China’s Rebound Fuels Emerging Market Optimism

Putting aside the worrying rise in Covid-19 cases, the positive narrative for investors in developing economies remains intact.

(Bloomberg) --

Emerging markets have a lot going for them right now.

Putting aside the worrying rise in Covid-19 cases, the positive narrative for investors in developing economies remains intact. China’s economy probably returned to growth in the second quarter, putting the yuan -- the current barometer of global risk sentiment -- on course for further gains following its biggest weekly jump since January 2019. Goldman Sachs Group Inc. revised its 12-month forecast of the currency to 6.7 from 7, expecting it to benefit from a weaker dollar.

“China’s domestic fundamentals look increasingly solid,” Goldman strategists including New York-based Zach Pandl wrote in a note. “Growth remains sturdy, the virus is reportedly under control, the trade surplus has expanded, and both equity markets and interest rates are moving higher.”

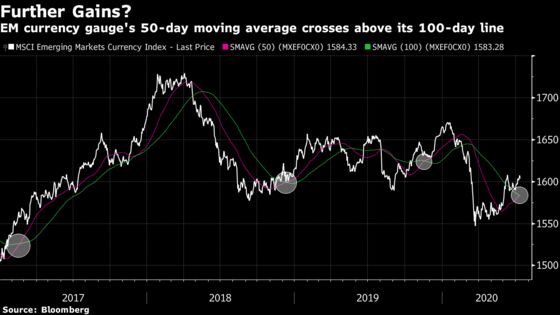

That’s likely to add further momentum to this month’s rally in emerging-market currencies, with the 50-day moving average on an MSCI Inc. gauge now higher than its 100-day counterpart. Developing-nation currencies are cheap and will probably play catch-up with other risky assets as the foreign share of local debt holdings has shrunk to a record low, according to Deutsche Bank AG.

In equities, opportunities for stock selection “still look very good,” even after an MSCI measure climbed to an almost five-month high last week, said Paul Quinsee, J.P. Morgan Asset Management’s New York-based global head of equities.

“Emerging markets still offer reasonable value overall,” he said. “The very fastest-growing companies are expensive, but we can find many high quality investments with solid prospects at attractive prices.”

Listen: EM Weekly Podcast: China Rally, GDP; Key Rate Decisions to Watch

Here’s what investors will be watching this week:

China’s Recovery

- China, the country first hit by the coronavirus pandemic, will probably say Thursday that second-quarter gross domestic product expanded 2.2%, following the historic 6.8% collapse in the first quarter

- Industrial production will likely remain in clear expansion, while consensus expects retail sales to be flat in year-over-year terms

- The yuan has rebounded more than 1% on a basket basis since the June lows, partly reflecting the confidence in the Chinese economy and partly the lower perceived risk of trade tension with the U.S.

- Read: Emerging Markets Ready to Roll on With Biden on Top: Macro View

- China’s June trade data due Tuesday are likely to show a further easing in the year-on-year contraction in both exports and imports

- The extent and longevity of the Chinese rally will come under scrutiny -- still, Chinese stocks performed strongly on Monday to reverse much of Friday’s whiplash. It remains likely that the Chinese government prefers stronger stocks and a buoyant currency

- “The offshore yuan rally has more legs to run,” Stephen Innes, Bangkok-based chief market strategist at Axicorp, said in a report. China’s central bank “has maintained its relatively hands-off approach toward the market, not overly fussed about the stronger yuan”

- Read: CHINA INSIGHT: Virus Controlled, Demand Still Weak - Dashboard

Poland’s Pick

- Investors are ignoring the potential for turbulence in the wake of Polish President Andrzej Duda’s narrow victory in Sunday’s election. Duda won 51.2%, an unassailable lead with more than 99% of precincts reporting, the state electoral commission said on Monday. The challenger, Warsaw Mayor Rafal Trzaskowski, hasn’t conceded defeat and his aides spoke of voting “irregularities” and protests on Sunday, when exit polls predicted a closer race

- The zloty fell 0.3% against the euro as of 7:24 a.m. in New York

- Read: Nationalist Makeover Extended as Polish President Wins Election

- Poland’s central bank will probably leave its policy rate unchanged at 0.1% for the second monthly meeting on Tuesday. The central bank has embraced near-zero rates and is in the midst of one of the emerging world’s biggest quantitative-easing programs, with the Polish economy set to suffer its first recession in three decades

- On Thursday, the central bank will publish core inflation data for June, as well as minutes from the June policy meeting

Other Rate Decisions

Bank Indonesia will probably cut its benchmark interest rate by 25 basis points to 4% on Thursday as inflation continues to decline. The rupiah has been among the worst-performing emerging-market currencies in July so far, due to mixed reviews for the central bank’s plans to directly finance government expenditure

- Also on Thursday, the Bank of Korea will likely stand pat, based on a survey of economists by Bloomberg. A small minority of analysts are expecting a cut on the grounds that economic data continue to fall below the central bank’s published expectations. Korean bonds and the won have remained in a fairly narrow range in the past month, and volatility in the won continues to slip lower in line with the major currencies

- Chile’s central bank will keep its key interest rates at 0.5% on Wednesday, according to all the economists surveyed by Bloomberg. While policy makers are unlikely to announce any further asset purchases, they may announce additional liquidity for banks to support credit growth, Bloomberg Economics says

Economic Data

- India CPI for June rose more than economists expected

- Indian bonds have remained relatively stable since the crisis began, and the differential with Indonesian bonds remains high -- more than 1.3 standard deviations above the five-year average, according to a study by Bloomberg. The further drop in headline CPI that consensus expects may partly vindicate the strong performance of Indian bonds

- On Wednesday, Indonesia and India will release trade data. Although the consensus is for a deterioration both on a month-on-month basis, both trade balances are highly likely to improve for the year as a whole

- India’s improvement has been especially striking and has caused upward pressure on the rupee -- Asia’s fourth-best performer in July -- narrowly following the yuan and the Philippine peso. The relatively sudden appreciation since the beginning of July has led to debate about whether the central bank is finally allowing the improvement of the balance of payments to be reflected in currency strength

- The Philippines might also get its long-awaited remittance data for April. The central bank has forecast a 5% drop for the year as a whole

- South Africa’s consumer-price index probably fell to a 16-year low in May, data may show on Wednesday. That would fuel bets on another reduction in the central-bank’s policy rate on July 23, following four cuts this year that have left the rate at a record low

- Russia’s industrial production probably contracted 7.2% in June, following May’s 9.6% slump, as the effect of the coronavirus pandemic lingered, data may show Wednesday. The ruble has been among the worst-performing emerging-market currencies in the past month

- Brazil’s economic activity index for May, scheduled for publication Tuesday, will probably flag a partial recovery, even as cases of Covid-19 increased. Citigroup expects stability in the real to remain elusive. It’s the world’s worst-performing currency this year

- Argentina’s consumer price inflation figures for May are to be released on Wednesday. Bloomberg Economics expects monthly inflation to remain below 2% for the third time, bringing the year-over-year reading to its lowest level since October 2018

- On Wednesday, Colombian retail sales for May will show the impact of the lockdown on consumer spending. Even as the government reimposes some virus containment measures in Bogota through Aug. 23, the peso remains the best-performing Latin American currency of the quarter so far.

©2020 Bloomberg L.P.