(Bloomberg Opinion) -- China's overseas M&A isn't quite dead.

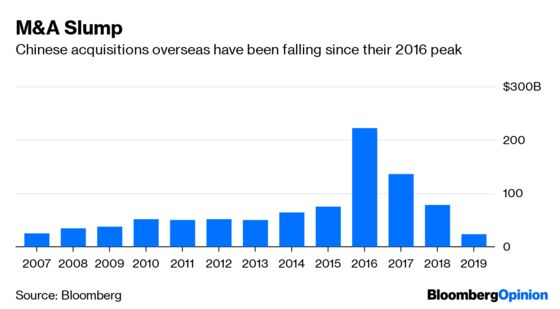

But you can forget the acquisition of strategic assets in the West: That $45.5 billion record purchase by China National Chemical Corp. of Swiss agribusiness firm Syngenta AG in 2017 is a thing of the past. With Beijing still worried about capital outflows, and protectionism deepening globally, the value of China’s deals abroad fell to $78 billion last year from a peak of $222 billion in 2016.

So, what is getting through? Infrastructure investment in emerging markets, for one, where the need for China’s money outweighs the desire to repel its influence. From Malaysia to Brazil, projects billed under President Xi Jinping’s Belt and Road campaign are forging ahead despite popular backlash. On the other side of the spectrum, deals that barely register on the geopolitical barometer are also squeaking by. These can include foreign fashion brands and commercial real-estate firms. Yet even these benign sectors could face roadblocks soon enough: National security is a slippery slope.

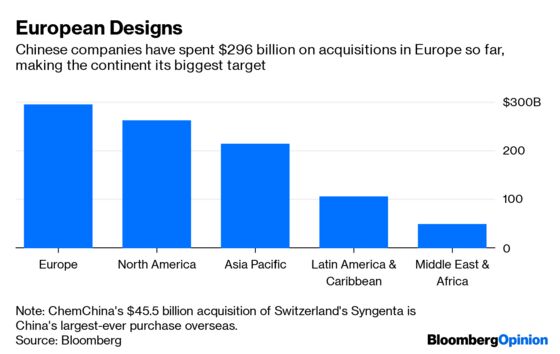

For now, Brazil remains a bright spot for Chinese dealmaking, particularly among state-owned firms. China Three Gorges Corp. is looking to acquire the Brazilian assets of EDP-Energias de Portugal SA, having aborted a 9.1 billion euro ($10.2 billion) deal to buy the entire company in April. In May, China General Nuclear Power Corp. forked out $739.2 million for Italian multinational Enel SpA’s wind farms and solar plants in the Latin American country. But while Chinese companies have spent a cumulative $56.6 billion in acquisitions in Brazil, relations between the two countries have been prickly in recent months as suspicions mount over Belt and Road. In April, President Jair Bolsonaro said, “The Chinese can buy in Brazil, but they can’t buy Brazil,” during a breakfast with journalists.

Foreign luxury brands have proven less contentious, particularly the European lines that mainland shoppers covet. Apparel company Shandong Ruyi Group, for instance, wants to become the LVMH of China: In January, it bought The Lycra Co., maker of the elastic material used in yoga pants, and eventually plans to take the company public. Ruyi has been on a buying spree of marquee fashion brands including U.K. trench coat maker Aquascutum and France’s SMCP SA, whose labels include Sandro and Maje. Last year, Shanghai-based Fosun International Ltd. snapped up Lanvin, France’s oldest surviving fashion house, and is in talks to buy Thomas Cook Group Plc's tour-operator business. Meanwhile investment firm Hillhouse Capital Management Ltd. is buying Scottish whisky maker Loch Lomond Distillers Ltd. Asian investment firms often buy overseas brands with the aim of eventually bringing them into China.

Commercial real estate has also been a relatively safe target: In recent years, some of China’s largest acquisitions in developed markets have been companies that run warehouses. China Investment Corp. bought European logistics property business Logicor from Blackstone Group LP, while China Vanke Co. led a group including Hillhouse in buying Global Logistic Properties Ltd. from Singapore’s sovereign wealth fund.

Yet in this charged political climate, today’s safe targets could be on tomorrow’s blacklist. In France, even yogurt became a political lightning rod when the government blocked PepsiCo Inc. from buying Danone SA in 2005. Who’s to say we can draw the line at yoga pants?

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.