China Is Keeping Stimulus in Check. Here’s What May Change That

A miniscule cut to the 1-year bank funding rate announced Tuesday amid a bond sell-off is the latest sign of restraint.

(Bloomberg) --

A rash of manufacturing job losses, a collapse in investment, a property-market bust or renewed turmoil in the banking sector: These are the risks that could end China’s current policy of restrained stimulus.

So far, they’re being held at bay, and China’s officials are working to keep it that way, managing rather than reversing the slowdown in the world’s second-largest economy.

A miniscule cut to the 1-year bank funding rate announced Tuesday amid a bond sell-off is the latest sign of restraint. Both the People’s Bank of China and the fiscal authorities have refrained from stimulating activity through bigger rate cuts and increased spending, wary of reflating the debt bubble they’ve worked hard over the past few years to contain.

“China is done with the approach of driving up growth straightaway,” said Nie Wen, an economist at Huabao Trust Co. in Shanghai. “The constrained nature of those policies needs longer time to feed in, and till then, the leaders are stitching the patches to avoid a sharp decline in growth.”

The trickiness of the balancing act is best seen in the job market, always the most important focus for the Communist Party’s drive for stability. One problem with that is that the official jobless rate isn’t sensitive enough to identify turning points in the labor market.

While the government announced it has “almost achieved” its target of creating 11 million jobs this year, months ahead of schedule, the official unemployment rate is higher than it was last year and could keep rising toward the end of the year, according to China International Capital Corp. And other indicators of employment don’t look so rosy, although there is some signs of stabilization.

“The government may resort to more supply-side measures to absorb potential unemployment pressure in a down cycle,” such as easing the barriers for investment in services, given there’s no quick fix to reboot the economy using monetary policy, Liang Hong, chief economist at CICC, wrote in a recent note.

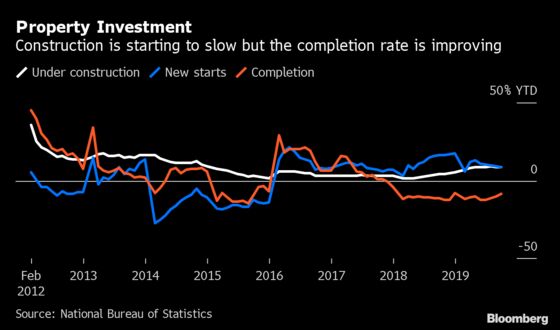

Another source of instability would be a rapid deceleration in property investment as developers face tightening financing conditions, according to Yao Wei, chief China economist at Societe Generale SA in Paris.

For now, a large amount of construction is still ongoing, but projects are starting at a slower pace and the completion rate is improving. That can lead to two layers of complications -- a quick fall in property starts could jeopardize overall investment, but more completed new houses might boost the sales of second-tier goods from glass to decoration materials and home appliances. The net effect of those two factors will be one to watch.

Unless easing trade tensions lead to a revival in companies pouring money into new equipment, the onus will likely remain on the government to increase spending on infrastructure to keep overall investment figures healthy. Authorities have loosened the rules on the financing of major infrastructure and rolled back environment curbs.

China’s debt as a share of gross domestic product rose marginally to 257.6% in the first eight months this year from 248.5% at the end of 2018, according to the calculations by Bloomberg Economics. That ratio could pick up faster if the economic slowdown deepens.

Debt defaults are increasing, but debt resolutions have lagged behind, Goldman Sachs Group Inc. warned last month. The state takeover of Baoshang Bank Co. worsened the situation of Chinese small lenders, adding to the woes of weaker capital buffers, higher financing costs and difficulty in attracting deposits.

For now though, the state’s approach to the banking sector appears to have warded off a worse decline in confidence, and the government is now considering sweeping reforms to shore up smaller lenders and force the weaker ones to merge or restructure.

“Stability is the bottom line,” said Martin Chorzempa, a research fellow at Peterson Institute for International Economics in Washington. The authorities are “tinkering around” to defusing risks without causing a sharp decline of growth, and people looking for signals of China giving up derisking and hitting the gas of stimulus again would be taking “the wrong way to look at it,” he said.

To contact Bloomberg News staff for this story: Yinan Zhao in Beijing at yzhao300@bloomberg.net

To contact the editors responsible for this story: Jeffrey Black at jblack25@bloomberg.net, Malcolm Scott

©2019 Bloomberg L.P.

With assistance from Bloomberg