China’s $6 Trillion Hidden Debt Gets Stress-Tested in Downturn

China’s $6 Trillion Hidden Debt Gets Stress-Tested in Downturn

(Bloomberg) -- China’s property market crunch is making it difficult for local governments to cut an estimated $6 trillion of hidden debt even as Beijing shows more determination in cracking down on the problem.

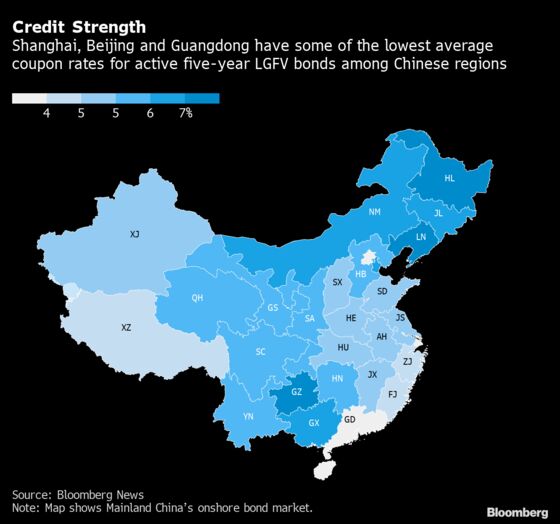

Beijing, Shanghai and Guangdong province are planning trials to eliminate the off-balance sheet borrowing that local authorities use to raise funds for spending. Although there were no details, it’s likely the pilot programs could eventually be rolled out to more of the 31 other regions in the country.

The central government is getting more serious about tackling financial risks associated with the debt, which it labeled a “national security” issue earlier this year. Authorities must balance the push to fix the problem with efforts to keep record bond defaults and a slowing economy from getting out of hand.

Read More: China Is Slowing - That’s a Problem: BE Nowcasts

A downturn in the property market won’t make it an easy task. Land sales, which account for about 40% of local governments’ revenue, have tumbled since August, putting pressure on public finances. Moody’s Investors Service warns of a potential decline in land sales income and local governments possibly taking on more, not less, debt in order to fund infrastructure.

Here’s a look at what government-linked economists say are the challenges faced in trying to eliminate the debt.

What is hidden debt?

Local governments, under pressure to shore up growth in the wake of the global financial crisis in 2008, went on a borrowing binge to fund infrastructure projects as part of China’s 4 trillion yuan ($626 billion) stimulus package.

Before a new budget law was introduced in 2015, regional authorities weren’t allowed to borrow directly. Instead, they were encouraged by Beijing to use state-owned companies now known as local government financing vehicles, or LGFVs, to raise money through bank loans, and later, bond issuance.

The debt doesn’t appear on the balance sheets of local governments, yet carries an implicit guarantee of repayment with public money. Most of the debt is owned by local banks, so the surge over the years has led to moral hazard and risks to the financial system.

In a way, the hidden debt is emblematic of China’s old growth model, one that’s heavily dependent on investment and debt-fueled urbanization.

How big is the problem?

Much of the problem lies precisely in the fact that there’s no way to ascertain exactly how much debt local governments have accumulated.

The International Monetary Fund estimates LGFV debt amounted to 39 trillion yuan ($6 trillion) in 2020. Goldman Sachs Group Inc puts it at 53 trillion yuan. Using a narrower definition, the state-run National Institution for Finance & Development estimates 15 trillion yuan.

The problem is becoming thornier with the property slump. On the one hand, LGFV bonds have become popular among investors seeking shelter in state-backed assets, following a sell-off in private developers’ bonds. On the other hand, many LGFVs count land as their main assets and declining land sales could hurt their ability to repay debt.

It’s also likely Beijing could lean on state firms to help ease property market stress, which may make it even harder to cut down on hidden debt. Local state-owned companies and LGFVs could be called in to help, through for example, buying more land or bailing out firms if needed.

Many regions -- especially those in the western hinterland -- have been slow in addressing the problem, and could delay efforts if the central government doesn’t roll out the trial programs, said Mao Jie, a professor at the University of International Business and Economics, who advises the Ministry of Finance.

“It’s a systemic challenge” to resolve hidden debt, he said. “Both local governments and the market need to make enormous changes in the way they operate.”

How can provinces tackle it?

Several options are available, according to the experts.

Repaying debt with fiscal revenue

- Some cities in Guangdong province have repaid LGFV debt with public income, and this remains one of the manufacturing hub’s options during its trial, according to Wen Laicheng, a professor at Central University of Finance and Economics. Guangdong could probably eliminate its hidden debt within two years, Mao said.

Repaying debt by selling LGFV or government assets or equities

- This could help local governments make more efficient use of assets, even though they will have less resources, said Cui Zhijuan, a professor at Beijing National Accounting Institute, which is under the Ministry of Finance.

Repaying debt with project returns and LGFVs’ profit

- This could only be viable in a few places such as Shanghai, because most LGFVs’ projects are public welfare and have limited returns, Wen said.

Transforming LGFVs into real market entities

- This would turn hidden debt into corporate debt, as LGFVs take on more profit-driven business, such as utility and construction instead of public welfare projects.

Replacing hidden debt with refinancing bonds

- A total of 688 billion yuan worth of such bonds have been sold as of the end of October with the purpose of repaying existing debt, according to GF Securities Co. Ltd. The issuance though would be restricted by the governments’ debt cap and may take place in Beijing, Shanghai and Jiangsu province mainly, according to China Industrial Securities Co. Ltd.

Restructuring or bankruptcy of LGFVs

- While none of the LGFVs have defaulted so far, provinces including Jiangsu and Yunnan have said they will restructure or liquidate LGFVs that have lost repayment capabilities. Bankruptcies may be a necessary cost to pay in order to reform some LGFVs, while at the same time China needs to guard against any “malicious evasion” of debt repayment by local authorities, Cui said.

What’s been happening so far?

China has tried to bring hidden debt under control over the past decade. Here are a few examples of success in different regions:

- Shanxi province merged about three dozen highway builders into one entity, which signed new loan arrangements with banks and reduced interest payments

- Shanghai SMI Holding Co. Ltd. is one of the earliest examples of successful LGFV reform, according to Mao

- Liaozhong district in the northeastern city of Shenyang repaid 15 million yuan of debt with assets in 2019

- Duolun county in Inner Mongolia repaid 600 million yuan of hidden debt with properties they owned

- Authorities set up a municipal bond market in 2015 to move financing away from the more opaque LGFV debt

Going forward, the trials are likely to expand next year to more cities in less developed regions, such as the western provinces, according to Zhang Yiqun, a member of the Society of Public Finance of China. Despite the challenges, the country will likely cut all hidden debt by 2035, and regions with better finances may be able to achieve that by 2025, he said.

“About half of the debt will be repaid, and the other will be transformed into on-balance-sheet debt,” Zhang said.

©2021 Bloomberg L.P.

With assistance from Bloomberg