China’s Bond Traders Stuck With a Market That Just Doesn’t Move

China's Bond Traders Stuck With a Market That Just Doesn't Move

(Bloomberg) --

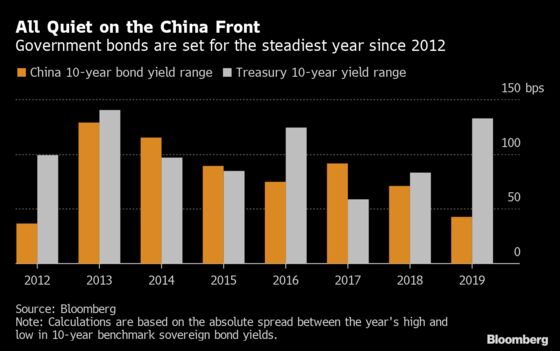

While most of the world’s bond markets swing between massive gains and losses, traders in China are getting increasingly stuck.

Consider this: last week’s paltry 8 basis-point increase in the nation’s 10-year yield was the worst rout in five months, even as a return of risk appetite sank sovereign debt globally. It shows how little the bonds are moving, with the rate trading between 3% and 3.12% since August. This year’s range -- at just 42 basis points -- is set to be the narrowest in seven years.

Improving sentiment in equities is now offsetting a dovish (yet not so dovish) central bank, meaning there’s little conviction either way among bond traders onshore. While the People’s Bank of China has tweaked multiple policies to support a slowing economy in recent months, it’s refrained from deploying the sweeping stimulus that some bond bulls had been hoping for.

“The domestic bond market is stuck,” said Ming Ming, head of fixed income research at Citic Securities Co. “Monetary policy has remained steady, and policy makers have a higher tolerance for downward pressure on the economy.”

Weaker-than-expected economic data on Monday will have bond traders looking for signs of easing from policy makers as soon as this week. Industrial output, retail sales and fixed-asset investment all rose less than anticipated in August.

Frances Cheung, head of Asia macro strategy at Westpac Banking Corp., said the PBOC may cut the rate on medium-term lending facilities Tuesday as 265 billion yuan ($37.5 billion) of loans mature. Even if the rate is left unchanged, the central bank could lower the cost of borrowing with the loan prime rate on Sept. 20, she said.

China’s bonds have had a relatively good few months amid a sell-off in the equity market, with the 10-year yield in August falling briefly below 3% for the first time since 2016. Their addition to the Bloomberg Barclays Global Aggregate Index has helped attract foreign investors, who have bought about $40 billion of the bonds this year through August. JPMorgan Chase & Co. will start a phased inclusion into its benchmarks from February.

Still, the rally has been capped by concerns over credit risks, a volatile yuan and increasing supply. More than 2 trillion yuan of special government bonds will be sold this year by the end of September, and China is considering allowing regional authorities to sell more debt for infrastructure investment, people familiar with the matter have said.

Beijing’s calibrated approach to stimulus has also kept bond bulls in check. China’s central bank this month cut the amount of money lenders need to deposit in reserves to the lowest level since 2007 - a move that will inject 900 billion yuan into the economy. It’s also been adding liquidity via open-market operations.

Still, the PBOC hasn’t touched its one-year benchmark lending rate since 2015 even as weak economic data strengthened the case for further stimulus. It also passed on the opportunity to lower the rate for medium-term loans earlier this month. Its big overhaul of how loan rates are calculated only reduced costs by a small amount, and largely fell flat with the bond market.

It all means Chinese bonds are unlikely to get much of a lift from monetary policy, according to Hao Zhou, a senior emerging markets economist at Commerzbank AG. He predicts the 10-year benchmark yield will end the year at 3.1%. The bonds traded at a yield of 3.09% as of 5:22 p.m. in Shanghai.

“Bond yields will likely remain sticky for now,” he said.

--With assistance from Helen Sun, Jeffrey Black and Philip Glamann.

To contact Bloomberg News staff for this story: Livia Yap in Shanghai at lyap14@bloomberg.net;Yuling Yang in Beijing at yyang329@bloomberg.net;Yinan Zhao in Beijing at yzhao300@bloomberg.net;Claire Che in Beijing at yche16@bloomberg.net

To contact the editors responsible for this story: Sofia Horta e Costa at shortaecosta@bloomberg.net, Tian Chen

©2019 Bloomberg L.P.

With assistance from Bloomberg