China's Default Scares Are Giving Bond Investors Whiplash

China's Big Default Scares Are Giving Bond Investors Whiplash

(Bloomberg) -- China’s biggest default scares of 2019 have taken bondholders on some wild rides, underscoring both the risks and the opportunities for investors as more of the nation’s companies struggle to repay debt.

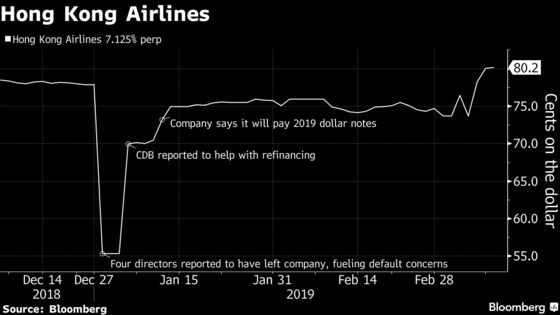

At least three large Chinese borrowers -- Qinghai Provincial Investment Group Co., China Minsheng Investment Group Corp. and Beijing Orient Landscape & Environment Co. -- missed bond-payment deadlines last month only to come up with the cash shortly thereafter. A fourth issuer, Hong Kong Airlines Ltd., saw its dollar bonds plunge on repayment concerns in January but made good on a maturing note after reportedly securing help from China Development Bank.

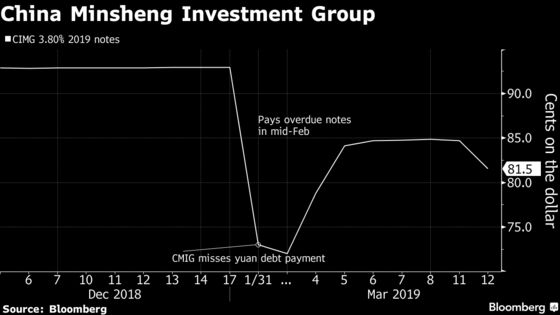

In all four cases, knee-jerk declines in the companies’ bonds gave way to at least partial recoveries. Dollar notes issued by Hong Kong Airlines have rallied 45.5 percent from their lows and CMIG’s have gained 12.4 percent.

While many bond investors would rather avoid such volatility, some buyers of distressed debt welcome it. Taking advantage of the turbulence requires acting fast in illiquid markets, making the right call on borrowers’ ability to repay, and -- in some cases -- determining the Chinese government’s willingness to intervene. That’s no easy task amid an uncertain economic outlook and mixed messages from Chinese authorities on corporate bailouts.

“Price volatility in distressed names does bring investment opportunities,” said Gary Zhou, Hong Kong-based fixed-income director at China Securities International. “But they are more likely to be grasped by specialized distressed fund managers who follow those names very closely, have greater access to information about the issuers and are able to carry out in-depth analysis of default probabilities.”

It could be a risky trade given that defaults are piling quickly this year. Goldman Sachs Group Inc. in a note last week that timeliness of repayment can’t be ensured even in cases where support is provided.

The following charts show how bonds at the center of this year’s default scares have performed since repayment concerns bubbled to the surface.

The affiliate of embattled conglomerate HNA Group Co. was rocked by default concerns in early January after reports that key directors and executives had left the company. But Hong Kong Airlines denied speculation it had applied for liquidation and repaid $550 million of bonds on time. It may have got REDD Intelligence reported that CDB agreed to help refinance the notes.

The conglomerate, once hailed as a poster child of China’s vibrant private sector, shocked investors when it missed a bond payment on Jan. 29. CMIG repaid the notes on Feb. 14 after agreeing to sell one of its biggest assets.

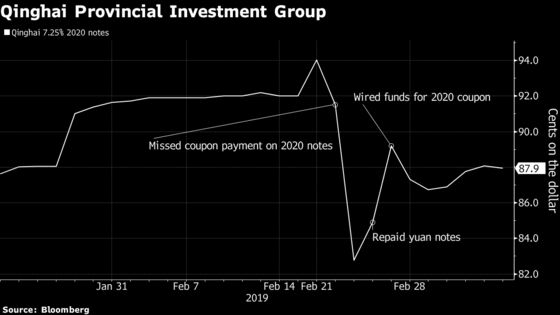

The aluminum producer, seen as a bellwether for China’s willingness to support troubled companies linked to local governments, surprised investors when it failed to repay a dollar-bond coupon on Feb. 22, citing insufficient cash offshore. The company wired the funds five days later and repaid 20 million of yuan notes on Feb. 25. That spurred a partial recovery in Qinghai’s bonds, but investors remain wary.

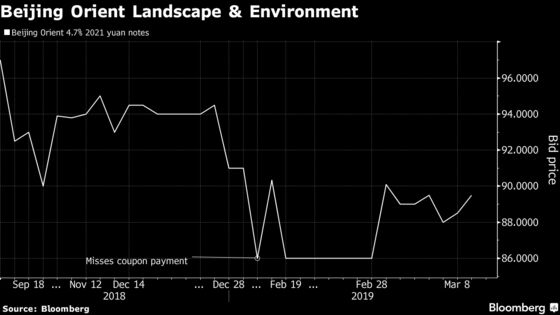

The builder of water-treatment plants said it transferred 500 million yuan for the principal payment on a yuan bond due last month, but failed to send a 30 million yuan interest payment on time because of a staff error. One day after it was due, Shanghai Clearing House confirmed receiving the full payment.

To contact Bloomberg News staff for this story: Ina Zhou in Hong Kong at hzhou179@bloomberg.net;Yuling Yang in Beijing at yyang329@bloomberg.net;Qingqi She in Shanghai at qshe@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Michael Patterson, Lianting Tu

©2019 Bloomberg L.P.

With assistance from Bloomberg