s Companies Have Unseen Foreign Debt That’s Maturing Fast

Countries like China which control the flow of cross-border capital are recommended to hold reserves.

(Bloomberg) -- The foreign debt built up by Chinese companies is about a third bigger than official data show, adding to the pressure on the country’s currency reserves as a wave of repayment obligations approaches in 2020.

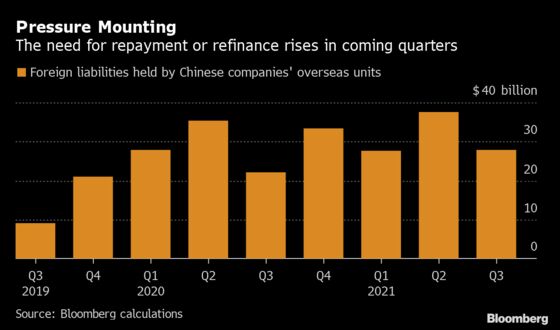

On top of the $2 trillion in liabilities to foreigners captured in official data, mainland Chinese firms have around another $650 billion in debts built up by subsidiaries overseas, according to Bloomberg calculations. About 70% of that debt is guaranteed by entities such as onshore parent companies and their subsidiaries, the data show. The amount of maturing debt will rise in coming quarters, with $63 billion due in the first half of 2020 alone.

The prospect of Chinese companies rushing to find dollars to service liabilities comes at a time when authorities have already allowed the currency to sink below 7 per dollar amid a trade war with the U.S. The nation now risks a reprisal of what happened after the yuan’s devaluation in 2015, when foreign-debt servicing contributed to a rapid decline in the country’s foreign-currency reserves.

“China’s debt servicing risks can be underestimated with this part of the debt staying outside the official gauge,” said Ji Tianhe, a strategist at BNP Paribas SA in Beijing, adding that the $3.1 trillion in foreign-currency reserves is “just enough” to cover the risks.

The PBOC set the yuan fixing rate at 7.057 per dollar Monday morning, stronger than forecast. The offshore Chinese yuan pared losses after falling to an all-time low against the dollar.

Countries like China which control the flow of cross-border capital are recommended to hold reserves worth 30% of short-term foreign debt, 20% of other external liabilities, 10% of exports and 10% of broad money supply to counter potential outflow risks, according to a guideline by the International Monetary Fund.

Global Standards

Applying that methodology to the official data on China’s foreign liabilities suggests the nation would need at least $2 trillion of reserves during a currency crisis, and more than that if capital controls aren’t enforced well, according to Natwest Markets Plc. If the debt of Chinese companies’ overseas units is taken into account, the reserves would need to be higher still.

China doesn’t include the debt of offshore entities when calculating foreign liabilities and this is in line with global standards, according to the State Administration of Foreign Exchange, the part of the People’s Bank of China which manages the reserves. SAFE also stressed that the fundraising of those offshore entities is under their regulatory oversight, according to a written response to questions from Bloomberg.

“China’s foreign debt risks are under control generally” and there’s still room to raise more foreign debt, Ye Haisheng, SAFE director in charge of capital account management, wrote in an article in April. “However, a country relying too heavily on foreign debt is subject to debt-related risks and even currency and financial crises” when the external environment worsens, he said, referring to episodes like Europe’s sovereign debt turmoil in the last decade.

Yuan Pressure

The pressure on Chinese companies to repay or refinance debt securities will rise into 2020, the data compiled by Bloomberg show, and the recent weakening of the yuan to a decade-low amid persistent trade frictions could complicate that process. Looming repayments and stricter rules for refinancing could lead to defaults, reduction in capital inflows, and even outflows, squeezing domestic credit supply, according to research from Nomura Holdings Inc.

“Statistically, these borrowings by overseas entities are not China’s direct foreign debt,” said Guan Tao, a former official with the State Administration of Foreign Exchange. “But if it is guaranteed by domestic companies, which bears a secondary repayment duty, it becomes contingent debt.”

If companies struggle to pay the coupon or repay their debt, then the effects may become more widespread. In June, China Construction Bank Corp. had to repay a defaulted $300 million note from an overseas unit of China Minsheng Investment Corp. as it had provided a standby letter of credit.

Property Debt

Onshore parent companies may also have to increase collateral if the yuan swings wildly and this would increase the financing costs of the borrowers, said Guan, now a professor of economics at Wuhan University. He added the risks shouldn’t be overstated as it needs to be analyzed case by case.

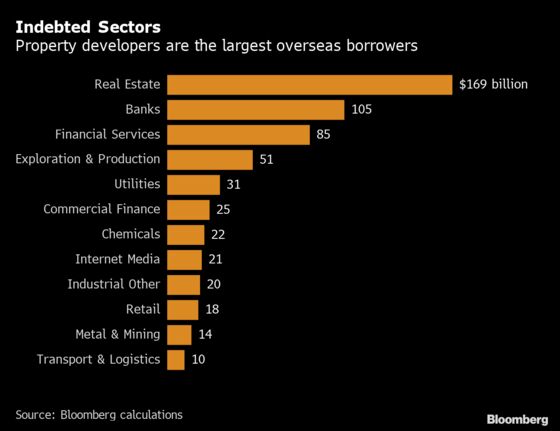

Property developers are the largest borrowers overseas and have accumulated nearly $169 billion as of Aug 23, Bloomberg data showed. JPMorgan Chase & Co. estimate that property developers will need to refinance about $39 billion worth of offshore bonds before June 2020.

The cash flows and the earnings of many property developers are still solid, and they remain in a relatively good shape for now, Hong Hao, chief strategist at Bocom International in Hong Kong, said in an interview with Bloomberg TV Monday.

The authorities have taken steps to prevent risks. The National Development and Reform Commission announced rules in June limiting the number of local state-owned enterprises which can sell bonds offshore, and last month, the rules for property developers selling foreign debt were also tightened.

“Over the next few years, China is set to incur consistent current account deficits as trade tensions reduce net exports and services outflows keep increasing,” Mansoor Mohi-uddin, macro strategist at Natwest Markets, wrote in a note. “The PBOC is thus likely to want to maintain its foreign-currency reserves in case it faces balance of payments pressures in future.”

--With assistance from Huixuan Qu and Zheng Wu.

To contact Bloomberg News staff for this story: Yinan Zhao in Beijing at yzhao300@bloomberg.net;Qizi Sun in Beijing at qsun62@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, James Mayger

©2019 Bloomberg L.P.

With assistance from Bloomberg