China's Aversion to Big Bang Stimulus Tested by Trump Tariffs

Tax cuts seen as likely route to mitigating economic fallout.

(Bloomberg) -- China’s attempt to break free from the debt-financed stimulus of the past is being stress tested by Donald Trump.

As the White House threatens tariffs on everything the U.S. imports from China, policy makers in Beijing are cushioning the economic blow with tax cuts, regulatory relief and investment incentives, rather than the kind of spending and monetary binge seen in 2008 and 2015.

While big bang support can’t be discounted should growth and employment really take a hit, economists for now expect China’s composure to hold, meaning more targeted tax cuts rather than breakneck spending.

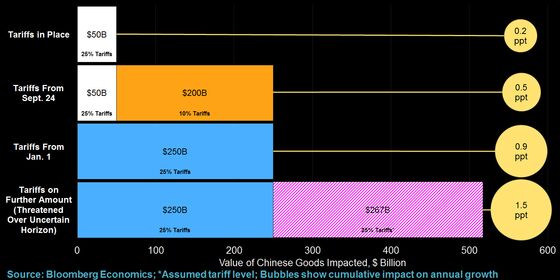

Impact of Tariffs on China’s Growth

“In the past they have been throwing big money via the state owned enterprises at big infrastructure projects and now it is more about giving money to the people and hoping they will spend it,” said Joachim Fels, global economic adviser at Pacific Investment Management Co. “We think there will be more fiscal easing over and above what has already been announced.”

Comparison of China’s stimulus this year to 2008 and 2015

China’s leaders from Xi Jinping down are politically committed to avoiding a ‘flood’ of stimulus, and a multi-year campaign to curb the rate of debt expansion appears paused, not scrapped. Xi’s right-hand man on the economy, Liu He, has long advocated a shift away from credit-fueled growth at all costs and senior officials continue to warn of the dangers of excess debt, even as they seek to channel more money to cash-strapped private businesses.

Underscoring the need for support, economists downgraded their forecasts for gross domestic product growth in the final three months of 2018 and the first quarter of 2019, according to a Bloomberg survey of 65 analysts published Tuesday. An official gauge of activity in China’s manufacturing sector worsened in October, data released Wednesday showed, falling to 50.2 from 50.8 in September, missing the median prediction of 50.6 in a Bloomberg survey of forecasters.

What Our Economists Say... |

|---|

Bloomberg Economics estimates that the drag on 2019 GDP growth could be about 1.5 percentage points -- assuming a tariff rate of 25 percent on all Chinese imports. Absent a policy response from Beijing, that would take China’s GDP growth toward 5 percent, down from a forecast 6.6 percent in 2018. There are, of course, multiple uncertainties that make a drop of that magnitude unlikely. -- Tom Orlik and Chang Shu, Bloomberg Economics Click for the full note. |

The key question for the economy in the coming months is whether the boost from policies announced this year will kick in with enough force to outweigh the drag from higher duties and the fading effect of a pre-tariff export-rush.

The success or failure of China’s attempts to stabilize its economy matters much more for the rest of the world than it used to, as the nation is “a more balanced contributor to global growth” according to Bank of America Merrill Lynch economists Ethan Harris and Aditya Bhave.

The IMF now calculates that China contributes about a third of the global expansion.

China’s targeted stimulus approach is primarily geared to stoking domestic demand, for instance a tax cut on the purchase of cars, as Bloomberg News reported Monday. While that move may dovetail with others aimed at reducing the cost of consumption, like tariff reductions, Chinese households in the biggest cities still face soaring rents and rising outlays for food, education and healthcare.

But even with the domestic economy pressured, there are two major constraints to enacting more powerful stimulus -- debt and the weakening yuan.

Read More on China’s Trade War Response |

|---|

|

Non-financial corporate debt is rising again as a percentage of gross domestic product following a year and a half of deleveraging from its mid-2016 record, according to data from the Bank for International Settlements.

Efforts to support infrastructure debt will add to local governments’ debt burdens. And with household leverage rising quickly, consumers are less able to borrow the nation out of trouble than before. That atmosphere contributes to a heightened risk awareness among small and medium-sized companies, who are struggling to get funding even if they want it.

Meantime, the yuan dropped to its weakest level since May 2008 on Tuesday, close to the key level of 7 per dollar. The weak yuan would make any large-scale expansion of the money supply perilous for domestic purchasing power. Policymakers will be reticent to let it weaken significantly for fear of broadening the trade war into a new front: currencies.

Given such constraints, and the background goal of curbing credit expansion, the central bank has so far refrained from broad monetary easing. Instead, it has sought to reorganize the liquidity available so that it flows to the right places. Growth in outstanding credit, and the money supply, are still slowing.

That leaves fiscal policy one of the few available circuit breakers, and an expansion of the deficit in 2019 a likely option. China International Capital Corporation Ltd sees potential for cuts to the value-added tax rate in 2019 and even a cut to the corporate income tax rate -- where China still charges firms more than comparable peers. Economists Eva Yi and Hong Liang see the deficit expanding to the 3 percent of GDP from this year’s 2.6 percent target.

And unlike the deeply indebted corporate sector, China’s central government still has deep pockets to draw from.

"We expect the Chinese government to continue to roll out stimulus measures that match the weakness in the economy," the Bank of America economists wrote in a recent note. "This should help ensure a soft landing next year. However, the trade war still has a ways to go and it is much too early to judge the efficacy of the stimulus measures. Stay tuned."

--With assistance from Matthew Boesler.

To contact the reporters on this story: Jeffrey Black in Hong Kong at jblack25@bloomberg.net;Yinan Zhao in Beijing at yzhao300@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, Malcolm Scott, James Mayger

©2018 Bloomberg L.P.