China Risk May Overshadow Emerging Markets Eyeing Vaccine Hopes

This factor may overshadow optimism on vaccine developments during the final week of August.

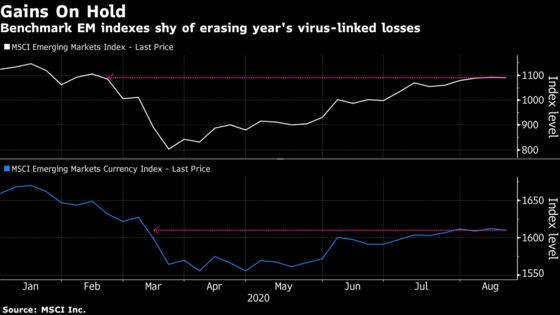

(Bloomberg) -- The final week of August may prove key for emerging markets attempting to erase this year’s losses as investors fret that rising U.S.-China tension will overshadow optimism about vaccine developments.

Stocks, currencies and dollar bonds from the developing world fell last week after President Donald Trump called off a meeting on the trade pact. MSCI Inc.’s emerging-market equity gauge halted a four-week winning streak, while Brazil’s real and Russia’s ruble both dropped more than 2%. Dollar bonds slid for a second week, the first back-to-back decline since the pandemic was declared in March, a Bloomberg Barclays index shows.

Investors are seeking confirmation of revised timing for the U.S.-China talks as the yuan hovers around the key 6.90 per dollar level. The Trump administration ratcheted up pressure on China last week, suspending its extradition treaty with Hong Kong and ending reciprocal tax treatment on shipping with the former British colony. The move came after China imposed a national security law that led to charges against more than 20 pro-democracy activists.

Developing stocks and currencies got a boost on Monday, with the Trump administration said to be signaling that U.S. companies can continue to use the WeChat messaging app in China.

“The main thing markets will continue to focus on is U.S.-China,” said John Malloy, co-head of emerging and frontier markets at RWC Partners in Miami, which oversees $8 billion in emerging and frontier assets. As we get closer to the American presidential election, “we’re going to see more rhetoric coming out of the U.S. government and probably responses from Chinese authorities as well,” he said.

Currencies from the developing world may not attract inflows without promising vaccine news, according to Citigroup Global Markets Inc. strategists including Dirk Willer in New York. Credit markets will also pay close attention to scientific developments to track when economies can reopen without the risk of a resurgence.

“Markets should continue to trade vaccine headlines, and although a ‘silver bullet’ vaccine is unlikely in the near term, expedited review processes in some countries (e.g. China and Russia) could present upside surprises as the year concludes,” Citigroup strategists wrote in a separate note.

Political risk still clouds sentiment in the Eastern Europe, Middle East and Africa region. In Eastern Europe, investors will be again watching Belarus, where President Alexander Lukashenko faces protests after a disputed election. While Vladimir Putin publicly supports Lukashenko, Russia’s president has problems of his own after being accused of orchestrating the near-fatal poisoning of an opposition leader.

In Africa, regional leaders are pressing their demand for the reinstatement of Mali President Boubacar Keita, who was deposed in a military coup last week. France and the United Nations, wary of the impact the coup may have on a Western-backed counter-insurgency effort in the country, appealed for calm and urged soldiers who detained Keita to free him.

Listen: EM Weekly Podcast: Shift in Monetary Policies; Inflation Threat

Korea, Hungary Decide

Bank of Korea is likely to keep policy on hold Thursday, with rates close to the effective lower bound, according to Bloomberg Economics and the unanimous consensus of economists. The growth forecast is likely to be cut considerably, according to the central bank Governor Lee Ju-yeol told parliament

Korea’s 10-year bond yield has crept up since Monday last week, although it may change direction if the country decides to adopt tighter social-distancing measures

- Read: Korea Virus Wave Disrupts Recovery as Stronger Measures Eyed

- Hungary’s central bank will probably leave its benchmark rate at 0.6% on Tuesday, according to a separate Bloomberg survey. Policy makers lowered the rate by 15 basis points last month

Brazil Watch

- In Brazil, investor sentiment will probably be driven by debates on the post-Covid fiscal adjustment. Last week, Brazil’s lower house maintained a freeze on public sector wages that had been unexpectedly voted down by the senate, an episode that revealed cracks in President Jair Bolsonaro’s congressional base

- A consumer price inflation reading up to mid-August will probably flag an uptick stoked by rising food prices. Current-account data for July, to be released on Tuesday, is forecast to show a surplus of almost $8 billion, according to economists surveyed by Bloomberg

- Brazilian unemployment figures due Friday may show an increase in the jobless rate in July

Debt Deals

- Argentine foreign-law bondholders who accept the nation’s debt offer and tender an exchange before Friday will be eligible for additional consideration on accrued interest and will have greater ability to select the new bonds received

- Argentina’s Exchange Bondholder group will exchange a total $4.8 billion of bonds on or before Aug. 24

- The nation needs to come to an agreement to renegotiate its debt with the International Monetary Fund and push forward with an economic plan

- Ecuador, meantime, extended its deadline to settle its debt restructuring offer with bondholders until Sept. 1 from Aug. 20

Other Data and Events

- Taiwan’s industrial output rose 2.65% in July from a year earlier, lower than economists’ expectations

- Poland’s M3 money supply fell 0.3% in July from a month earlier, according to data released on Monday. On Tuesday, the statistics office presents unemployment data, while the central bank holds a non-policy sitting, followed on Thursday with July minutes

- South Korea will report consumer confidence for August on Tuesday. Investors will look to see if the recent spike in local Covid cases has dented sentiment. September manufacturing business survey follows on Wednesday

- Thailand manufacturing numbers are due from Wednesday

Mexico’s inflation accelerated further beyond the central bank’s target in early August due to a spike in fruit and vegetable prices, boosting expectations that the bank will soon halt a cycle of interest rate cuts

- A final reading of Mexican second-quarter GDP growth is expected to show an 18.9% contraction, according to economists surveyed by Bloomberg

- Though consumer inflation in South Africa is seen accelerating in July, the rate remained below the central bank’s 3%-6% target range, data may show Wednesday, according to the median estimate in a Bloomberg survey

- China will publish July industrial profits on Thursday. The figures have bounced back despite the Covid-19 shock

- Malaysia will report July trade data on Friday

- The ringgit was the second-strongest performer in EM Asia last week, after the yuan

- Chile’s unemployment rate, to be posted on Friday, will probably climb to 11.2% in July from 7.5% a year earlier, according to Bloomberg Intelligence

- Nigeria’s economy contracted for the first time in more than three years in the second quarter as the crash in oil prices and the global fallout from Covid-19 hit output

©2020 Bloomberg L.P.