These Indicators Show Whether China Housing Clampdown Is Easing

These Indicators Show Whether China Housing Clampdown Is Easing

(Bloomberg) -- Judging whether Beijing is dialing back on its property crackdown has become essential to investors looking at the industry’s stressed stocks and bonds.

But the Communist Party’s opaque governance means investors are forced to rely on media reports to learn about easing measures, the impact of which can be ambiguous. Developers themselves aren’t always clear on their plans to raise cash or pay down debt.

That’s prompting money managers to look instead at indicators such as sales data, household loans, bond sales and equity placements for a more detailed picture of developers’ funding stress. While definitive conclusions are difficult, the numbers suggest the industry is a long way from returning to pre-crisis normal.

“A reopening of the market is difficult to predict,” Moody’s Investors Service analysts led by Annalisa Di Chiara wrote in a note dated Wednesday. “While refinancing remains the key motive for debt issuance, investors remain cautious and selective, and as a result, access to the U.S. dollar bond market remains uncertain, particularly for lower rated companies.”

Government efforts so far suggest Beijing’s solution to private developers’ liquidity woes is the acquisition of assets by larger state-owned firms. In recent days, Agile Group Holdings Ltd. and Shimao Group Holdings Ltd. have announced sales of stakes in companies to state-owned enterprises to raise cash. Enlarging the state’s influence would provide greater stability to the crucial sector and limit the risk of financial fallout.

The following are some of the main indicators for gauging the stress on real estate firms:

Housing Demand

Home sales fell for a sixth month in December, while more than 80% of the firms that disclosed full-year sales guidance failed to meet their 2021 targets, local media reported. Proceeds from home sales generally make up more than half of developers’ cash inflows, according to calculations based on official data. Long-term household loans, a key proxy for mortgage loans, grew by the slowest amount since February 2020.

Making things worse, officials have limited developers’ access to cash from presold properties tied up in escrow accounts. Regulators are considering lifting some of the restrictions, people familiar with the matter told Bloomberg.

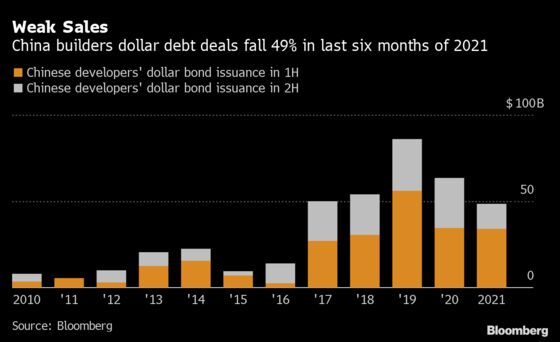

Bond sales

The offshore market -- a key source of funds for many private developers -- remains largely closed off, with the yield on Chinese junk bonds prohibitively expensive at 19%. Only one of China’s top 20 developers by sales, Greentown China Holdings Ltd., has sold a dollar bond in January, compared to at least seven in the previous period last year, Bloomberg-compiled data show.

Sales of dollar notes in the second half of 2021 fell 49% to $14.7 billion compared to the previous year as concern over contagion from China Evergrande Group flared.

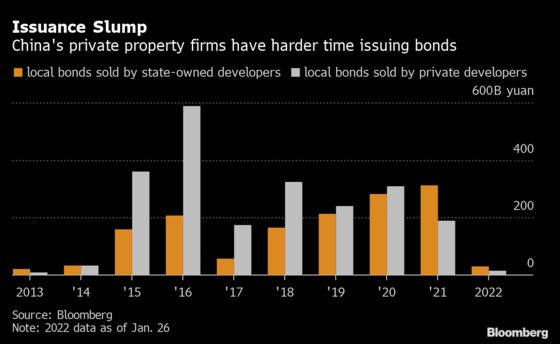

The onshore market doesn’t show a much better picture for private developers. Last year, local bond sales by such firms fell 39% to 190 billion yuan ($29.9 billion). The situation is very different for state-owned developers. They sold 315 billion yuan of local bonds, up 12% from a year earlier, to overtake private peers for the first time in seven years.

Authorities in December eased limits on borrowing by major property firms used to fund mergers and acquisitions, which may make it easier for state-owned companies to acquire assets being sold by weaker developers. Regional lender Shanghai Pudong Development Bank Co. sold a bond to help fund loans for M&A in the sector, and at least two state-owned developers planned to issue similar notes.

Property firms have $44 billion of local and offshore debt maturing in the first half of the year.

Share placements

More developers are turning to the equity market as an alternative channel to raise cash this year, but the result typically triggers a sharp selloff. Valuations for developers remain low in the equity market, trading at just 0.3 times book value, and about 2.7 times earnings on average. Because new stock is typically sold at a discount to market, low multiples mean developers would need to sell plenty of new shares to raise a meaningful amount of cash.

With Hong Kong’s stock market under pressure from souring sentiment onshore and in international markets, a glut of fresh stock from a struggling sector is unlikely to find strong demand.

There were record share-price declines on Thursday for Times China Holdings Ltd. after it placed new shares in Hong Kong and Logan Group Co., which sold equity-linked securities to refinance existing debt. Sunac China Holdings Ltd. also plunged by a record after raising $580 million earlier in January. Convertible bonds -- equity-like instruments that can convert into stock -- were recently sold by Country Garden Holdings Co. and Hopson Development Holdings Ltd.

Trust funding

The shadow banking sector, including the $3 trillion trust industry, has already shrunk in recent years amid government efforts to curb hidden debt. That’s adding pressure for smaller, private firms who struggle to secure loans from banks.

The property sector’s net financing from trusts was negative 236.9 billion yuan last year, according to a CICC report. Moody’s expects outflows to continue this year as authorities maintain their tight regulatory oversight.

That could make it challenging for developers to pay mounting trust payment bills -- they face 142.4 billion yuan in trust payments due in the first quarter, according to data tracker Use Trust.

Bank loans

Chinese banks had more than 51.4 trillion yuan of outstanding loans to the real estate sector as of September, including 12.2 trillion yuan for property development. The exposure was more than any other industry, and accounted for about 27% of the nation’s total lending, according to the central bank.

Macro outlook

China’s central bank already cut three of its policy rates in January, though at 10 basis points the reductions were small. Banks also lowered the five-year loan prime rate which serves as the basis for mortgages. That reduction was even narrower at just 5 basis points, disappointing investors at the time. Most analysts and economists agree more monetary easing is needed, especially if falling home prices take a toll on already-fragile consumer sentiment. Property comprises as much as 40% of household assets by some estimates.

A planned nationwide property tax is also an overhang for property buyers. Citigroup Inc. economists have said China could remove that uncertainty by rolling out a milder levy “as soon as possible.”

©2022 Bloomberg L.P.

With assistance from Bloomberg