China’s Junk Property Bonds Are Safer Than They Look

(Bloomberg Opinion) -- China’s surging bond defaults are making debt of the nation’s risky developers look like a buy.

Yes, you read that right. It may seem illogical, with China’s $13 trillion fixed-income market heading for its biggest year of missed payments by far. But a few defaults aren’t always a bad thing if they help to keep prices at rational levels.

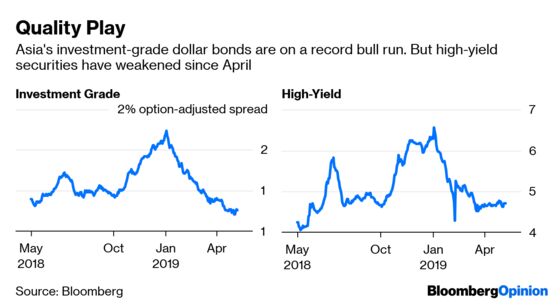

Asian dollar bonds staged a record rally since the first quarter, in part because of the dovish turn by the U.S. Federal Reserve. The spread on the region’s investment-grade securities has narrowed to 130 basis points over Treasuries. It’s been tighter than that only 8% of the time in the past five years.

The spread on Asian junk bonds has also fallen, though not as much. That reflects jitters over Chinese property companies, which have come to dominate the market. In the first four months of the year, they sold a net $29 billion of debt, bringing the amount outstanding to $120 billion. Developers account for more than half of emerging Asia’s high-yield dollar bonds.

All parties end, and Asia’s investment-grade market is no exception. Sooner or later, the U.S.-China trade conflict will start to bite. Global economic growth will slow and the greenback will get stronger: Both factors will erode emerging Asia’s ability to honor its dollar debt.

Meanwhile, there’s interest-rate risk. Are Asia’s bond traders prepared for the doomsday scenario in which the benchmark Treasury yield jumps to 4% or 5%? A key auction last week didn’t end well: The bid-to-cover ratio on the $27 billion sale of 10-year securities was the lowest since March 2009.

With spreads already so low, the potential for capital gains has diminished. What investors can still hope for is yield, and that’s what China’s junk-rated developers can offer. New issues have offered an 8.6 percent coupon on average this year, on notes that have an average maturity of three years.

If nothing else, traders can hold until maturity and hope to collect the coupon without much drama (or interest-rate risk). Investment-grade securities don’t have this buffer.

Granted, high-yield bonds have a greater likelihood of default. However, there’s reason to believe that the concern over Chinese issuers may be overstated, at least in the offshore market. Any developer that wants to survive for the foreseeable future will try its best to honor its dollar obligations. That’s because the onshore market is largely closed to them.

Real-estate companies would ditch the dollar market at the drop of a hat and return to local-currency financing, if regulators would only let them. The cost of borrowing onshore is much lower. Case in point: China Evergrande Group recently issued a four-year yuan bond at a 6.27% coupon rate; it paid 10% to borrow in dollars last month.

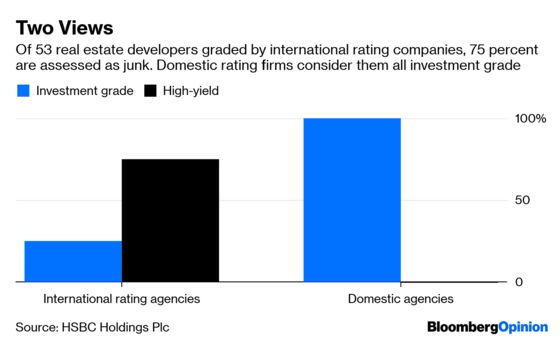

Three-quarters of Chinese property companies covered by international rating companies are considered junk, according to HSBC Holdings Plc. Every single one is rated AAA by domestic agencies in the onshore market.

To be sure, not all developers are created equal. China Minsheng Investment Group Corp., which defaulted after amassing 232 billion yuan ($34 billion) of debt in just five years, was young and reckless when it was courting overseas investors in 2016. Look for companies with a long track record of dollar bond issues.

High-yield comes with risk, but even investment-grade isn’t immune. Hong Kong-based export trader Li & Fung Ltd. was cut to junk by Moody’s Investors Service last year as revenue dropped amid the trade tensions.

Sometimes, the safer investments hide in the most dangerous places.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.