China Considers Further Relief as Deadline Nears on $211 Billion in Bad Debt

China Considers Further Relief as Deadline Nears on $211 Billion in Bad Debt

(Bloomberg) -- In the battle to keep millions of China’s smaller businesses afloat, banks are counting on being allowed another round of exceptions for borrowers falling behind on payments.

The regulator and some lenders have discussed extending loan relief beyond a June 30 deadline for corporates hurt by the pandemic, said people familiar with the matter, asking not to be named as the talks are private. The guidance from Beijing is to offer flexibility on principal and interest payments, the people said. Banks would see a surge in bad loans in the second half without such measures, weakening their ability to keep credit flowing, according to bankers and analysts.

China’s $41 trillion banking system is at the forefront of propping up companies hit early this year by the local outbreak of coronavirus and the impact from its global spread. Called on to rescue the economy, lenders led by Industrial & Commercial Bank of China Ltd. more than doubled loans to businesses in the first quarter, while deferring and rolling over 1.5 trillion yuan ($211 billion) in repayments.

With few signs of a swift economic recovery, a June end to the government’s bad-loan holiday would crystallize the damage to bank balance sheets. Their plight is a window into the stresses emerging around the world as the economic cost of the pandemic becomes clearer, and an initial round of emergency lending and payment deferrals falls short.

“This is a global issue,” said Harry Hu, a Hong Kong-based analyst at S&P Global. Many international authorities are calling for flexibility in the recognition of non-performing loans, he said. “If all of them are marked as bad loans, banks’ provisions will soar and earnings will slump. Without capital accumulation, how are banks supposed to support the economy?”

| Read more ... |

|---|

Millions of Chinese Firms Face Collapse If Banks Don’t Act China Makes Bad Loans Disappear as Virus Pummels Banks China Allows Small Banks to Lower Buffers Against Bad Debt |

Zhang Ming’s is a case in point. A 1 million yuan loan taken at the peak of China’s outbreak in February helped him get his employees back and resume production at his Zhejiang-based company, which makes and exports wooden frames and Christmas ornaments. But as the virus became a pandemic, international clients such as Walmart Inc. and Costco Wholesale Corp. canceled orders, cutting business by 70%. Zhang now has another 3 million yuan of debt coming due this month, not covered by the crisis measures.

“I wish the bank could give me another three months, orders may pick up by then,” he said, asking that his company not be identified in a discussion on private financial matters. “If not, many small manufacturers like us will shut for good this year.”

Like Zhang, business owners around the country are finding that even with the lifting of local lockdowns, customers are slow to return. Chinese consumers aren’t flocking back to restaurants and malls amid concern about incomes, jobs, and the virus itself. Other countries are struggling to strike a balance between containment measures and reopening economies, clouding the picture for exporters.

Buying Time

Chinese authorities in March let lenders delay recognizing bad loans from smaller businesses hit by the virus and allowed some borrowers to delay payments after measures to contain Covid-19 brought much of Asia’s largest economy to a standstill.

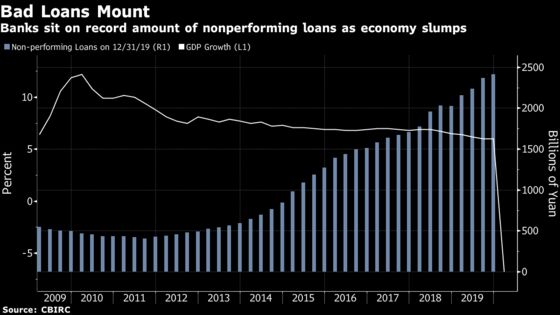

That allowed the banks to report only a 0.06 percentage point increase in non-performing loan ratios to 2.04% at the end of March.

The China Banking and Insurance Regulatory Commission, which has made no official announcement on extended loan relief, didn’t immediately respond to request seeking comment. ICBC declined to comment.

S&P estimates that the non-performing asset ratio, a more stringent measure of troubled advances that includes forborne loans, could almost double to 10% from pre-outbreak levels this year. That’s a projected increase of 8 trillion yuan.

Should Covid-19 disruptions extend beyond 2021, the chances of recouping delayed payments will diminish, S&P has warned. Increased loan provisioning could weigh on profits for years to come, forcing the authorities to come to rescue as they did with at least three banks last year.

Even before the virus outbreak smashed the economy, bankers were dubious of the reliability of official bad loan data, a problem that may only get worse this year.

About 83% of respondents in an annual survey by China Orient Asset Management Co., conducted before the virus flared, said official non-performing loan data understates the actual figures. Almost a quarter said the official numbers were “significantly” lower than reality, pointing to hidden risks stalking banks.

After writing off 5.8 trillion yuan of bad loans between 2017 and 2019, banks will carve out more in the next three years, according to Jason Guo, China banking sector lead partner at Deloitte & Touche LLP.

Such concerns are, for now, swamped by the needs of an economy on track for its worst performance in four decades and the millions who have been rendered jobless. Central bank Governor Yi Gang vowed in a recent interview to use policies such as loan-repayment extensions to support activity.

“There’ll be a lag of three to six months for NPLs to show up on banks’ balance sheets,” said Guo. “How to deal with them will be on every bank’s priority list in the second half of the year.”

©2020 Bloomberg L.P.

With assistance from Bloomberg