China Makes Bad Loans Disappear as Virus Pummels Banks

China Makes Bad Loans Disappear as Virus Pummels Banking System

(Bloomberg) --

Chinese banks are taking extraordinary measures to avoid recognizing bad loans, seeking to shield themselves and cash-strapped borrowers from the economic fallout of the coronavirus outbreak.

Some of the measures, which include rolling over loans to companies at risk of missing payment deadlines and relaxing guidelines on how to categorize overdue debt, have the explicit approval of regulators in Beijing. Some lenders are also refraining from reporting delinquencies to the country’s centralized credit-scoring system and allowing borrowers to skip interest payments for as long as six months, according to people familiar with the matter, who asked not to be named discussing internal decisions.

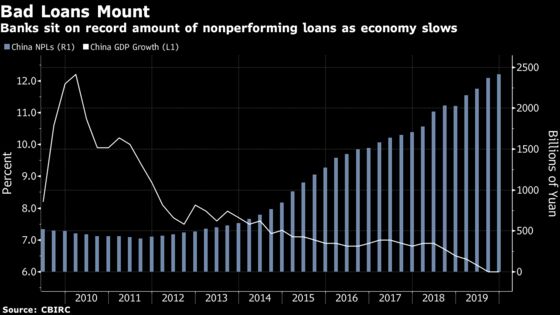

The moves will buy time for both Chinese companies and the nation’s $41 trillion banking industry, after the outbreak brought much of the world’s second-largest economy to a standstill. But they’re also fueling concern about a buildup of hidden risks on lenders’ balance sheets. Some analysts worry that China is reversing a multi-year push to increase the transparency of its financial system and undermining the long-term health of banks.

“This will provide breathing space,” said Harry Hu, a credit analyst at S&P Global Ratings. “It will also likely undermine standards, making some Chinese banks less creditworthy in the long run.”

Earlier this month, S&P said a prolonged health emergency could cause China’s non-performing loan ratio to more than triple to about 6.3%, amounting to an increase of 5.6 trillion yuan ($800 billion) in bad debt.

The push by banks and regulators to tamp down NPLs is part of a broader effort by President Xi Jinping’s government to shore up the Chinese economy, which some forecasters say may suffer a rare quarter-on-quarter contraction in the first three months of this year. In addition to pumping billions of yuan into the banking system to make it easier for lenders to extend credit, authorities have cut interest rates, reduced taxes and pledged to adopt more “proactive” fiscal policies.

Shares of Chinese banks continued to under-performer the benchmark index this year in Hong Kong. The four biggest state-owned banks are trading at an average 0.5 times their estimated book value for this year, near the record low.

The NPL measures mark an abrupt shift in China’s approach toward financial regulation. Authorities in Beijing have spent the past three years trying to instill more discipline in the banking system and develop credit markets that more accurately price risk. As part of that effort, they’ve encouraged banks to be more diligent when accounting for bad loans.

The outbreak has changed the government’s priorities. In a press conference this week, Ye Yanfei, an official at the China Banking and Insurance Regulatory Commission, said policy makers need to be more tolerant when it comes to bad loans. “Saving corporates now is saving banks themselves,” Ye said.

China isn’t the only country to have relaxed accounting standards for banks during a crisis. In April 2009, during the depths of the global recession, mark-to-market rules in the U.S. were eased after banks complained that they resulted in bigger-than-warranted writedowns on thinly traded mortgage securities. While critics of the decision said it reduced transparency, it arguably helped big American lenders recover more quickly from the crisis.

China’s ability to control the pace of NPLs during economic shocks is an advantage of its centralized financial system, according to Leland Miller, the chief executive officer of China Beige Book.

“When you have a party that controls all the counterparties in the economy -- you have state banks loaning to state enterprises and you have state banks loaning to small- and medium-sized enterprises -- you can tell them to lend,” Miller said in an interview on Money Undercover with Bloomberg TV’s Lisa Abramowicz. “You never have to freeze up liquidity in the same way that a commercial financial system would work.”

Yet even if China’s banks turn on the credit taps, lots of businesses may struggle to secure the funding they need to stay afloat.

A survey of small- and medium-sized Chinese companies conducted this month showed that a third of respondents only had enough cash to cover fixed expenses for a month, with another third running out within two months. About two-thirds of the country’s 80 million small businesses, including many mom-and-pop shops, lacked access to loans as of 2018, according to China’s National Institution for Finance & Development.

It remains to be seen whether the benefits of delaying NPLs will outweigh the costs. Much depends on how quickly Chinese authorities can contain the outbreak and get the country back to work. In the week to Feb. 21, the economy was likely running at 50%-60% capacity, according to Bloomberg Economics.

A sharp recovery in coming months would likely ease concerns that banks are obscuring the true health of their balance sheets. “If they can tide the virus over, then the delinquent loans will disappear,” said Zhang Shuaishuai, a banking analyst at China International Capital Corp.

But that’s far from a given. S&P analysts see scope for caution, saying last week that it may take years for the industry to revert to normal standards for recognizing NPLs and that some banks may see their long-term health suffer as a result.

To contact Bloomberg News staff for this story: Jun Luo in Shanghai at jluo6@bloomberg.net;Zheng Li in Shanghai at zli698@bloomberg.net;Heng Xie in Beijing at hxie34@bloomberg.net

To contact the editors responsible for this story: Candice Zachariahs at czachariahs2@bloomberg.net, Jonas Bergman, Michael Patterson

©2020 Bloomberg L.P.

With assistance from Bloomberg