China's Capital Controls Keep a Bad Year From Getting Worse

Signs of an exodus from the world’s biggest emerging market are hard to find. What gives?

(Bloomberg) -- In many ways, it looks like the perfect environment for Chinese capital outflows: economic growth is slowing, U.S. interest rates are rising, and the yuan is trading near its weakest level in more than a decade.

Yet signs of an exodus from the world’s biggest emerging market are hard to find. What gives?

Analysts point to China’s stepped up capital controls. Tightened in the wake of a shock yuan devaluation three years ago, restrictions on everything from overseas takeovers to purchases of insurance policies in Hong Kong have kept outflows closer to a trickle than a flood in 2018.

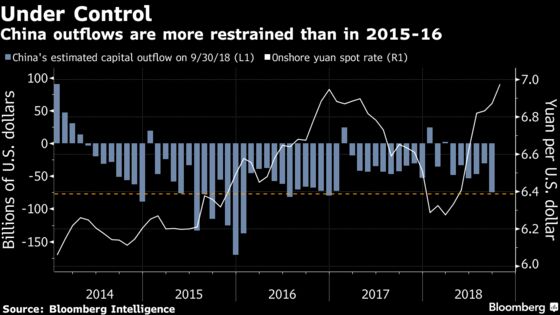

That should provide some comfort to investors after a turbulent year for Chinese financial markets that included rising bond defaults, real estate jitters and a $2.7 trillion selloff in equities. Even as the yuan and Shanghai stocks sank to multi-year lows in October, Chinese demand for foreign currencies moderated, according to official data published last week.

“Capital controls have played a very big role in limiting outflows during this round of yuan depreciation,” said Tommy Xie, an economist at Oversea-Chinese Banking Corp. in Singapore. “It’s very unlikely we will see disorderly outflows again.”

Chinese measures to curb capital flight in recent years include a ban on domestic cryptocurrency exchanges, increased disclosure requirements for individuals buying foreign currencies, and tightened restrictions on corporate investments overseas. They were all designed to help policy makers avoid a downward spiral of yuan depreciation, outflows and more depreciation.

That dynamic roiled the country’s financial system in late 2015 and 2016, when investors pulled an estimated $1.4 trillion from the country. Net outflows this year through September have been smaller, totaling about $296 billion, according to Bloomberg Intelligence.

“Compared with 2015 and 2016, outflow pressure has been moderate,” said Ding Shuang, Greater China and North Asia chief economist at Standard Chartered Plc.

Of course, that could change if the yuan’s slide accelerates. One sign that Chinese citizens haven’t lost interest in pulling money out: visits to Ybex, a Hong Kong-based online platform that helps connect individuals with foreign-exchange dealers, more than doubled from March to October as the Chinese currency weakened. “We’ve been receiving more and more inquiries about how to change money out of the yuan over the past few months,” said Andrew Lee, Ybex’s co-founder and chief executive officer.

A key test for the currency will come in January, when China resets its $50,000-a-year foreign exchange quota for citizens.

If outflow pressures increase, authorities still have plenty of tools at their disposal. They could increase administrative hurdles for individuals and companies trying to pull money out, or step up intervention in the foreign-exchange market to combat expectations of yuan weakness.

This month, the central bank signaled more hands-on management of the currency and sold its first-ever bills in Hong Kong, a move that may have been designed in part to discourage yuan short sellers. After seven straight months of depreciation, the Chinese currency has recorded a slight gain in November, and is now trading around 6.9367 per dollar.

“China may take a slew of market-oriented or non-market-oriented measures to stabilize the exchange rate,” Ming Ming, head of fixed-income research at Citic Securities Co. in Beijing, wrote in a recent note. As a result, “the chance for the yuan to fall to 7 a dollar is dropping.”

--With assistance from Alfred Liu.

To contact the reporters on this story: Tian Chen in Hong Kong at tchen259@bloomberg.net;Yinan Zhao in Beijing at yzhao300@bloomberg.net

To contact the editors responsible for this story: Richard Frost at rfrost4@bloomberg.net, ;Jeffrey Black at jblack25@bloomberg.net, Michael Patterson, Sam Mamudi

©2018 Bloomberg L.P.