China May Cut Deposit Rates So Battered Banks Can Keep Lending

China May Cut Deposit Rates So Battered Banks Can Keep Lending

(Bloomberg) --

China’s battered banks are being asked to sacrifice profits to help millions of cash-squeezed companies struggling under the weight of the coronavirus outbreak. Now they may finally see some relief for themselves.

Liu Guoqiang, a deputy governor of the People’s Bank of China, said over the weekend that policy makers are considering lowering their benchmark deposit rate for the first time in five years. A growing number of analysts are counting the days until such a reduction, with banks desperate for long-term incentives to keep doling out cheaper credit to support businesses as large parts of the economy remain idled.

The new benchmark for corporate loans has been cut three times in the past six months, but the PBOC has stopped short of the bolder move of cutting the deposit rate out of concern for the impact on savers. Lowering rates on 175 trillion yuan ($25 trillion) of household and corporate savings would boost bank margins and free up capacity for lenders already buckling under a surge in bad debt.

“If you keep ‘fleecing the sheep’ without giving them anything in return, some weaker Chinese banks may run into trouble themselves and that will end up destabilizing the financial system,” said Wang Yifeng, a Beijing-based analyst at Everbright Securities Co.

Almost two thirds of Chinese banks’ 265 trillion yuan in liabilities come from deposits. So a cut in the deposit rate will directly lower their funding costs and give them incentive to pass lower lending rates to borrowers, Wang said. Other easing measures, such as reserve ratio cuts, won’t have the same impact, he said.

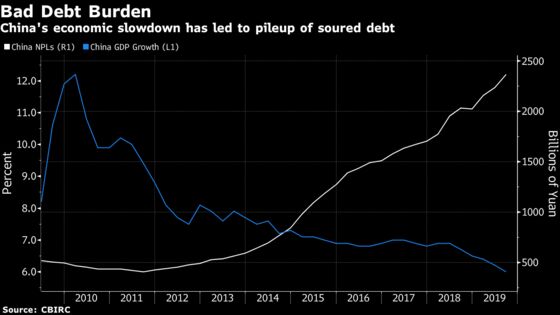

The virus outbreak has added another shock to China’s $41 trillion banking system. Lenders across China were already struggling to stay alive after two years of record debt defaults, triggered by an economic slowdown and a crackdown on debt. Authorities last year seized and bailed out a number of lenders. Even some of the relatively larger banks could require “sizable recapitalization,” S&P Global warned last month.

The rating company also estimated that a prolonged public health emergency could cause the banking system’s bad loan ratio to more than triple to about 6.3%, amounting to an increase of 5.6 trillion yuan.

Meanwhile, the industry’s net interest margin, a measure of lending profitability, narrowed to 2.2% at the end of last year from 2.7% five years ago amid fierce competition for deposits. Government directives to lower borrowing rates for smaller companies is now exacerbating the squeeze.

As part of the latest relief measures to fight the virus, banks were required to provide some firms with loans at preferential interest rates of no higher than 3.15%, with some as low as 2.4%, according to the PBOC. They can borrow from the central bank at 2.75% and would be barely breaking even, once you include operating expenses and potential bad loan charges.

Breaking Even

“To ease the impacted corporates’ financing difficulty and lower their interest burden, we believe government, financial institutions and depositors will all need to sacrifice,” Citigroup Inc. analysts led by Judy Zhang wrote in a note this month. A 5 basis points cut in the demand deposit benchmark rate and a 10 basis points reduction in the term-deposit rate would lift Chinese banks’ margin and boost their profit by 2.1%, they wrote.

Those higher margins could come in handy, with millions of firms such as car dealerships and karaoke bars desperate for credit as demand dries up. The economy will likely grow 4.3% in the first quarter, the slowest in 30 years, according to a recent survey. Full-year growth is expected to be about 5.5%, down from estimates of 5.9% last month.

“The chance of such a rate cut is getting significantly higher as the PB0C needs some actions to show that it’s getting involved in the current campaign against the virus,” Lu Ting, chief China economist at Nomura International HK Ltd., wrote in a note. The demand deposit rate could be cut by 5 basis points while the one-year term-deposit could be lowered by 15 basis points, Lu said.

Even so, Lu, as well as economists at BBVA SA and ANZ Banking Group Ltd., questioned the overall impact of such a move given that those rates are already low at 0.35% and 1.5%, respectively. Many lenders, however, are paying more than the benchmarks to retain savers.

For Chinese banks, whose shares have underperformed the benchmark indexes in Hong Kong and on the mainland for most of the past five years and are trading near record low valuation, cheaper funding costs would come as a welcome relief.

“The deposit rate should be cut sooner than later,” said Liao Zhiming, an analyst at Tianfeng Securities, who expects a 25 basis point cut to 1.25% for one-year deposits. “A moderate cut will ease their pressure on margins.”

To contact Bloomberg News staff for this story: Jun Luo in Shanghai at jluo6@bloomberg.net;Heng Xie in Beijing at hxie34@bloomberg.net;Yinan Zhao in Beijing at yzhao300@bloomberg.net

To contact the editors responsible for this story: Candice Zachariahs at czachariahs2@bloomberg.net, ;Jeffrey Black at jblack25@bloomberg.net, Jonas Bergman, James Mayger

©2020 Bloomberg L.P.

With assistance from Bloomberg