China’s Hurting Banks Brace for Worst-Case Economic Scenario

Banks are already suffering record loan defaults as the economy last year expanded at the slowest pace in three decades.

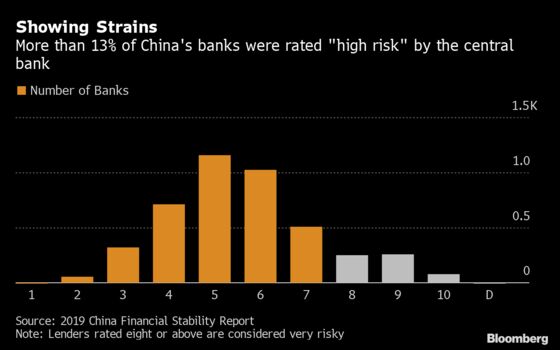

(Bloomberg) -- Just as it looked like Beijing was starting to get a handle on its regional banking crisis, a much more severe threat is engulfing the world’s largest banking system as a deadly new virus hits the country’s economy.

The impact of the spreading coronavirus risks bringing to life the worst-case economic scenarios contained in China’s annual banking stress tests. Last year’s exercise envisaged annual economic growth slowing to as low as 4.15% -- a scenario which showed that the bad loan ratio at the nation’s 30 biggest banks would rise five-fold. Analysts now say that the outbreak could send first-quarter growth to as little as 3.8%.

Banks are already suffering record loan defaults as the economy last year expanded at the slowest pace in three decades. The slump tore through the nation’s $41 trillion banking system, forcing the first bank seizure in two decades and bailouts of two other key lenders.

“The banking industry is taking a big hit,” said You Chun, a Shanghai-based analyst at National Institution for Finance & Development. “The outbreak has already damaged China’s most vibrant small businesses and if it prolongs, many firms will go under and be unable to repay their loans.”

The virus outbreak comes on top of an unresolved trade dispute with the U.S. With many banks under-capitalized, it may put even the nation’s heavyweight lenders, often called on to support growth, at danger from the growing stress.

Economic growth is seen plummeting this quarter, even amid heavy cash injections from the central bank. Whether that stagnation will carry through to the rest of the year, depends on how quickly authorities can get a handle on the spreading virus and get its economic engines running again.

UBS Group AG estimates growth will slow to 3.8% in the first quarter from a 6% pace at the end of year and to 5.4% for 2020 if the virus is contained within three months. If the virus is more protracted, annual growth could dip below 5%, UBS said. Goldman Sachs Group Inc. also predicts a sharp slowdown in the quarter to 4%, while still predicting full-year growth at 5.5%.

Doing its own calculations based on China’s stress tests, debt rating firm S&P Global estimates that the worst-case scenario would cause bad debt to balloon by 5.6 trillion yuan ($800 billion), for a ratio of about 6.3%, adding to the already daunting 2.4 trillion yuan of non-performing loans China’s banks are sitting on.

Banks with operations concentrated in Hubei province and its capital city of Wuhan, the epicenter and the region worst hit by the virus, will likely see the greatest increase in problem loans.

The region had 4.6 trillion yuan of outstanding loans doled out by 160 local and foreign banks at the end of 2018, with more than half in Wuhan. The five big state banks had 2.6 trillion yuan of exposure in the region, followed by 78 local rural lenders, according to official data.

Moreover, policy makers have once again enlisted its largest lenders, including Industrial and Commercial Bank of China Ltd., to serve their civic duty by bailing out millions of struggling small businesses by providing more cheap loans, rolling over debt and waiving fees.

Officials on Friday sought to ease concern over the hit to the banking sector. Zhou Liang, vice chairman of the China Banking and Insurance Regulatory Commission, said that a potential increase in bad loans is manageable. Chinese lenders dissolved 3 trillion yuan of bad loans last year alone, he said, adding that bad loan ratio of China’s small businesses was at 3.22%.

Highlighting the plight of small bushiness, a recent nationwide survey show about 30% said they expect to see revenue plunge more than 50% this year because of the virus and 85% said they are unable to maintain operations for more than three months with cash currently available.

“Social stability is of utmost importance to the authorities in China,” S&P analysts led by Tan Ming said in a recent report. “Therefore, banks have been asked to help carry the burden of this health outbreak.”

While most state banks agreed to cut the borrowing costs of virus-stricken firms by 0.5 percentage point, the State Council now requires them to ensure that small businesses are paying no more than 1.6% with government subsidy. Even as cheaper financing may help the broader economy, rates below 5% mean banks are barely making enough money to cover their cost of funding after accounting for default risks, people familiar with the matter have said.

A major difference from the 2008 global financial crisis, or the 2003 outbreak of SARS “is the lack of bank capital now to support an aggressive bank-led credit stimulus,” said Grace Wu, head of Greater China Banks at Fitch Ratings in Hong Kong. “Chinese banks do not have the same capacity to replenish capital now given their profitability has trended down in recent years.”

And investors are turning more downbeat on the Chinese banks whose shares have underperformed the benchmark in most of the past five years. The “big four” state-owned lenders, which together control more than $14 trillion of assets, currently trade at an average 0.6 times their forecast book value, near a record low.

ICBC fell 1.8% in Hong Kong as of 9:50 a.m., extending this year’s decline to 11%, while China Construction Bank Corp., the nation’s second largest, has lost 7.6% so far in 2020.

The unexpected epidemic is now their greatest test.

“The resilience of China’s banking system may be severely tested,” the S&P analysts said.

--With assistance from Helen Sun and Zheng Li.

To contact Bloomberg News staff for this story: Jun Luo in Shanghai at jluo6@bloomberg.net;Lucille Liu in Beijing at xliu621@bloomberg.net

To contact the editors responsible for this story: Candice Zachariahs at czachariahs2@bloomberg.net, Jonas Bergman

©2020 Bloomberg L.P.

With assistance from Bloomberg